By Paula Tekulová, Junior Quant Analyst, Quantpedia.

A recent spring 2022 crisis in the cryptocurrency market emphasized the importance of market-neutral crypto trading strategies. It’s not enough just to HODL crypto market and hope for the everlasting bull market. Therefore, we continue our series of research articles about the cryptocurrency market and offer an analysis of the skewness anomaly. So after our description of the skewness effect in commodities, an article about the multi-asset skewness strategy, and observation of the skewness/lottery effect in ETFs, we have one more asset class, where we can find lottery/skewness anomaly – in cryptocurrencies.

Skewness and investing

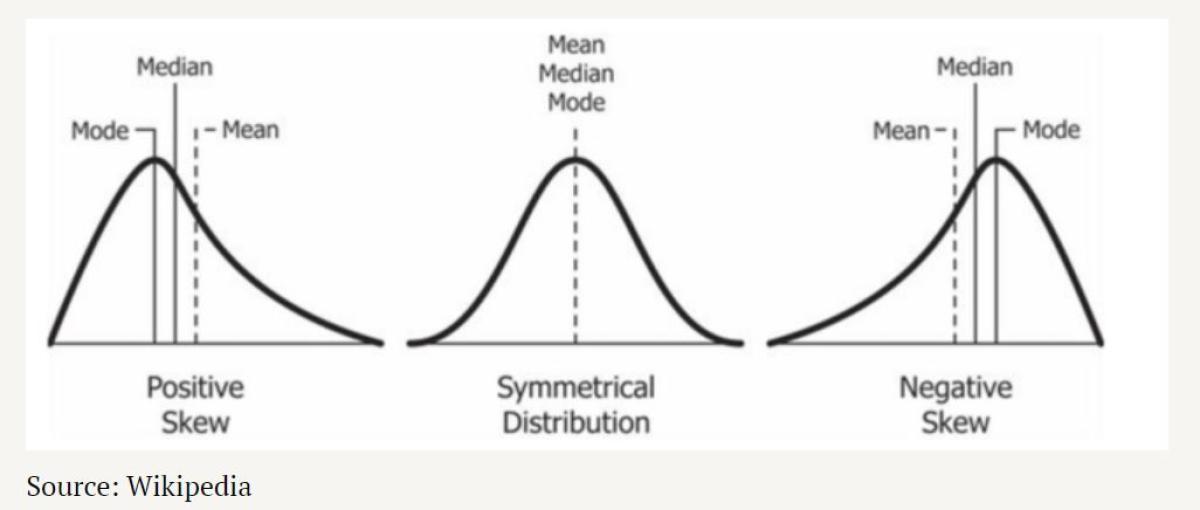

Skewness is a distortion or asymmetry in a collection of data that deviates from the symmetrical bell curve, or normal distribution. The curve is considered to be skewed if it is displaced to the left or right. Skewness may be expressed as a measure of how much a particular distribution deviates from a normal distribution. The skew of a normal distribution is zero, but a lognormal distribution, for example, has some right-skew.

When evaluating a return distribution, investors look for skewness, which evaluates the data set’s extremes rather than relying just on the average. Short or medium-term investors, in particular, must consider extremes since they are less likely to keep a position long enough to trust the average to sort itself out. Standard deviation is often used by investors to forecast future returns, however, it presupposes a normal distribution. Because few return distributions are near to normal, skewness is an interesting metric to use for predicting performance.

Skewness risk refers to the possibility that a model incorrectly assumes a normal distribution of instrument returns when the returns are skewed to the left or right of the mean. A positive skew means that the right-hand tail is longer than the left-hand tail and that the majority of the values are located to the left of the mean. A zero value implies that the values are very evenly distributed on both sides of the mean, reflecting a symmetric distribution in most cases (though not always).

Data and the Strategy

Cryptocurrencies are relatively a new type of asset, and their popularity is rapidly growing. Cryptocurrencies opened the door to trading for the general public and especially the younger generation found it as a really easy opportunity to make (or indeed lose) money. Due to the high demand for cryptocurrencies and strategies the literature on this field is rapidly growing, even if it is still not well developed. Blockchain is the underlying technology that allows cryptocurrencies to be created. The operation of such a technological gadget is based on the upkeep of immutable distributed ledgers in thousands of nodes. New cryptocurrencies are emerging in the financial sector as a result of the blockchain network’s transactional reliability.

Bitcoin is the most well-known member of the crypto family and the most valuable cryptocurrency in terms of market capitalization. Despite Bitcoin supremacy, cryptocurrencies are becoming increasingly competitive. Indeed, Bitcoin’s market share has fallen from 80% at the end of May 2016 to 48% at the end of May 2017; by 2020, Bitcoin’s market share was about 38%. However, we will not only look at Bitcoin, which we covered well in our articles about Bitcoin’s overnight seasonality and trend/reversion trading but also at a number of other popular coins. More specifically, for this research, we choose the 45 most popular coins purely based on their trading history. To be more specific, we choose cryptocurrencies that have a trading history at least from 1.1.2018 (or earlier) until this date (see Reference 3 for a complete list).

Data

The dataset contains the last four-year daily exchange rates data (from January 2018 to March 2022) for the 45 cryptocurrencies and was obtained from Coinmetrics. In particular, we have selected the daily exchange rates with US Dollar, since such bilateral exchange rates are the most studied by previous literature due to data availability.

Monthly Model

Now, we can look closely at our models. First, a monthly model, that each day calculates the skewness based on the last 30 days.

The rules: For each month take the most recent skewness. Calculate the monthly performance from the data and sort cryptocurrencies into two portfolios. We can sort cryptocurrencies into deciles, quintiles, quartiles, terciles, or halves. For illustration, let’s consider sorting cryptocurrencies into quartiles. Then the first portfolio contains 11 bottom cryptocurrencies (with the lowest skewness). The second portfolio contains the top 11 cryptocurrencies (with the highest skewness). Long the bottom 11 portfolios and short the top 11 portfolios. The portfolios are rebalanced monthly.

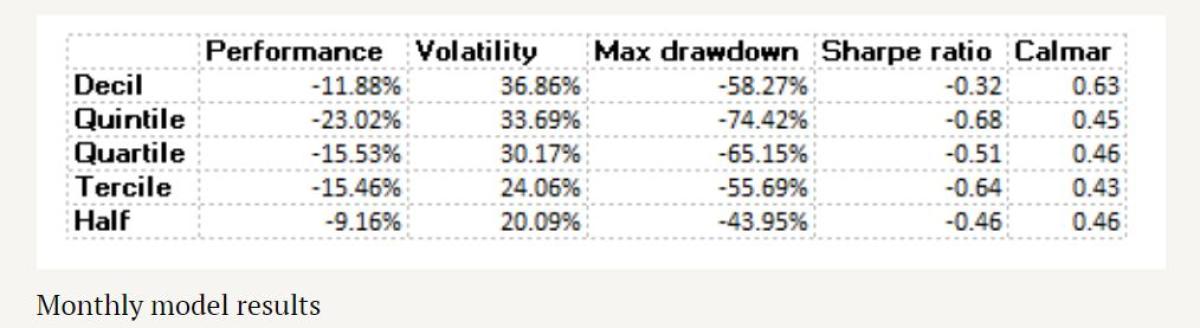

In the table below, we can observe results for all types of sorting. For better understanding, when we want to sort cryptocurrencies into deciles we take 5 bottom and 5 top cryptocurrencies. For quintiles portfolios we take 9 bottom and 9 top cryptocurrencies, for terciles we take the bottom 15 and top 15. Lastly, for halves, we take bottom 22 and top 22. Looking more closely at the results, we can observe that when we based the skewness on the last 30 days in all cases the performance is visibly negative. The Sharpe ratio is negative as well.

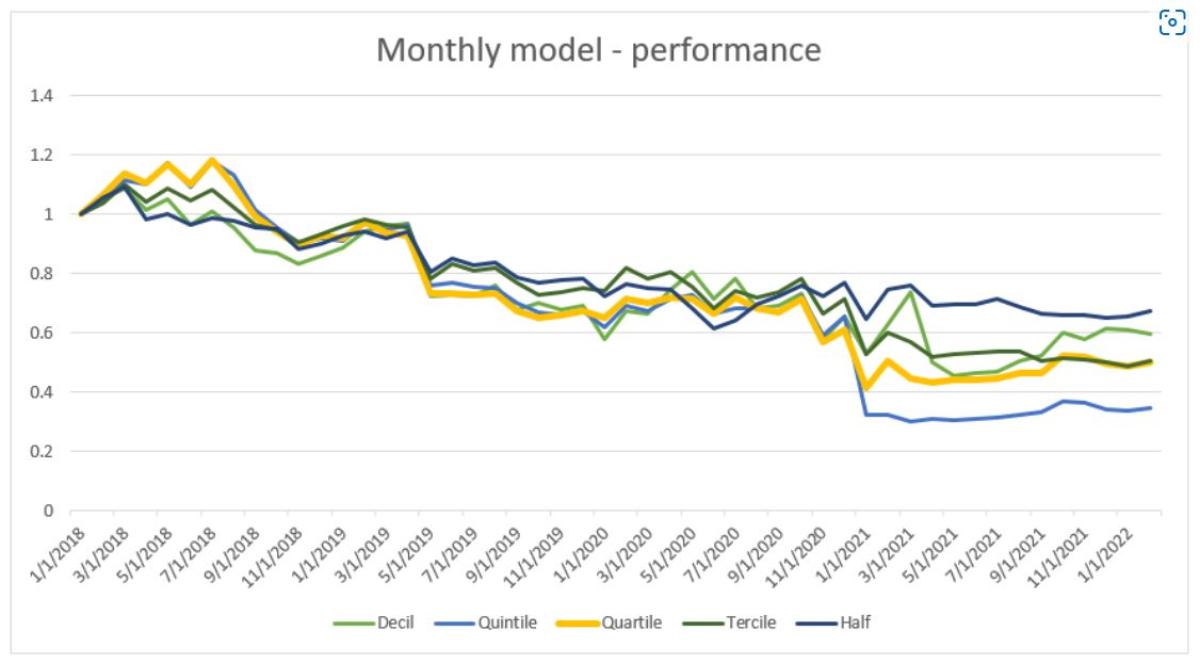

On the graph below, we can observe the evaluation of performance for our monthly model when considering sorting into quartiles. As we can see the beginning of the year 2018 looked promising. However, approximately around the end of the summer we can notice a rapid decrease in the performance. This decreasing trend continues till the beginning of the year 2021. In January 2021 we can observe that the performance of the model is stabilized and it continued at the level of approximately 0.5 for one year until the January of 2022.

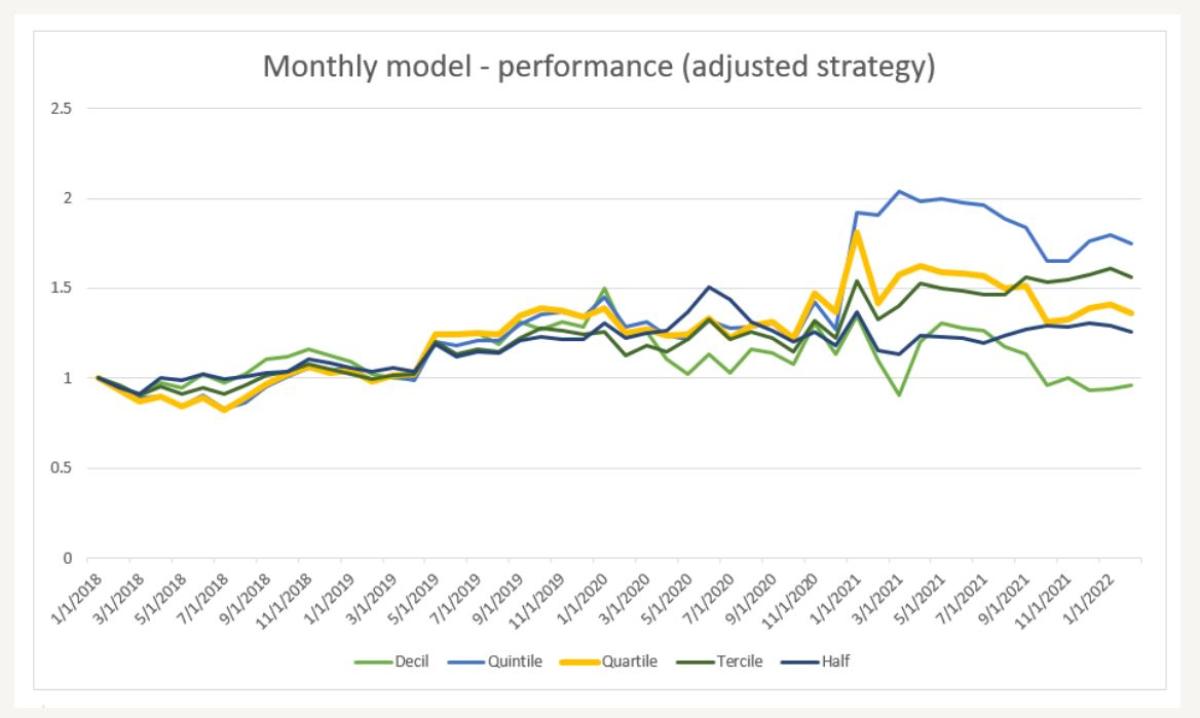

Monthly model – adjusted strategy

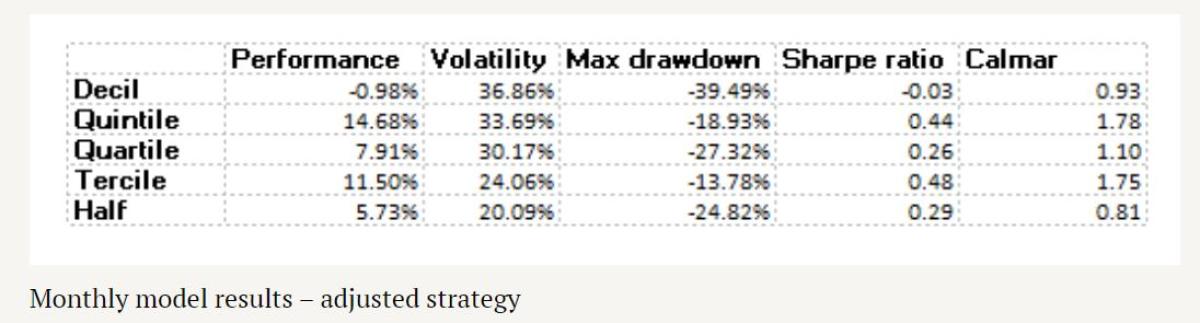

Due to the negativity of the performance, we can adjust our strategy and check the reverse rule. After sorting cryptocurrencies into deciles, quintiles, etc. we will short the bottom portfolios and long the top portfolios. After this adjustment, we can see that performance has improved. The Sharpe ratio increased for each portfolio and except for the decile portfolio, it is positive.

Usually, the skewness trading strategy uses 12 months of daily performance data to calculate a skewness measure, and the trading strategy normally goes long the most negatively skewed assets and short the most positively skewed assets (assets with lottery-like features that are usually the most over-priced). But it seems that the shorter skewness calculation period (1-month instead of 12-months) has a reversed impact on the performance of this effect in cryptocurrencies – the most positively skewed cryptocurrencies outperform.

Yearly model

In the second model, each day we calculate the skewness based on the last 360 days.

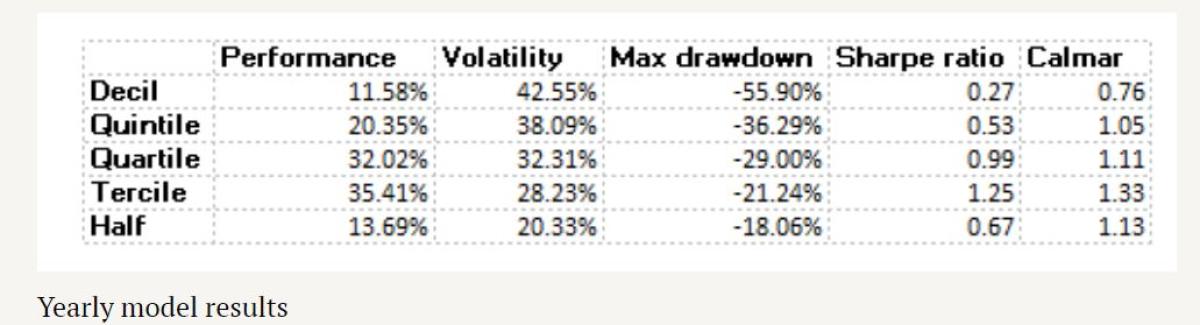

The rules: For each month, take the most recent 360-day skewness and sort cryptocurrencies into two portfolios. We can again sort cryptocurrencies into deciles, quintiles, quartiles, terciles, or halves. For illustration, let’s consider sorting cryptocurrencies into quartiles. Therefore, the first portfolio contains the 11 bottom cryptocurrencies (with the lowest skewness, the most negative). The second portfolio contains the top 11 cryptocurrencies (with the highest skewness, the most positive). Long the bottom 11 portfolios and short the top 11 portfolios. The portfolios are rebalanced monthly. In the table below, we can observe results for different types of sorting.

Looking more closely at the results, we can observe the performance is positive in all cases. However, it varies based on how many top and bottom cryptocurrencies we take. As we can see, based solely on performance results, the decile and half portfolios have the lowest performance of 11.58% and 13.69%, respectively. However, we see that the decil portfolio has the highest volatility of 42.55% and the maximum drawdown is more than -55%.

Further, the quantile portfolio has a performance of 20.35% with volatility and max drawdown of 38.09% and 36.29%, respectively. In addition, we can observe that compared to the decile portfolio, the Sharpe and Calmar ratio has increased by 0.26 and 0.29, respectively. Further, quartile and tercile portfolios have significantly higher performances of 32.02% and 35.41%, respectively. Furthermore, the volatility and maximum drawdown are higher for the quartile portfolio, representing 32.31% and 29%, respectively. For the tercile portfolio, we can observe a slight decrease in volatility to 28.23% and also in the maximum drawdown (21.24%). Lastly, we would like to point out that this portfolio has the highest Sharpe ratio of 1.25 and Calmar ratio of 1.33.

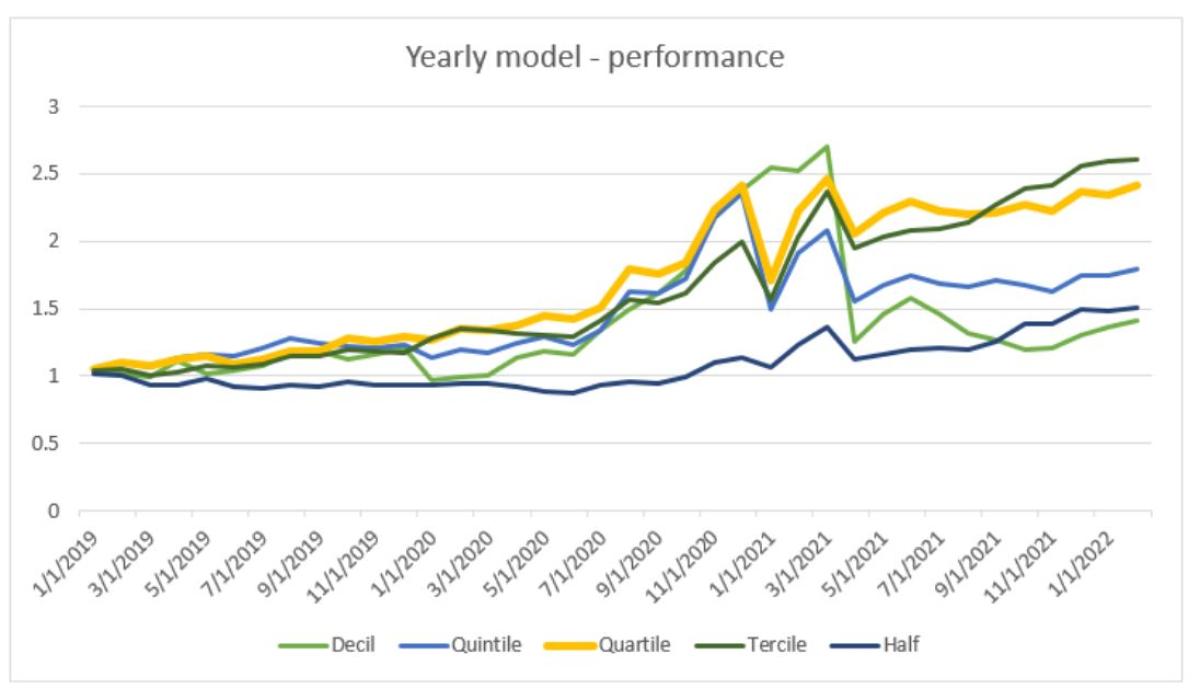

On the graph below, we can observe the evaluation of performance for our yearly model with different sorting rules, sorting into quartiles is highlighted in yellow color. The performance has a visible increasing trend for nearly all sorting rules.

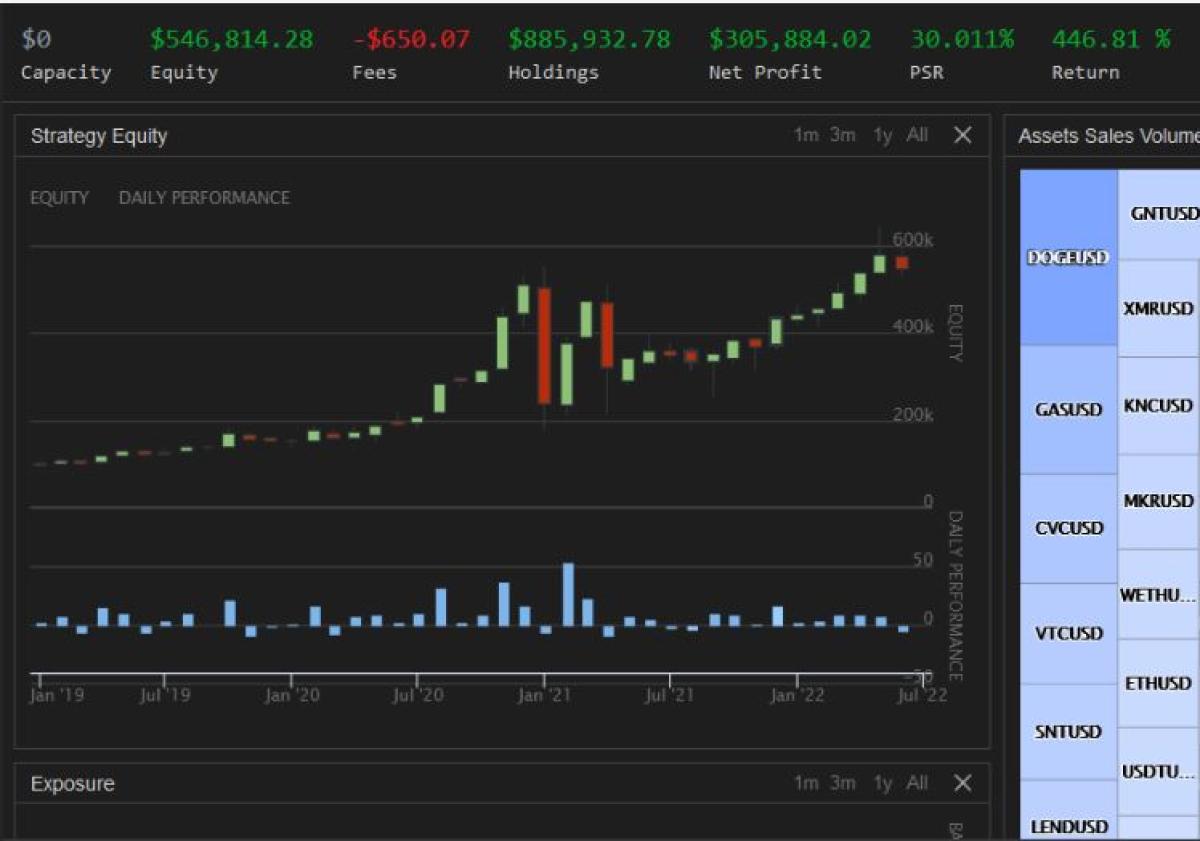

Our analysis is based on data from January 2018 to March 2022. But in the three months (April-June 2022), the cryptocurrency market recorded a period of remarkable turbulence and stress. So we have the opportunity to check the strategy’s performance in an out-of-sample setting. How does the skewness effect perform in a crisis period?

The print-screen chart shows another backtest of skewness anomaly in cryptocurrencies; this time is written in Quantconnect (the code and equity curve would be available for Quantpedia Premium and Pro subscribers at the beginning of July). We can see (examine the last three monthly bars) that despite the heavy losses in crypto markets, the long-short skewness effect still performs well.

Conclusion

In this paper, we examined the skewness of cryptocurrencies. We created two main models. The first model, called the monthly model, calculates for each day the skewness based on the last 30 days. Then, for each month, takes the most recent skewness and sorts cryptocurrencies into two portfolios. The model goes long the bottom (with the lowest skewness) portfolios and shorts the top (with the highest skewness) portfolios. The obtained results show that the performance is negative for every chosen portfolio. We decided to adjust the strategy and long the top portfolios and short the bottom portfolios. With this change, we observed a significant performance improvement.

For our second model, called the yearly model, we calculated each day the skewness based on the last 360 days. Again, for each month, the model takes the most recent skewness and calculates the monthly performance from the data. The model goes long the bottom portfolios and short the top portfolios. The yearly strategy works very well, and we have a positive performance even in the crisis period.

About the Author:

Paula Tekulová, Junior Quant Analyst, Quantpedia.

References

- https://www.investopedia.com/terms/s/skewness.asp

- www.coinmarketcap.com/charts

- List of the cryptocurrencies: ada, ant, bat, bch, btc, btg, cvc, dash, dgb, doge, drgn, elf, etc, eth, fun, gas, gno, gnt, knc, lend, loutk, itc, maid, mana, mkr, neo, omg, pay, powr, ppt, qash, rep, snt, usdt, usdt_eth, usdt_omni, vtc, weth, wtc, xlm, xmr, xrp, xvg, zec, zrx