By Stephen L. Nesbitt – Chief Executive Officer, Chief Investment Officer of Cliffwater.

In 2020 we characterized senior secured direct lending as “All Weather”, at that time crediting covenant protections, amendment fees, and sponsor support for strong relative performance during a severe, albeit short recession.1 Recently, another Weather event – unexpected inflation – is causing a rise in interest rates, pushing bond prices lower at a rate not seen in years. As we anticipated in our earlier research, direct lending has performed well as rates have risen while its fixed rate counterpart has stumbled.

Investors are rightfully concerned about interest rates. Higher inflation requires interest rates to rise to keep monetary policy unchanged. If not, policy would de facto become increasingly accommodative and spur additional inflation. An already growing economy receiving fiscal stimulus from the COVID and infrastructure congressional bills makes it very unlikely that the Fed wants to add further monetary stimulus to the mix. Consequently, interest rate increases are on the way; how much and when remains uncertain.

In the current environment investors should reevaluate allocations to fixed rate securities, the most popular being represented by the Bloomberg Aggregate Bond Index, comprised of all investment grade U.S. fixed income securities. This index, and the portfolios/ETFs that track it, have benefited from over 20 years of declining interest rates. That tailwind appears over for the foreseeable future. One substitute is senior secured floating rate corporate debt, whose yield increases with the general level of interest rates.

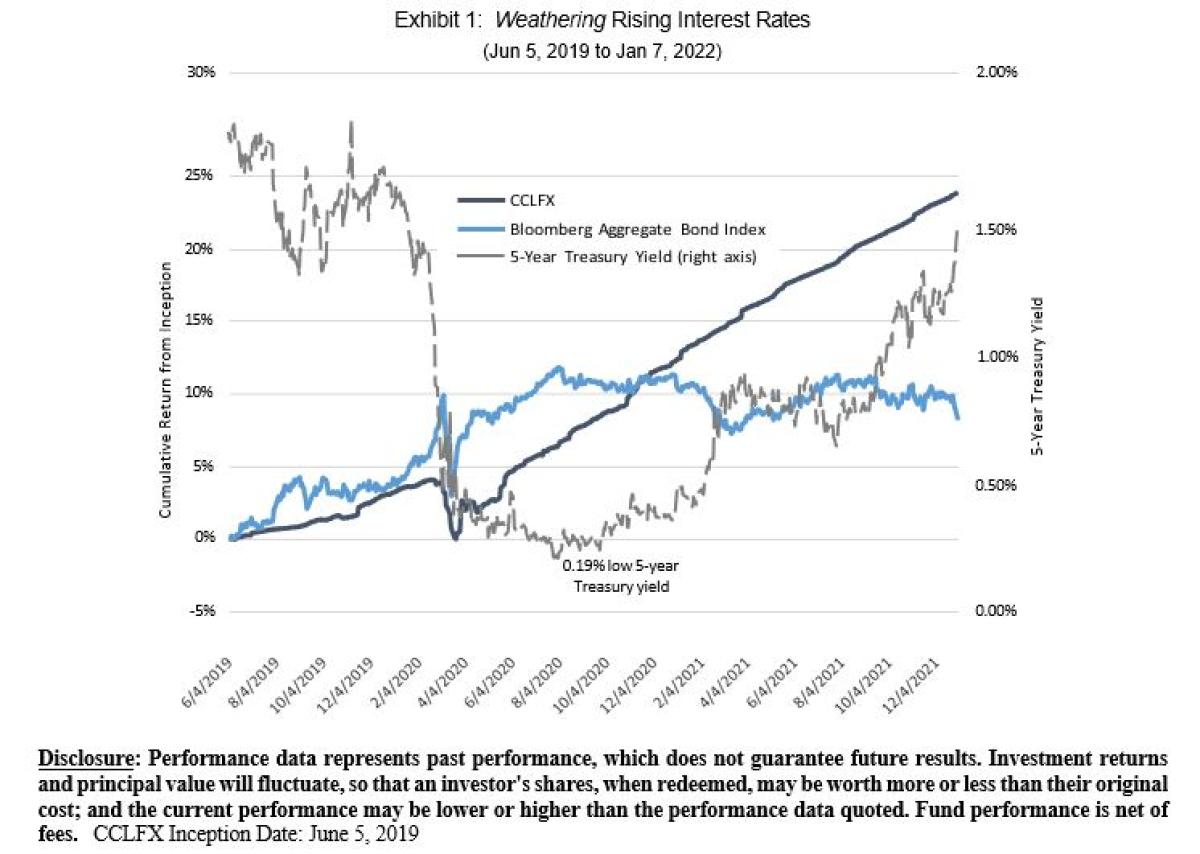

Exhibit 1 shows comparative performance of the Cliffwater Corporate Lending Fund (CCLFX), comprised of floating rate senior secured direct loans, against the Bloomberg Aggregate Bond Index over the 2.5 years CCLFX has been operating. The left-hand scale plots cumulative return for CCLFX and the Bloomberg Aggregate Bond Index. The right-hand scale plots 5-year Treasury yield, having a duration similar to the Bloomberg Aggregate Bond Index.

Exhibit 1 clearly shows the negative sensitivity of the Bloomberg Aggregate Bond Index to rising rates that began August 4, 2020, from a low yield equal to 0.19%, and the insensitivity of CCLFX returns, whose securities are floating rate, to interest rates.

Investor allocations to direct lending have been on the rise with higher current yields compared to traditional public bonds being the likely primary reason to date. Going forward, we believe investors will look to risk mitigation against rising interest rates as another motivator to increase allocations to private debt.

About the Author:

Steve Nesbitt is Chief Executive Officer and oversees all investment research as the firm’s Chief Investment Officer. Prior to forming Cliffwater in 2004, Steve was a Senior Managing Director at Wilshire Associates. From 1990 to 2004, Steve led the Consulting division at Wilshire Associates and also started and built its asset management business using a 'manager of managers' investment approach, including private equity and hedge fund-of-fund portfolios. Steve started his career at Wells Fargo Investment Advisors, an early pioneer in index funds, where he developed and managed index funds and oversaw asset allocation.

He graduated summa cum laude, with a BA in Mathematics and Economics from Eisenhower College (Rochester Institute of Technology), and an MBA, with Distinction, from The Wharton School at The University of Pennsylvania.

Stephen L. Nesbitt snesbitt@cliffwater.com

The views expressed herein are the views of Cliffwater LLC (“Cliffwater”) only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Cliffwater has not conducted an independent verification of the information. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Cliffwater. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement, is being distributed for informational purposes only and should not be considered investment advice, nor shall it be construed as an offer or solicitation of an offer for the purchase or sale of any security. The information we provide does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. Cliffwater shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. Past performance does not guarantee future performance. Future returns are not guaranteed, and a loss of principal may occur. Statements that are nonfactual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Cliffwater is a service mark of Cliffwater LLC.