Jeffrey Kanne, President and CEO, Darob Malek-Madani, Head of Research & Analysis, National Real Estate Advisors.

Historically, institutional-grade, core real estate produces an annualized return in the high single digits — settling between less risky bonds and more volatile stocks. Investors can try to bump up performance through value-added and opportunistic strategies involving various leverage, redevelopment, and development plays. Market timing — buy low, sell high — strategies can also work with the proper foresight. But windows for successful higher-return investing can be rather narrow, mostly confined to the early part of a cycle when investors naturally tend to be more tentative after addressing problems at market nadirs; and early cycle value-added and opportunistic funds generally outperform where follow-on funds often can lag or even disappoint. Coveted core real estate — existing grade A properties located in the leading real estate markets — provides a more consistent income stream from strong rent rolls and steady, if unspectacular, appreciation, holding value better in down markets than commodity properties.

STRUGGLING TO FIND CORE

Pension funds, their consultants, and advisers continually struggle to find the right asset allocation mix along the efficient frontier — looking for the highest expected return at a given level of risk. While core real estate is highly attractive, demand tends to outstrip supply, pushing down cap rates and discouraging investors unwilling or unable to pay the cost, especially in mature to later stages of any real estate cycle. Today, this pricing-out phenomenon for core real estate is more evident than ever before as institutional investors have bumped up their real estate allocation targets to the highest levels in history, and offshore investors swarm to park money in “safe” U.S. assets. Sim- ply, there just is not enough core real estate to satisfy the appetites. As a result, maybe not surprisingly, “Build-to-Core” has entered the real estate marketing lexicon. Because investors cannot find enough existing core assets, they gravitate to invest in development or redevelopment projects that create core assets in top markets and either sell them into the demand wave or more strategically hold them for sought-after, solid, long-term returns.

Merchant builders tout the former strategy — raising capital for opportunity development funds, selling the stabilized project for as much as possible to core investors, and moving on to the next development with profit, fees and promotes in hand. The limited partners do not realize the full benefits of owning the stabilized core assets, while the core buyer has bought the new asset effectively at a retail mark-up premium. Inevitably, the merchant builder-general partner will try to sell its limited partners on reinvesting their gains in the next wave of projects based on the recent success, but as noted, often these later cycle projects do not turn out as well in the riskier part of the cycle.

BUILD-TO-CORE PORTFOLIO STRATEGY

An alternate approach, an ongoing build-to-core strategy, has merit in establishing a portfolio of modern assets that over the long term can outperform older, existing buildings in competing for tenants and achieving higher occupancies and potentially better rents. A build-to-core portfolio consists of development projects, as well as a stabilized portfolio of modern assets derived from completed projects. Among advisers and over time, portfolio mixes may vary, but for the purposes of this article we define a build-to-core portfolio as 75 percent newly constructed core properties (properties five years old or less) and 25 percent development assets. The distinguishing feature of build-to-core derives from the stabilized core portion of the portfolio being composed of newly constructed, modern buildings. Modern buildings can feature more technologically efficient and sustainable systems, as well as more attractive amenities. As properties age, stabilized assets can be selectively sold at peaking values to maintain a proper portfolio balance between stabilized and development assets while keeping the stabilized portfolio on the leading edge of technological trends. With a long-term hold strategy in mind and judicious use of leverage across the entire portfolio, any setbacks or delays in specific development projects can be more easily managed through inevitable cyclical downturns. On the risk-return spectrum, this build-to-core portfolio strategy falls in the core-plus category, achieving a higher return than core and at a risk level significantly below value-add and opportunistic over a 20-year horizon.

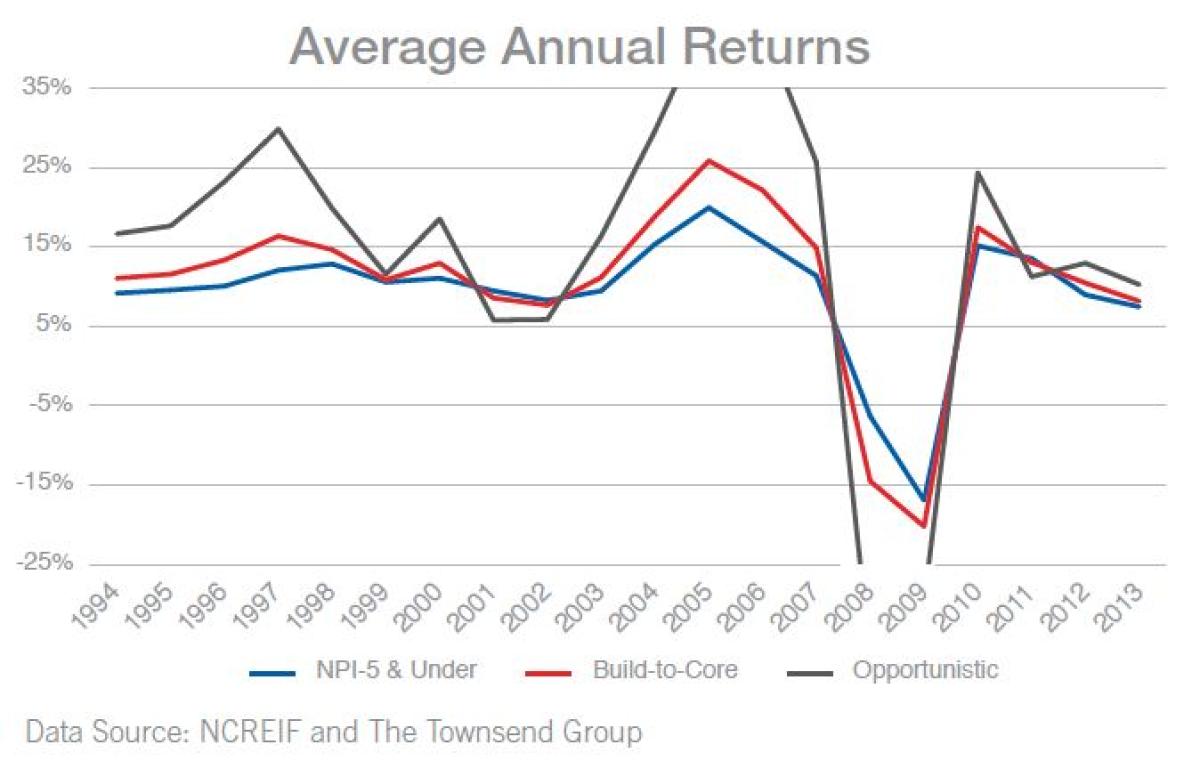

Above is a model of typical build-to-core portfolio returns compared to opportunistic and core strategies. The core index used is NCREIF’s NPI index including only properties 5 years old or younger. The opportunistic index is a product produced jointly by NCREIF and The Townsend Group and is populated by funds that may pursue multiple strategies, including development. In following our build-to-core definition, the build-to-core index is composed of 75 percent NPI – 5 and under and 25 percent opportunistic. As can be seen in the chart, the build-to-core index returns almost always fall between the core and opportunistic strategies, suggesting that the build-to-core strategy is best served by a core-plus designation.

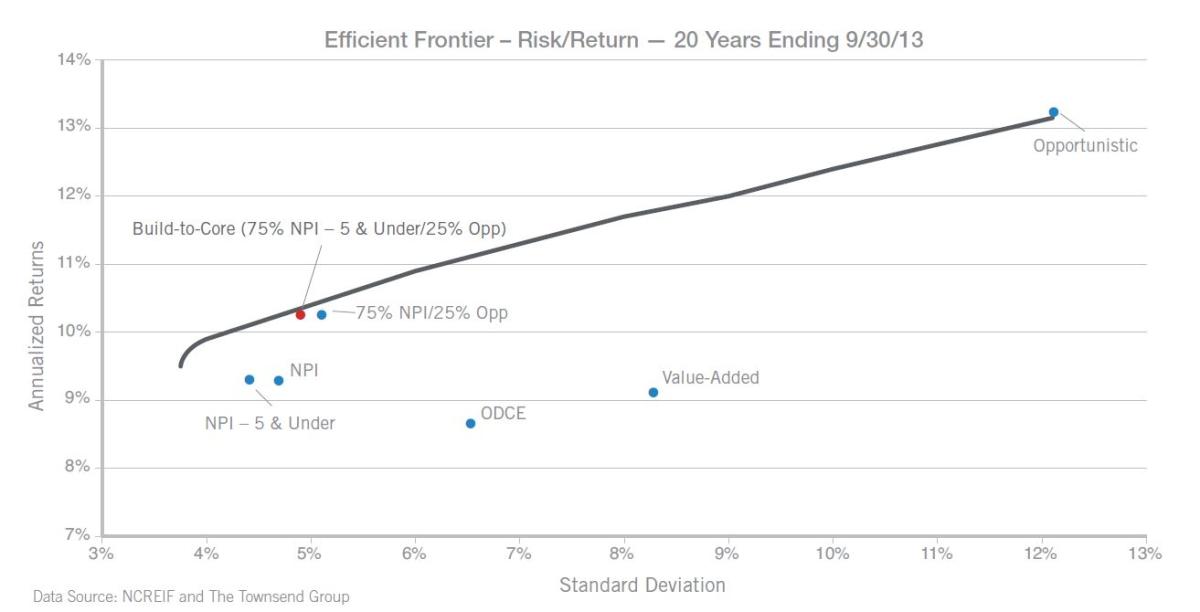

On the opposite page is a chart that depicts the annualized returns and standard deviations of the build-to-core index as it compares to the two indices above, as well as the NCREIF ODCE index and a value-added index produced by NCREIF and The Townsend Group. It also includes an index composed of 75 percent NPI and 25 percent opportunistic. This latter index represents a true alternative to build-to-core’s strategy, which could be achieved using two different managers rather than a single build-to-core vehicle.

In addition to the average annual returns and standard deviations of the indices depicted above, the chart includes an efficient frontier. The efficient frontier line represents the highest return achievable given each level of risk creating a portfolio from all indices included in the chart: NPI, NPI – 5 and under, ODCE, value-added and opportunistic. In evaluating the performance data for the different categories during the 20-year period, several inferences can be drawn:

- In addition to surpassing the NPI, build-to-core outperformed ODCE (leveraged core) and value-added indexes over the 20-year period.

- In getting closer to the efficient frontier, build-to-core registers a lower standard deviation and similar return to the alternative portfolio comprised by NPI (75 percent) and opportunistic (25 percent) that could be produced from two separate managers.

- The NPI – 5 and under’s lower standard deviation in the chart compared with the NPI illustrates that new core properties (found in a build-to-core portfolio) are lower risk than older core properties because ultimately they may attract higher occu- pancies and revenues with greater operating efficiencies.

Occupancy data supports the case for the build-to-core advantage when holding assets in a long-term portfolio. NPI – 5 and under properties score better occupancy levels than NPI properties (see Exhibit: Occupancy Levels).

The chart above depicts the risk/return of the NCREIF Property index, NCREIF ODCE index, as well as the opportunistic and value-added fund indices produced jointly by NCREIF and The Townsend Group. In addition to these indices, the chart depicts the returns of properties included in the NCREIF Property Index excluding all properties over five years old. The chart also includes composite indices constructed by National Real Estate Advisors to depict the risk/ return of two hypothetical portfolios, comprising: (1) 75 percent of the NCREIF Property index and 25 percent of the opportunistic index and (2) the 75 percent of the NCREIF Property index excluding properties over five years old and 25 percent of the opportunistic index (build-to-core). All the indices are derived for the 20 years ending 9/30/13, the most recent time period in which all data is available.

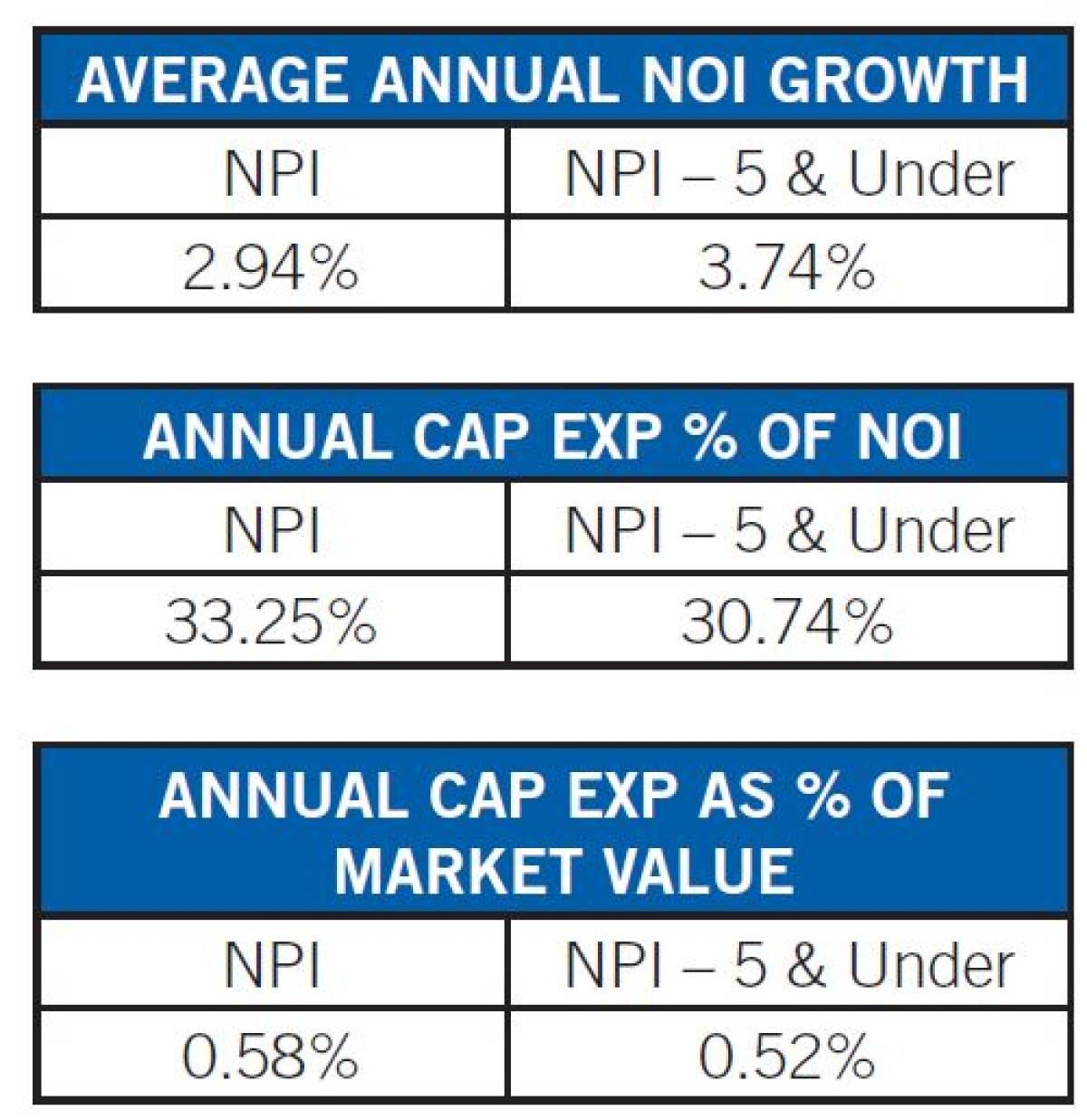

An analysis of net operating income data since 1983 also shows younger properties (NPI – 5 and under) achieved significantly faster NOI growth than older (NPI) properties by 3.74 percent versus 2.94 percent.

In addition, build-to-core properties can benefit from lower capital expenditures that buttress income returns. The charts to the left show that younger properties (NPI – 5 and under) on average had lower capital expenses both as a percentage of NOI and percentage of market value.

The occupancy, operating expense and capital cost of new buildings translates into lower risk due to their ability to attract tenants and maintain occupancy. This new-building advantage is captured in the build-to-core strategy, which seeks to produce core-plus returns with a portfolio of stabilized assets that is constantly refreshed by development projects.

BUILD-TO-CORE

Achieving solid build-to-core performance requires a focused adviser strategy and specialized development know-how, which many institutional advisers lack because necessary firm infrastructure is expensive and difficult to acquire. But advisers with development and project management skill sets can access opportunities that many managers cannot, providing a significant competitive advantage to investors seeking investments in new properties.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.