By Kai Wu, founder and CIO of Sparkline Capital.

Executive Summary

Venture capital has delivered great historical returns but is illiquid and hard to access. Fortunately, innovation does not occur only at venture-backed startups. We replicate venture capital returns using liquid small-cap public equities and find the underlying innovation premium also exists at large innovative firms. We also show that crypto tokens can provide a liquid complement to blockchain venture equity.

Introduction/Cradle of Innovation

Venture capital plays a leading role in the story of American innovation. Venture capital was instrumental in the birth of legendary Silicon Valley firms such as Apple and Google. Venture-backed firms ushered in the information revolution, cementing America's status as the hub of global innovation.

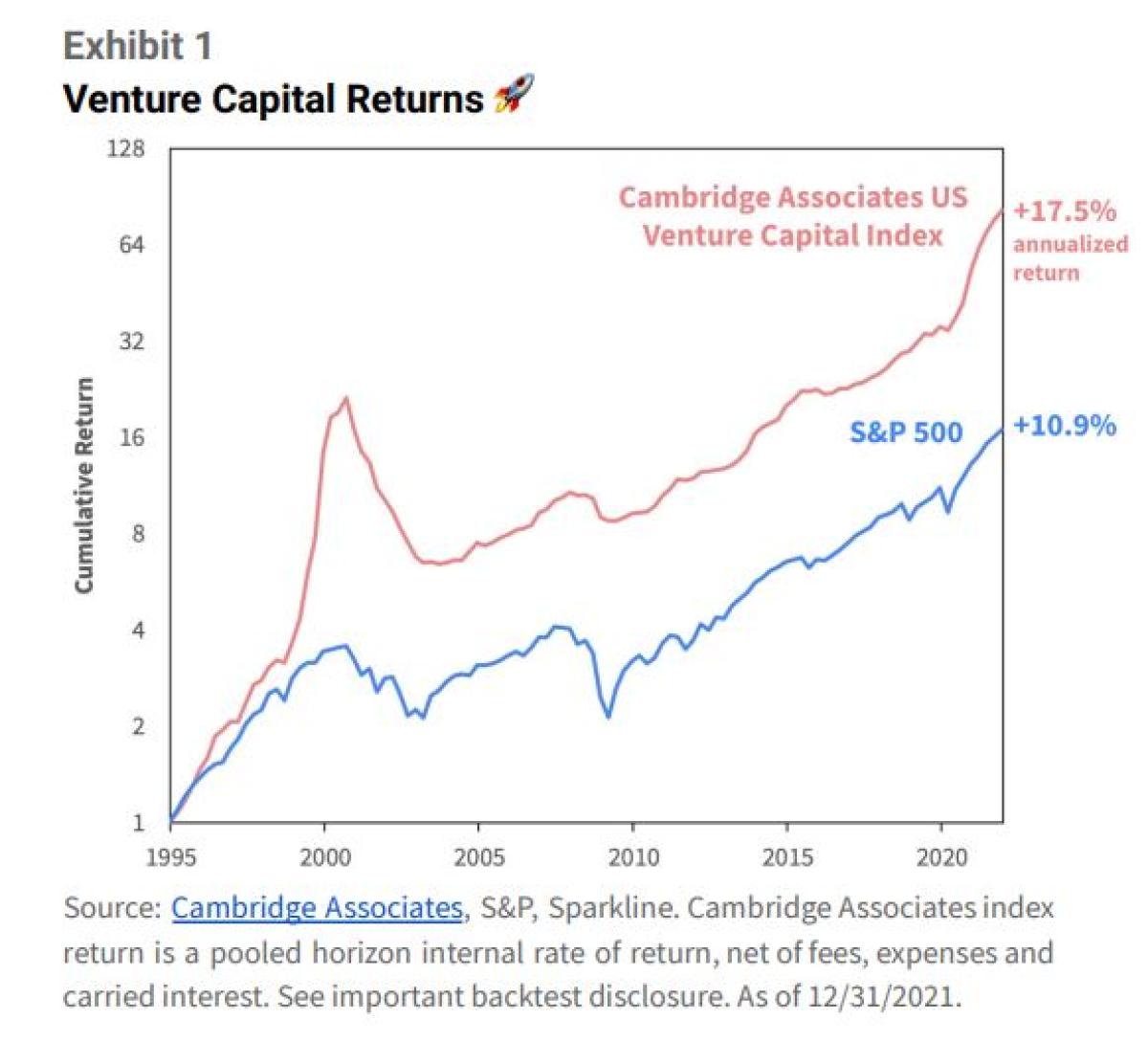

Investors in venture capital funds have been very generously rewarded. Since 1995, an index of venture capital funds has returned +17.5% per year, trouncing the stock market. The performance of top quartile venture funds has been even more astronomical (~40% per year).

This impressive track record fueled the meteoric rise of the $2 trillion venture industry. In 2021, US venture funds raised a record $139 billion across 1,000 funds. In just the first half of 2022, despite a collapse in tech stocks, these managers have already raked in $122 billion.

Venture Glut

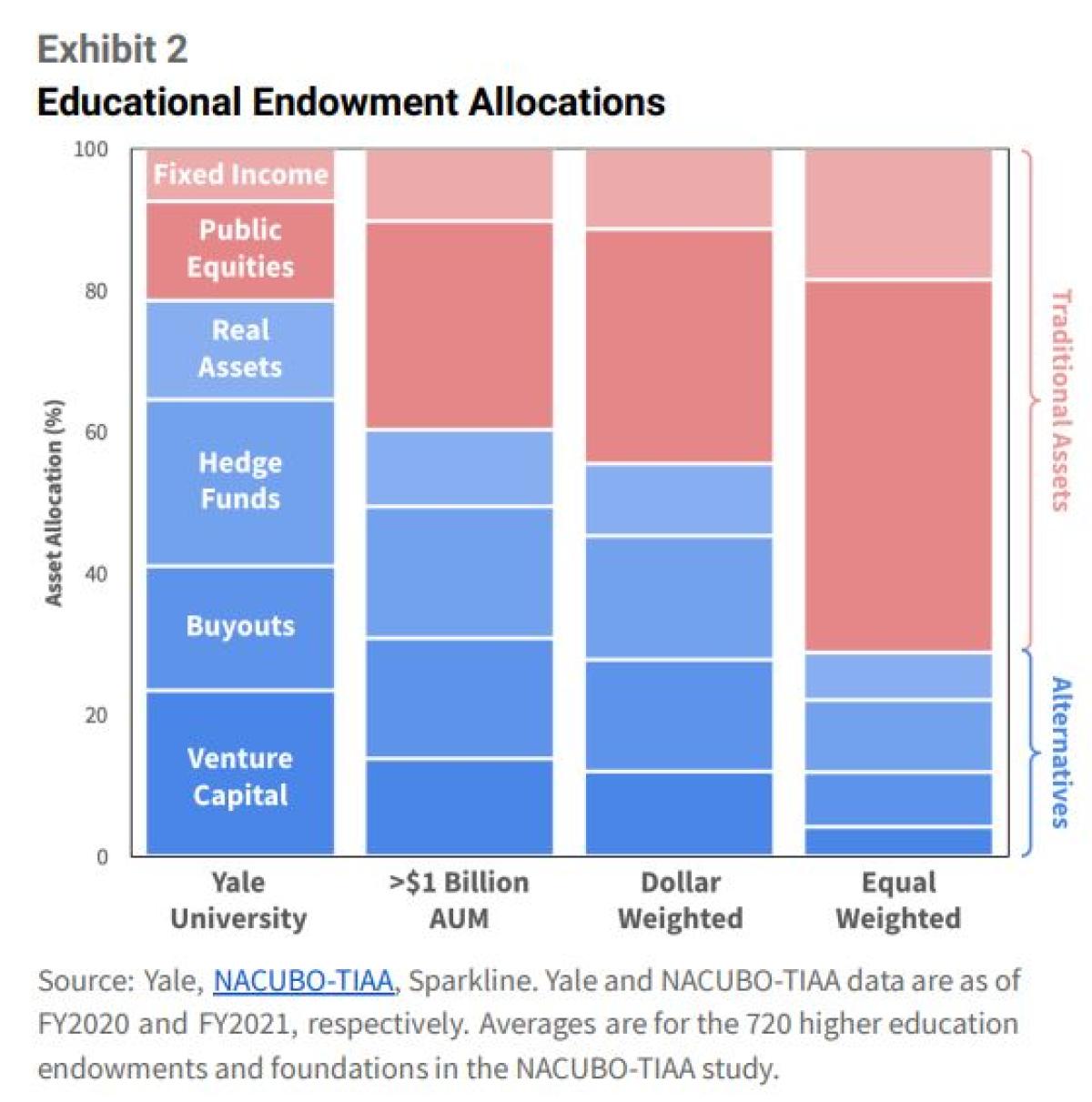

Venture capital is especially favored by elite institutional investors. This is largely due to the influence of David Swensen, the late CIO of Yale University, who popularized a model favoring illiquid alternatives like venture capital.

Yale’s 24% venture capital allocation is the crown jewel of the endowment world. Other institutions, most notably Yale’s multi-billion dollar peers, have also built huge venture allocations. This overweight to venture capital (and other alternatives) has been a key driver of their outperformance relative to smaller institutions over the past few decades.

However, the ongoing tech stock implosion has left many investors overexposed. As the tide goes out, the drawbacks of large illiquid allocations are glaring. Venture funds often lock capital for a decade or more, creating headaches for investors trying to adjust to volatile market conditions.

Making matters worse, venture managers are notoriously slow to write down their portfolio positions in downturns. While early-stage technology stocks are down 60 to 80%, many venture funds have yet to implement markdowns. Stale prices relative to a shrinking denominator exacerbates the overallocation.

Allocators are not the only ones stuffed to the gills. Venture managers have been raising increasingly massive funds at an accelerating pace (i.e., every 1.6 years). These funds have been raised faster than they can be deployed, with the global industry now sitting on $539 billion in dry powder. With more capital than opportunities, it may take years to work through this glut.

Venture capital has been a great boon to investors, but the current glut is forcing investors to reexamine its role in their portfolios. While venture investing is often seen as a mostly qualitative endeavor, we will show that its broad properties can be replicated using quantitative methods.

Replicating Venture

Venture Data 🤓

Our first goal is to show that the returns of the venture index can be replicated using liquid public equities. This not only helps us unpack the source of venture returns but also offers a potentially valuable tool for investors seeking venture-like exposure in a liquid and accessible vehicle.

We start by assembling a database of venture deals. Venture traditionally consists of a series of financing rounds, starting with Series A. Investments before Series A are called angel or seed rounds. These are generally the purview of founders, friends and family, or smaller venture firms.

Our analysis excludes angel and seed deals. While there are of course great opportunities at these very early stages, the venture index is dollar-weighted and thus driven by large institutional funds. Large funds tend to invest in later-stage startups, as smaller seed checks do not move the needle.

Ignoring seed deals helps reduce noise. Compared to public stocks, private firms have much less reliable data as they are not subject to standard regulatory and financial disclosures. Deal terms are often undisclosed and survivorship bias is a big concern, especially in the high-turnover startup world.

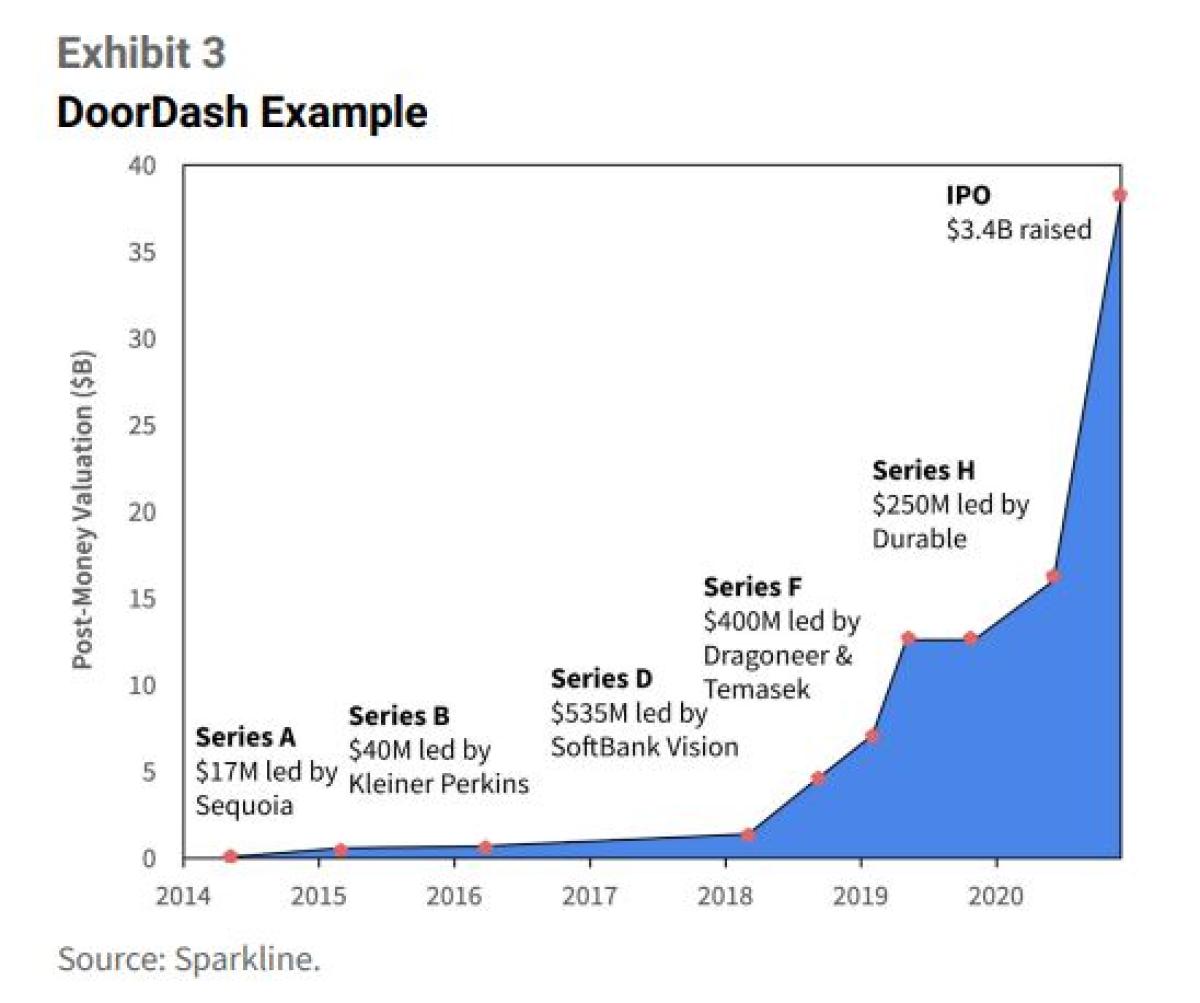

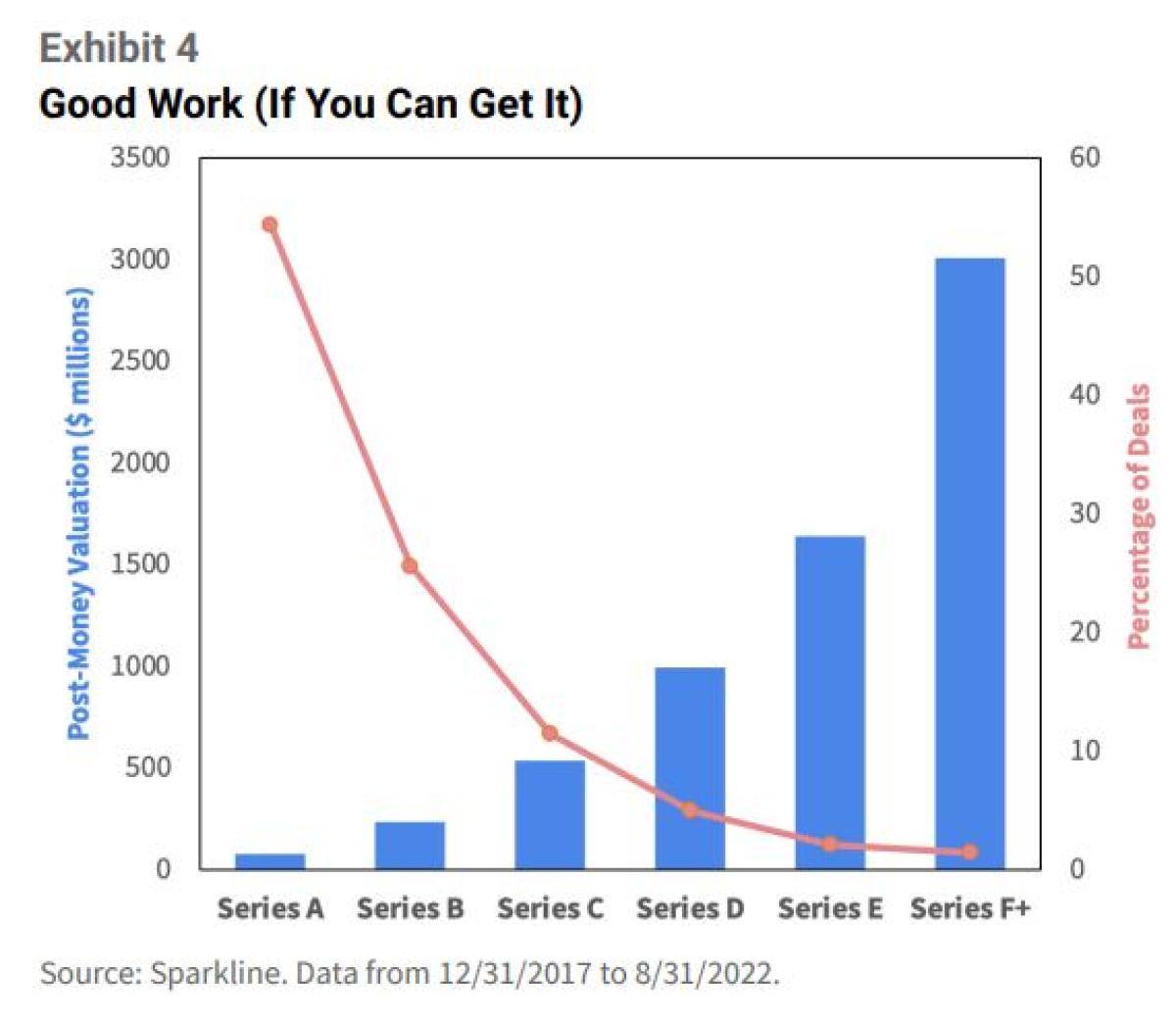

With this in mind, let’s start with a simple example. Exhibit 3 shows DoorDash’s path to its initial public offering (IPO). Founded in 2013, its 2014 Series A led by Sequoia Capital valued it at $72 million. From here, it raised $2.5 billion in venture funding over several years. Its final venture round valued it at $16 billion, six months before its $32 billion IPO.

While DoorDash is an idealized example, it is generally true that valuations tend to increase with each successive stage of financing. However, given their high failure rate, only around 50% of startups make it to each successive funding round (e.g., only ~⅛ make it to Series D).

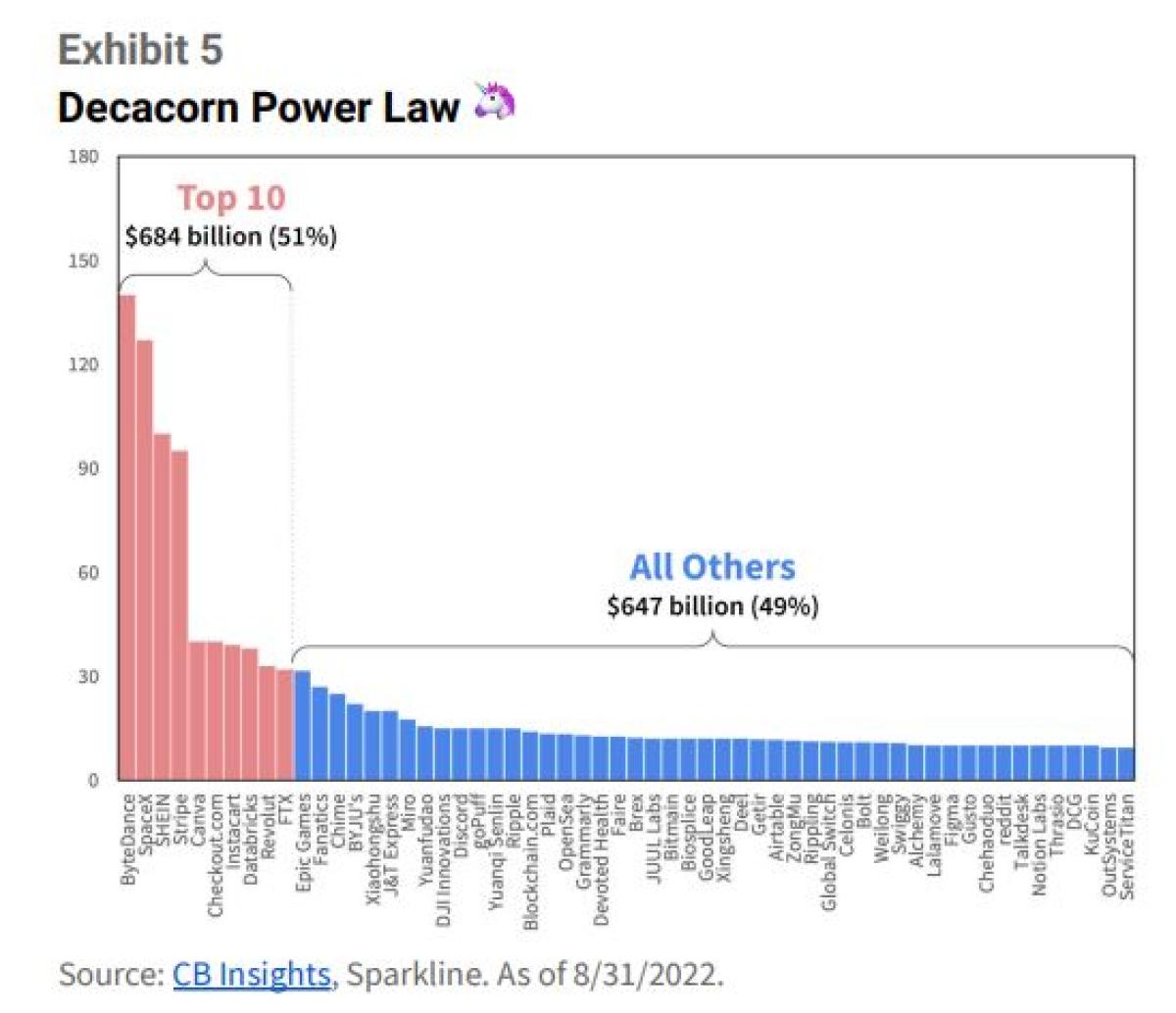

This underscores the famous “power law.” Most startups fail but the few that succeed can produce generational returns. Exhibit 5 shows the valuations of private venture-backed “decacorns” (i.e., $10 billion firms). The top ten are more valuable than the other 48. This power law exists not only for decacorns but also the startup world in general.

We also have data on the investors leading and participating in each financing round. The next table shows the most active venture investors by deals led over the past few years.

We see the impact of prolific new entrants into the space. Tiger Global and Coatue are so-called “crossover funds” that recently expanded from liquid markets into private equities. Meanwhile, the Softbank Vision Fund doled out a staggering $100 billion to startups like WeWork. These funds’ aggressive deployment played a big role in the recent valuation run-up.

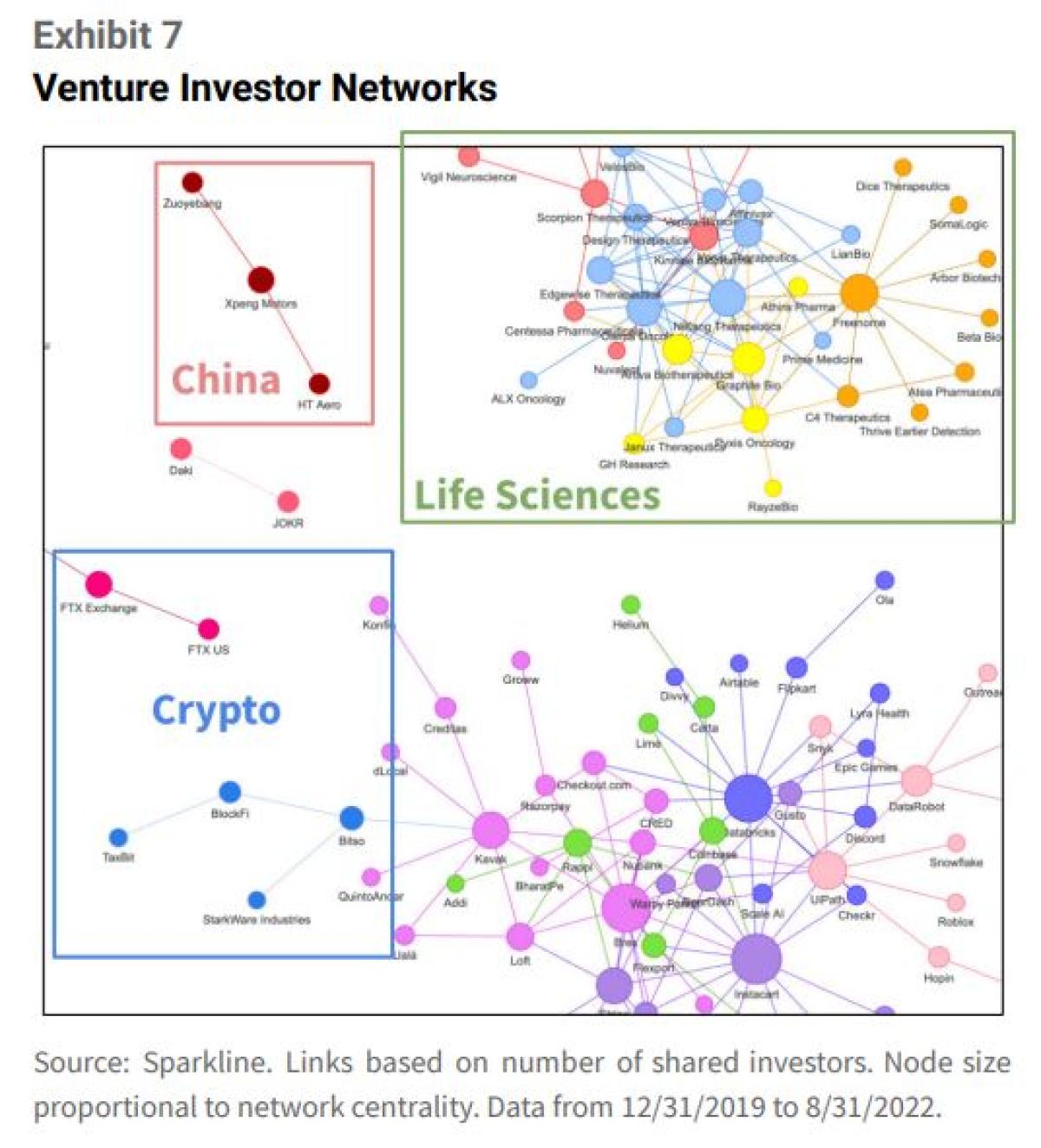

Venture capital is largely a relationship game. Venture firms source deals through their personal networks and invest alongside like-minded funds. Startups partner with investors based, among other things, on relationships and industry connections. Such network effects are a major reason for the rise of Silicon Valley as an innovation hub.

The next exhibit maps out the startup ecosystem from the perspective of investor networks. Venture funds often have specific investment focuses and tend to do deals with other funds that share their theses. This causes clusters to emerge around themes such as life sciences, crypto, and China.

Factor Exposure

Now that we have a handle on the data, let’s study the three basic characteristics of venture-backed startups.

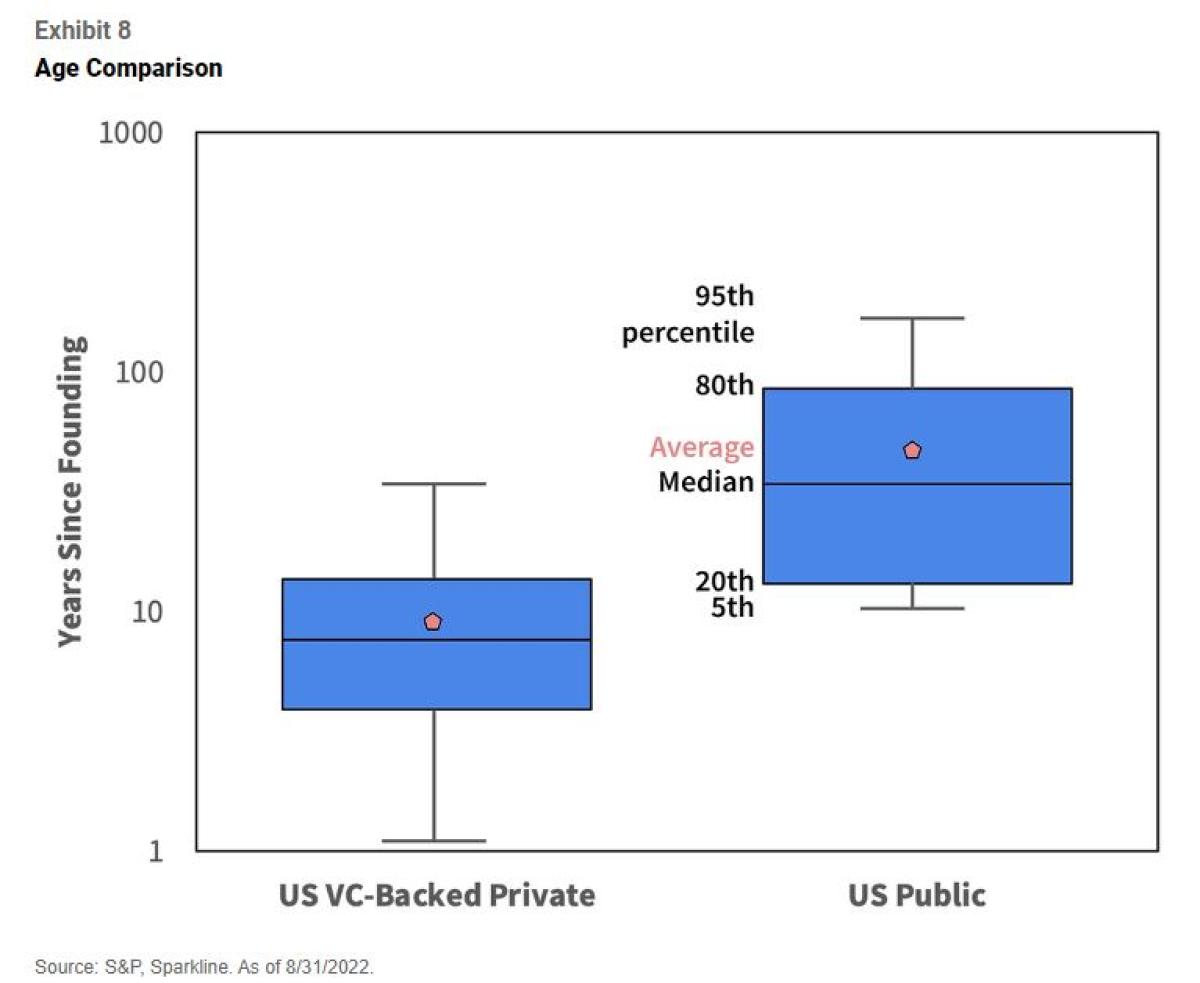

👶Young: Startups are by definition young companies. The next exhibit shows the age distribution of venture-backed private firms on a logarithmic scale. For comparison, we also show the age distribution of publicly listed US companies.

The median venture-backed startup is 8 years old, compared to 34 years old for public firms. Startups generally wait until they reach a certain maturity before listing on an exchange, a period which has lengthened over the past few decades (the median age of US firms at IPO rose from 7.9 to 10.8).

Of course, there are many exceptions. The oldest 20 percent of venture-backed startups are around the same age as the youngest 20 percent of public firms. In particular, the recent SPAC boom has brought a lot of startups to the public markets much sooner in their lifecycle.

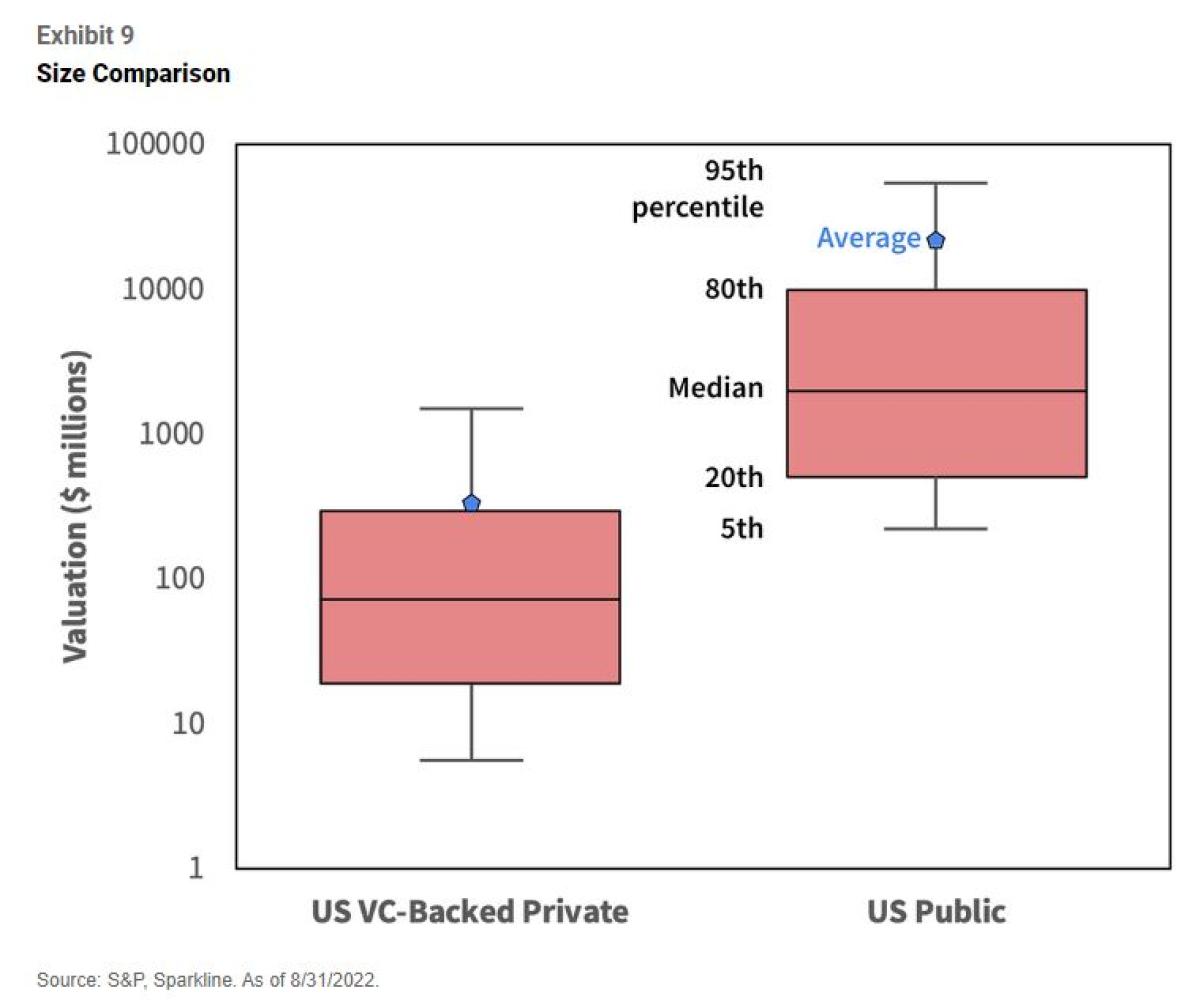

🐜Small: A related characteristic is company size. Exhibit 9 compares the valuations of US venture-backed private firms and public companies (again on a logarithmic scale).

Venture-backed private firms tend to have smaller equity capitalizations than public firms. However, there is huge dispersion. For example, SpaceX is valued at $127 billion, which would make it the 58th largest US stock if listed today (bigger than AT&T, Goldman, and Netflix). Conversely, there are over 800 US stocks with market caps under $1 billion.

While the power law is conventional wisdom in venture, it is actually more pronounced in the stock market. The average startup valuation is $290M against a median of only $70M, but this ratio is even more extreme in stocks ($14.5B v. $2B). This reflects the rise of the superstar firms from Monopolies Are Distorting the Stock Market (Sep 2020). Apple is a $2.5 trillion company that alone comprises 7.3% of the S&P 500!

🚀Fast-Growing: The third salient characteristic is fast growth. The startup world is “up or out.” Companies either grow and are rewarded with richer valuations or they die. Given their low hit rate, venture funds need their winners to be home runs in order to earn a decent return at the fund level. Most venture investors won’t even consider startups without significant growth potential.

Thematic Exposure

“The myth is that venture capitalists invest in good people and good ideas. The reality is that they invest in good industries.”

🏭Bob Zider

Venture firms don’t just blindly finance all high-growth startups. Instead, they tend to focus on firms innovating in specific technological domains (e.g., PCs, internet, crypto).

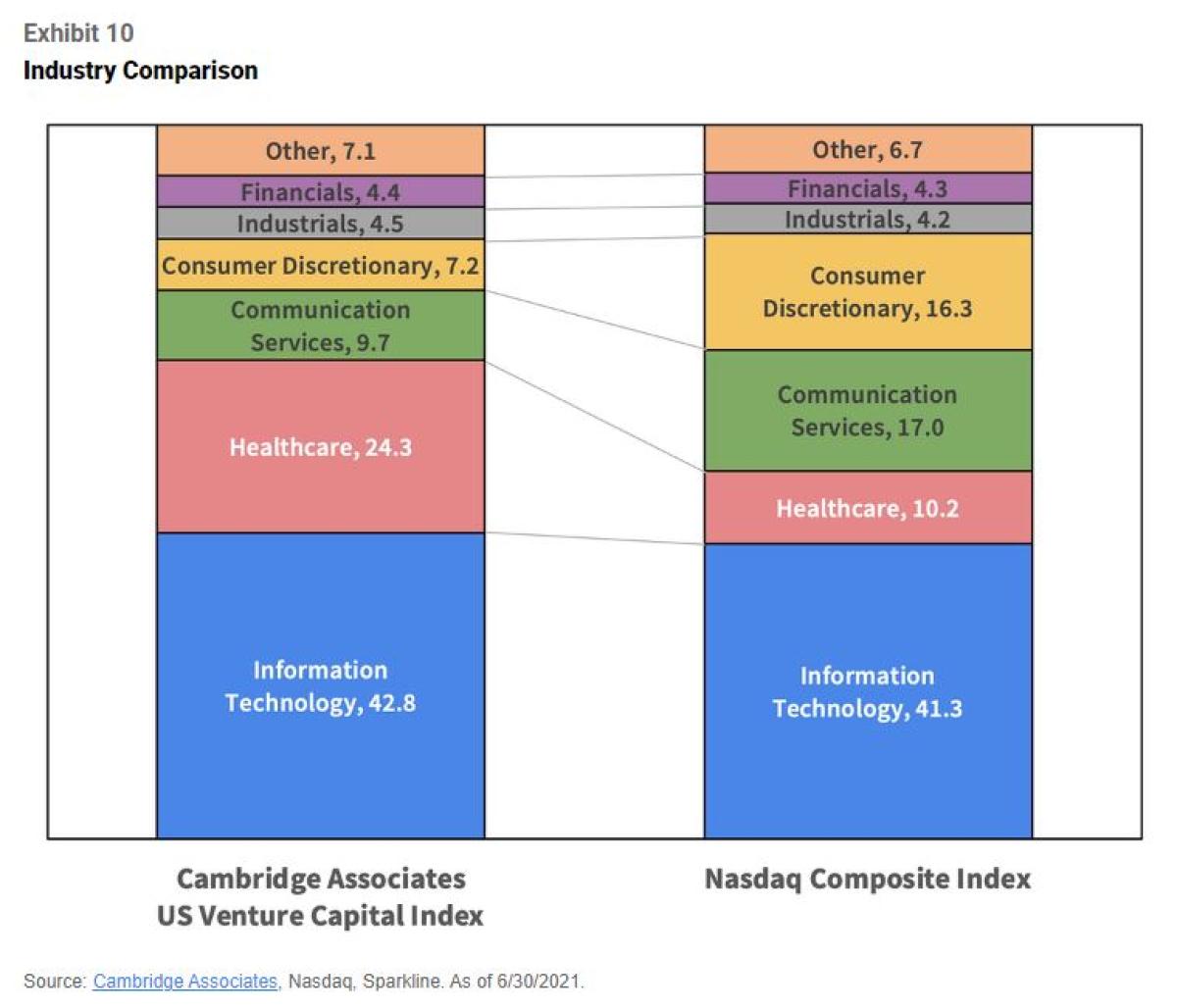

One simple way to classify companies is by industry. The next exhibit compares the GICS industry exposure of the Cambridge Associates US Venture Capital Index to that of the Nasdaq Composite.

Both venture capital and Nasdaq have around 42% in tech. However, this comparison is not very revealing. In Value Investing Is Short Tech Disruption (Aug 2020), we argued that investors should not conflate tech and innovation. After all, not all tech companies are disruptive (e.g., IBM), and disruptive firms exist in all industries (e.g., Tesla, Amazon).

We believe that unstructured data can provide a more granular way to classify firms by technological theme. Our last paper, Investing in Innovation (Apr 2022), clustered technologies by applying natural language processing (NLP) to patent abstracts. This section applies a similar technique to the business descriptions in our startup database.

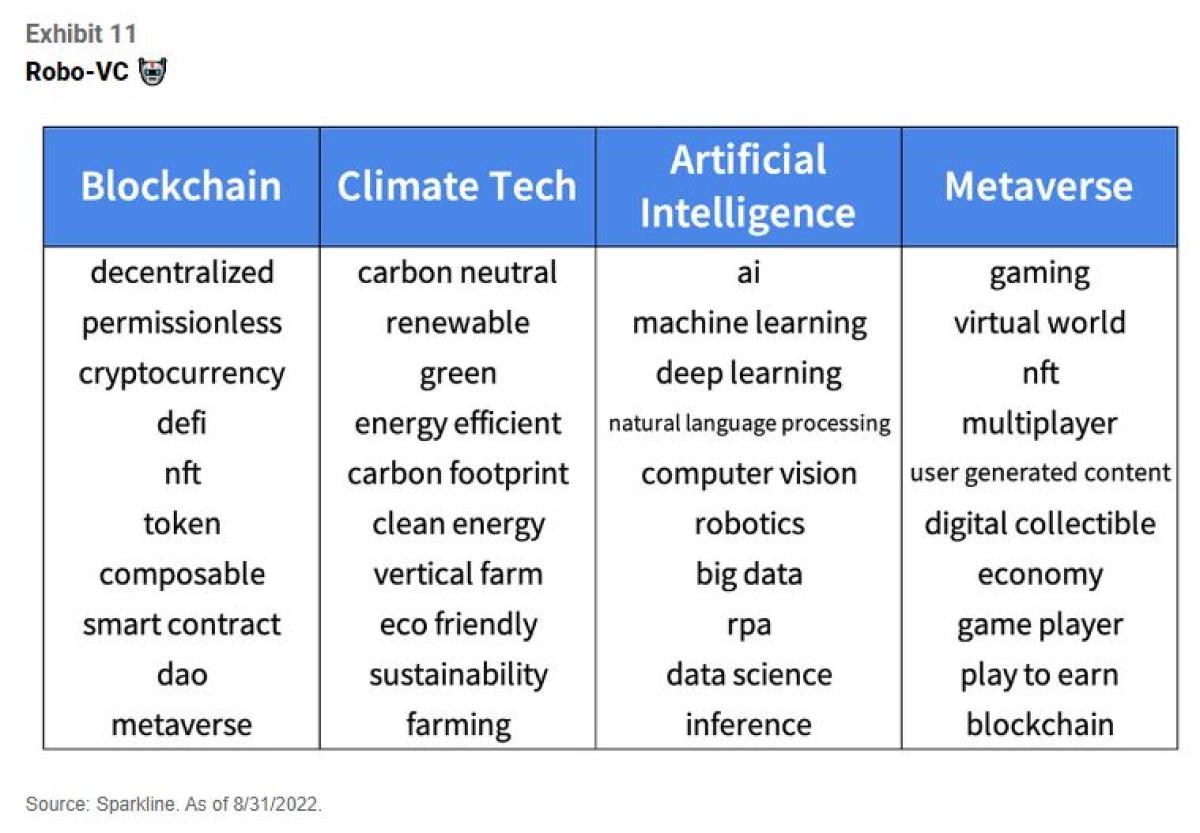

The algorithm starts by learning the relationship among concepts mentioned in the business descriptions. Exhibit 11 lists terms associated with four popular themes: blockchain, climate tech, artificial intelligence, and metaverse.

Our model produces intuitive results. For example, it correctly associates terms like “NFT” and “smart contract” with the blockchain. The model also successfully deciphers multi-word phrases like “carbon neutral” and acronyms like RPA (“robotic process automation”).

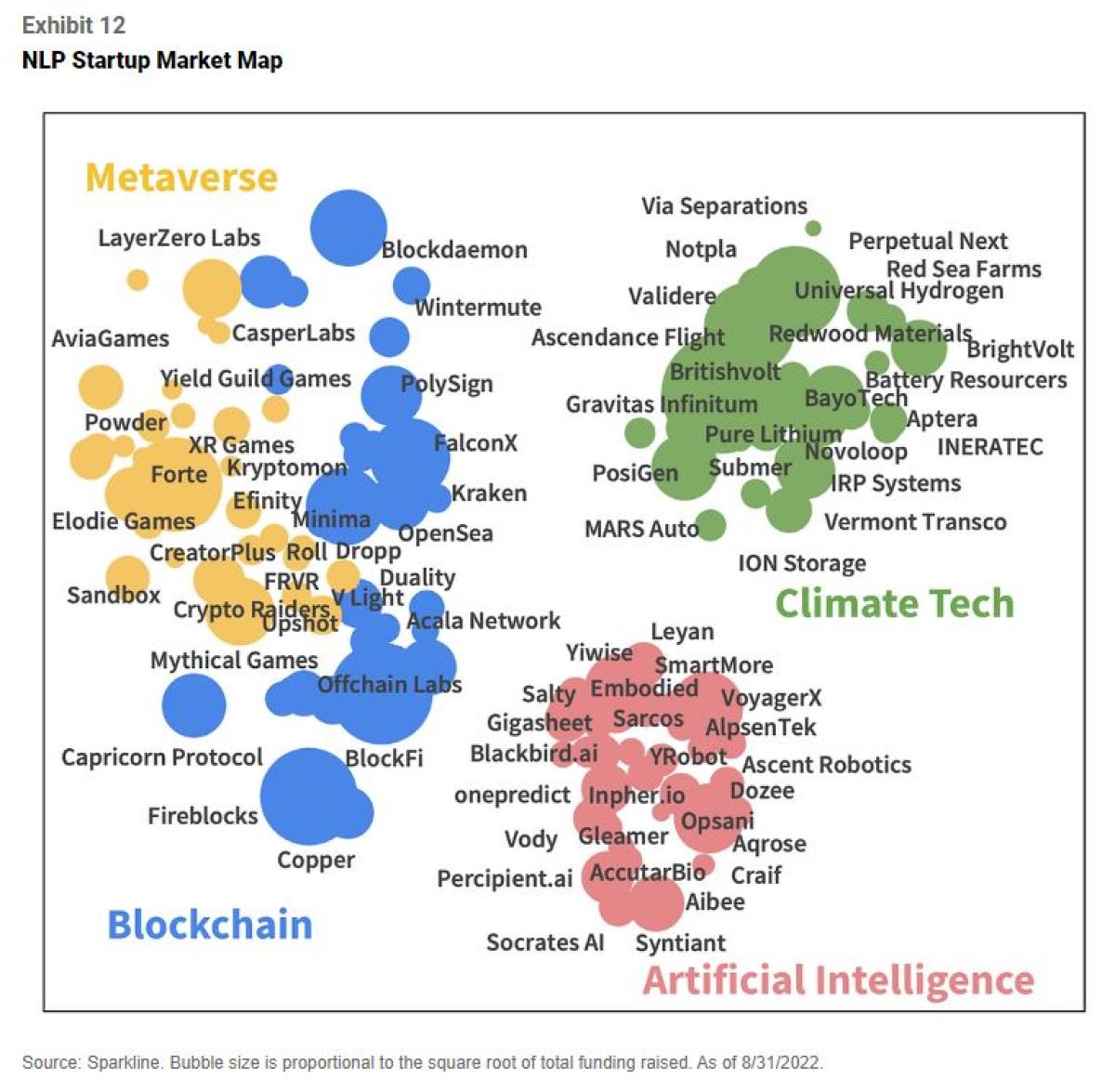

Now that our model speaks “startup jargon,” we’ll have it analyze the relationship among startups based on their business descriptions. We use machine learning to build the market map below, which identifies startups with exposure to each of these four themes. Bubble size is proportional to total venture funding.

The position of each startup is based on the similarity of its business description to those of other startups. For example, the model puts Fireblocks and Copper, which are both crypto custody platforms, near each other.

Proximity also matters at the theme level. The model places metaverse and blockchain startups nearby due to their shared association with blockchain gaming and NFTs. On the other hand, climate tech and artificial intelligence form distinct clusters.

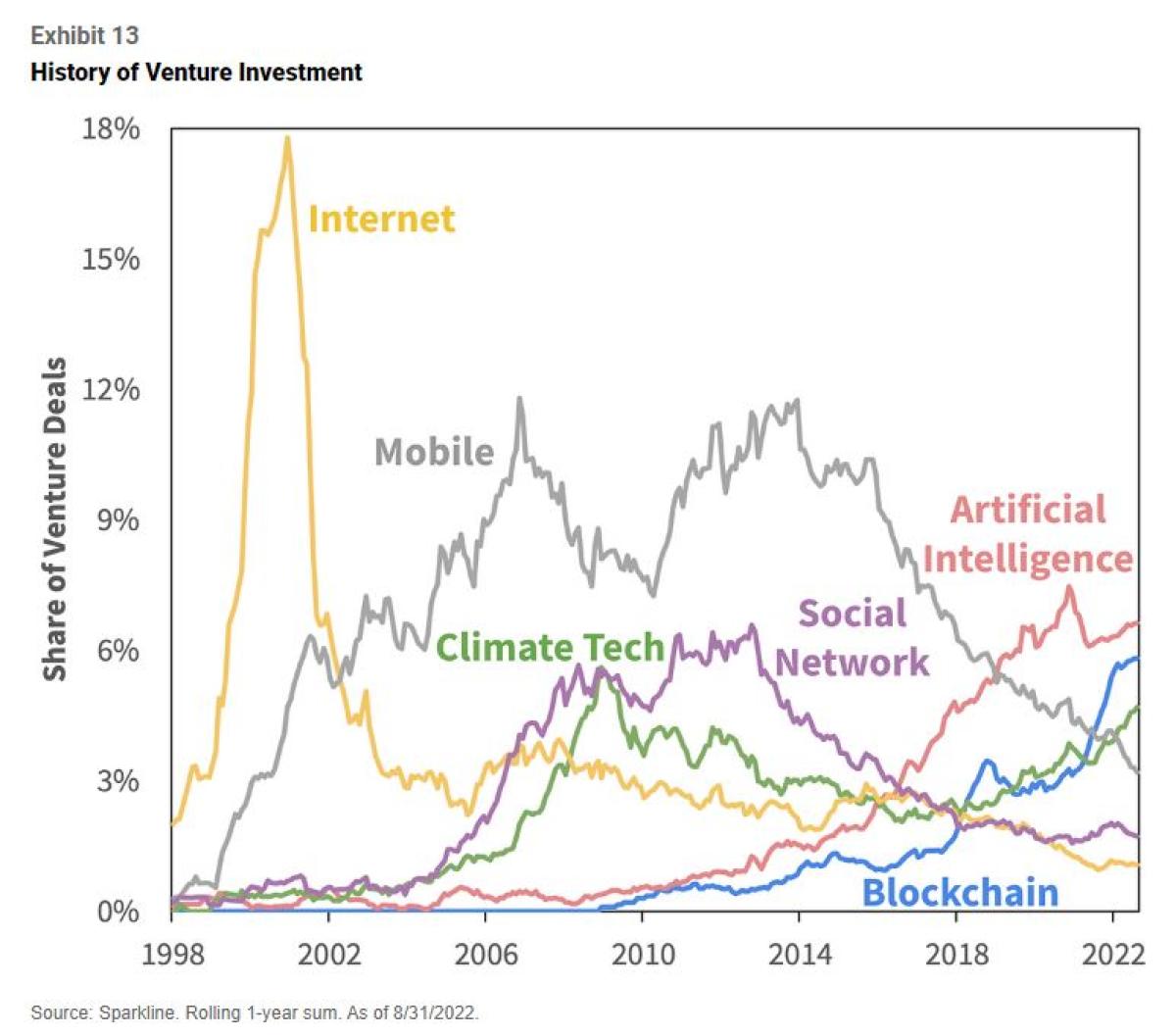

We now have a way to cluster firms innovating in similar technologies. Next, we explore how venture investment in each technology cluster evolves over time. We construct rolling one-year windows based on deal announcement dates and calculate the share of deals (and dollars) venture firms direct at each theme.

In the dot-com bubble, venture capital firms threw money at internet companies. Next, Blackberry and iPhone ushered in the mobile age. Then, Facebook’s success sparked a wave of investment into social networks. Artificial intelligence grew steadily over the past decade, while blockchain burst on the scene a few years ago. Climate tech investment faded after an initial burst but is now seeing a resurgence.

Our venture database complements the patent data from Investing in Innovation (Apr 2022) well. Patents have a much longer history and are more relevant for larger firms. On the other hand, venture data is more timely and offers insight into small-firm and non-patented innovation (e.g., trade secrets and open source).

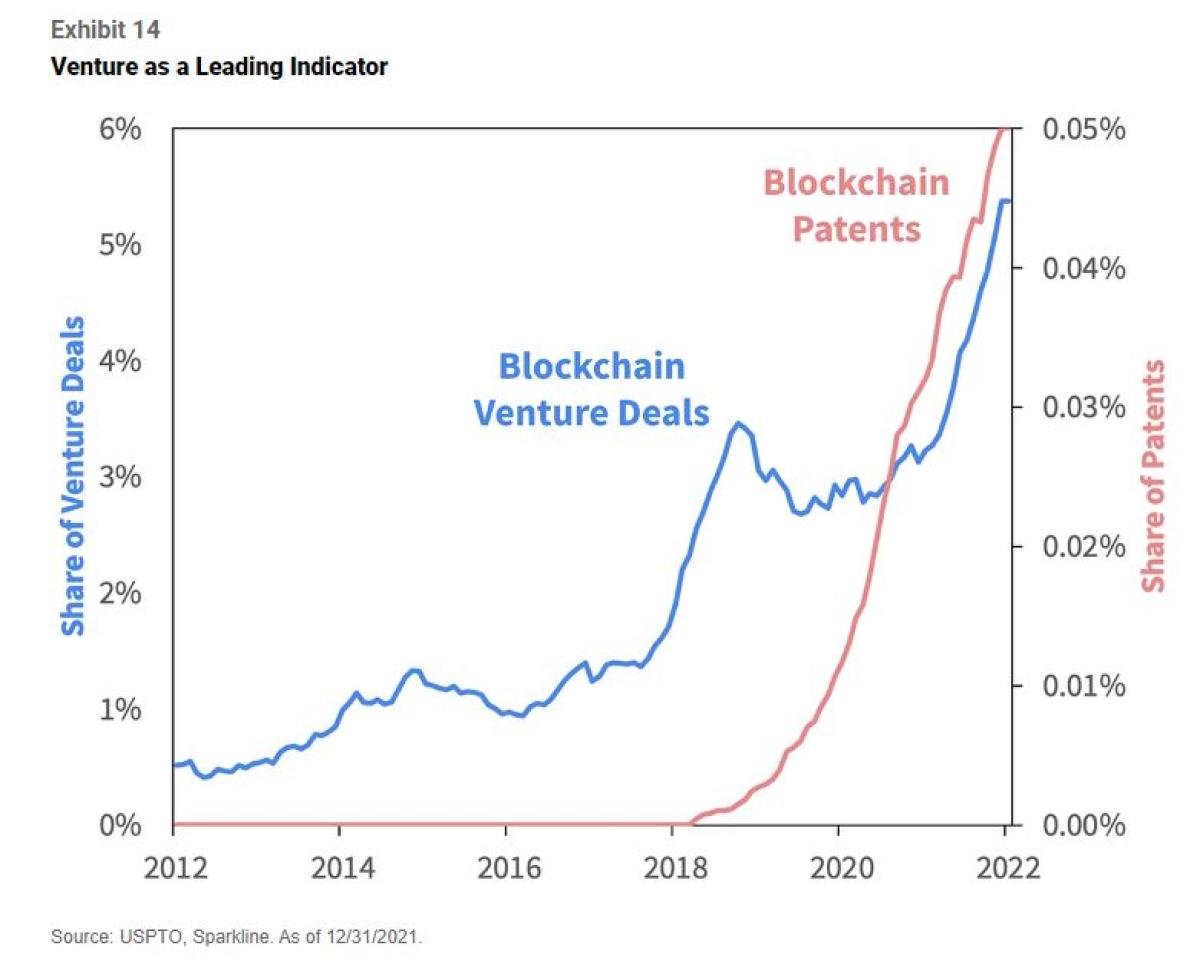

We see the more timely nature of venture investment in the following case study of blockchain technology. Venture funds were ramping up investment in blockchain startups years before blockchains appeared in the patent corpus.

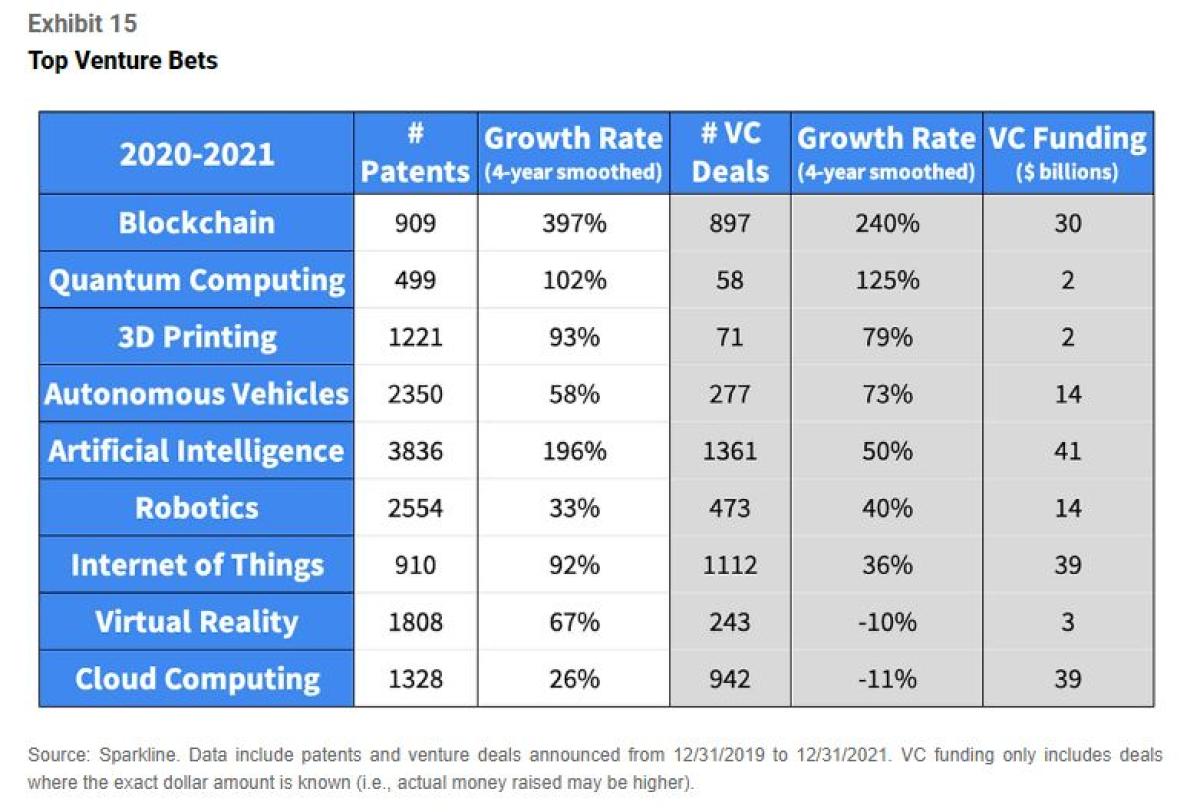

In Investing in Innovation (Apr 2022), we built a simple model to identify technologies trending in patent data. We showed the first few columns of Exhibit 15, which lists the top trending technologies. We now reproduce the table with the same technologies but add three new columns in gray.

Venture firms are extremely bullish on blockchain. They are also bullish on quantum computing and 3D printing, albeit from a much lower base. They are continuing to invest in the established sectors of autonomous vehicles, AI, robotics, and Internet of Things (IoT). However, venture investment in virtual reality and cloud computing has cooled off.

Replicating Venture 🦄🦄

“[T]he results push against the view that private equity adds value relative to passive portfolios of similarly selected public equities.”

🎓Erik Stafford, Harvard Business School professor

Private equity replication has gained some attention the past several years. While buyout funds have historically beat the market, they are illiquid, opaque, and expensive. Some have argued that public stocks can be used to replicate the returns of buyout funds with more investor-friendly terms.

Researchers, such as Verdad (2015) and Stafford (2015), have found that private equity buyout funds tend to target small, cheap, and levered firms. They build portfolios of public stocks with these characteristics. They find these portfolios are able to reproduce the returns of the private equity index.

We replicate venture capital using a similar approach but target stocks with a different set of characteristics. As we showed, venture funds tend to invest in firms that are:

-

👶 Young

-

🐜 Small

-

🚀 Fast-growing

-

🧬 Innovative

Our replication strategy buys liquid public stocks with these four characteristics. We select stocks that are in the US small-cap index (e.g., Russell 2000), bottom half of age, and top half of growth (defined using a composite of multiple growth metrics).

For innovation, we follow the methodology introduced in Investing in Innovation (Apr 2022). First, we build a rotating list of the ten technologies receiving the greatest increase in venture capital investment each period. Next, we use NLP on 10-K business descriptions to identify the public companies investing in these trending technologies.

We apply a market-cap weighting scheme to mirror the construction of the S&P 500 and Cambridge Associates US Venture Capital indexes. Our replication strategy currently holds 81 stocks. Some examples are shown below.

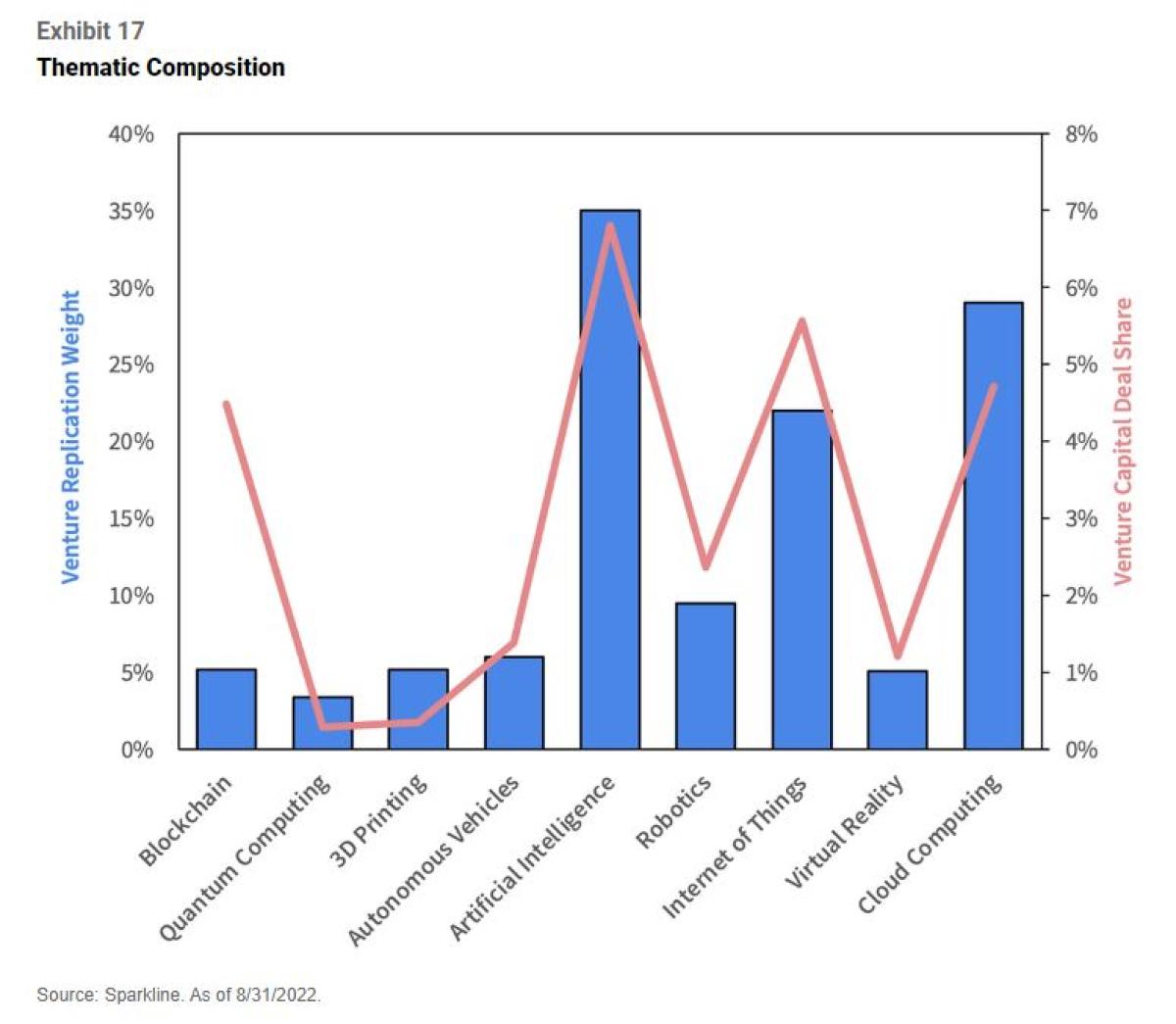

Let’s next explore the portfolio's thematic composition using the technologies from Exhibit 15. The portfolio’s thematic exposure closely matches the level of venture funding. The two series have a robust 85% correlation.

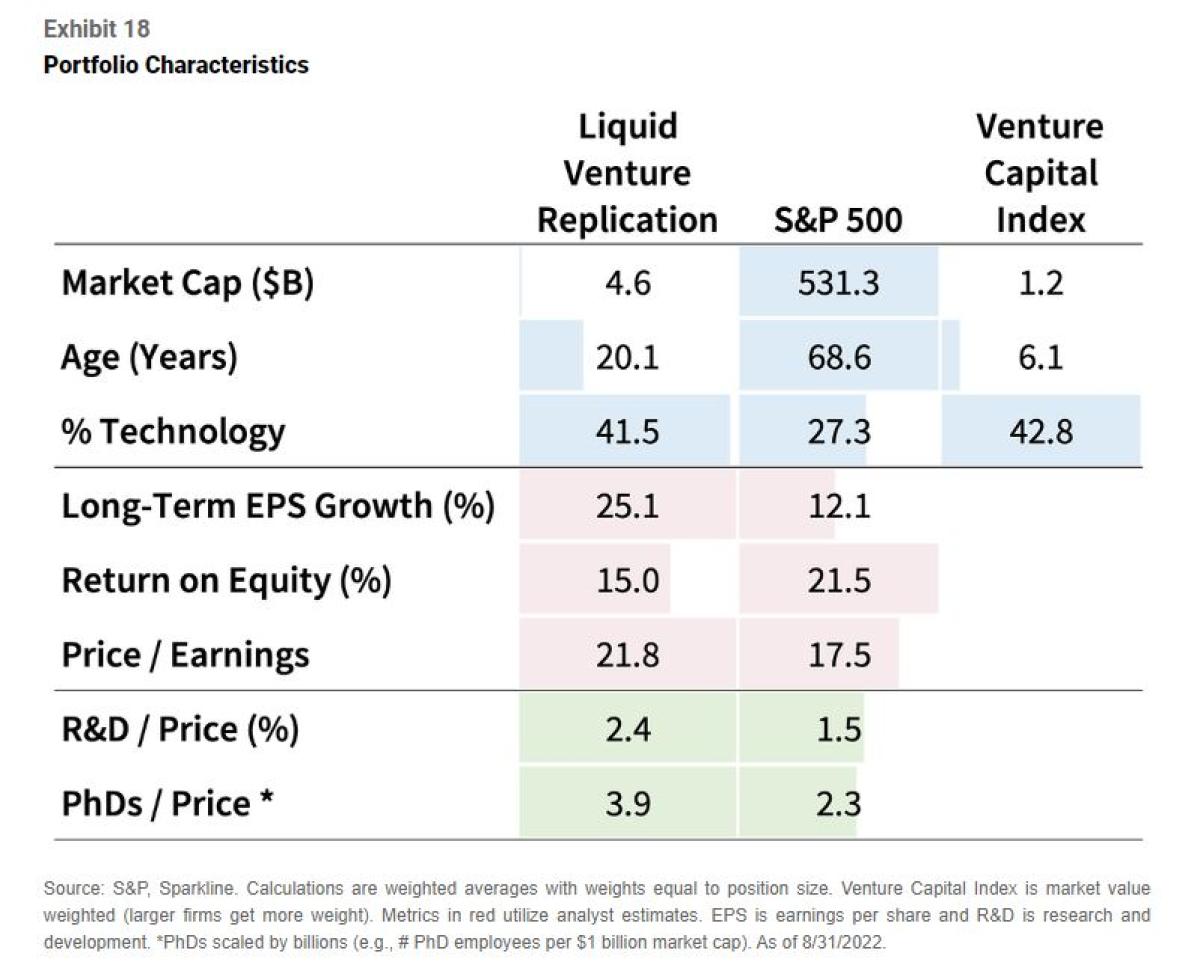

The big exception is that the portfolio is relatively light on blockchain. As we will show later, very few crypto companies are publicly listed. Investors seeking blockchain exposure should instead consider venture capital or crypto tokens. The next table compares the factor exposures of our venture replication to that of the S&P 500 and US venture capital. We show basic descriptive statistics in blue , fundamentals in red , and intangible value factors in green .

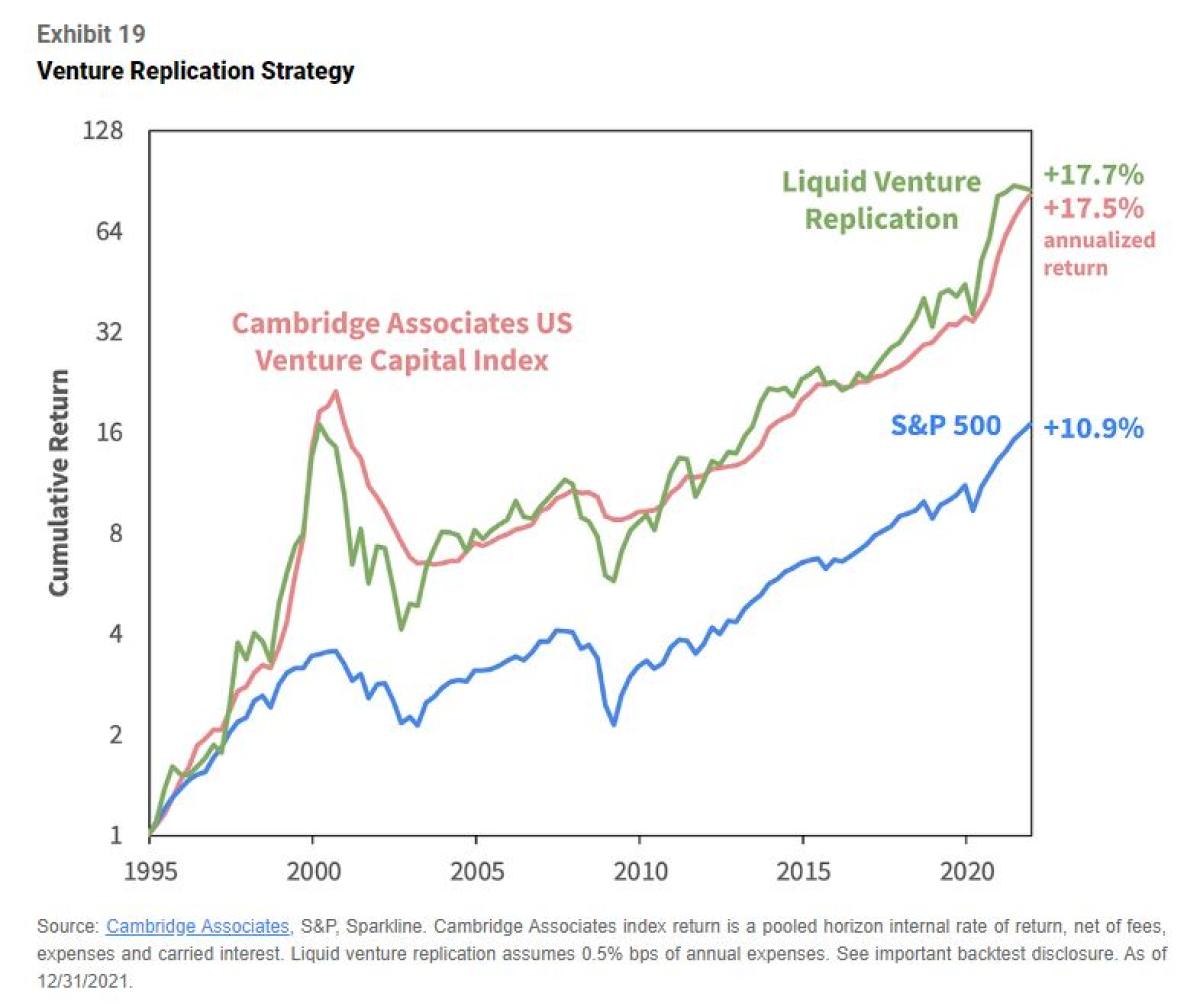

The replication holds smaller, younger, faster-growing, and more intangible-intensive companies than the S&P 500. These firms tend to be more expensive and less profitable. Compared to the venture capital index, the replication holds larger and more mature firms. But, as we will see, these mismatches do not make a huge difference in returns. We next apply our portfolio construction rules back through time. The strategy buys a monthly-rebalanced portfolio of stocks with exposure to the four factors. Exhibit 19 compares its performance to the Cambridge Associates US Venture Capital Index. We add a 0.5% annual expense ratio to the replication since the venture capital index is net of fees.

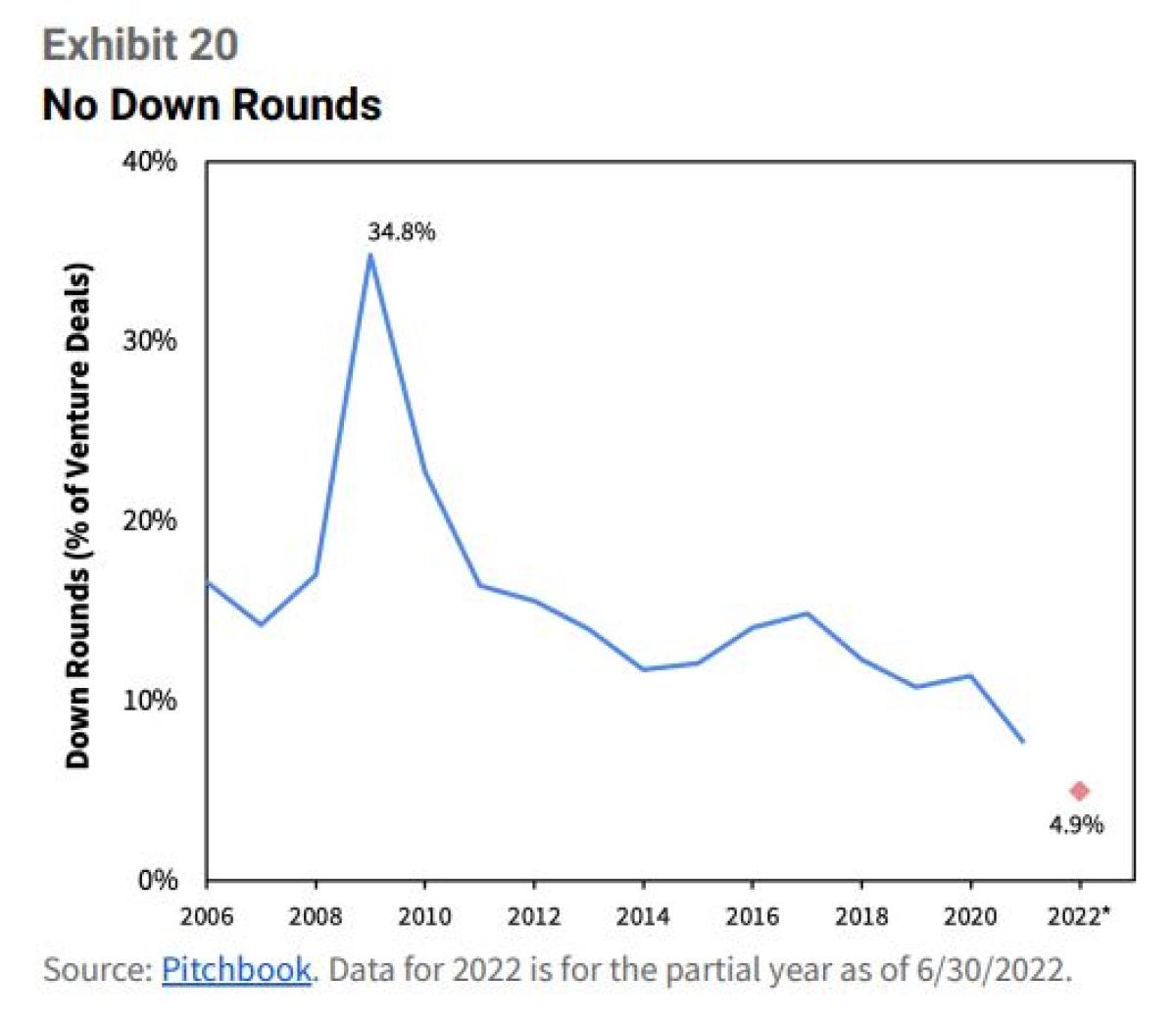

The total cumulative return and general contours of the replication closely match those of the venture index. The annual return correlation is a solid 72%. While the quarterly volatility of the replication is much higher, this is largely an artifact of the way private market performance is calculated (discussed in the next section). Venture Capital Risk Nowcasting Venture ⌚ The past year witnessed a sharp reversal of the 2020 stock market surge. Many once high-flying tech stocks, such as Affirm and Coinbase, are down 70 to 85% from last yearʼs highs. With all this carnage in the stock market, one would expect venture funds to be down similarly. However, venture funds are notoriously slow to mark down their holdings in market declines. Managers are incentivized to drag their feet in order to report smoother performance (and the illusion of lower risk). Startups are similarly loath to do “down rounds” (i.e., new financing at lower valuations). Of the 1,495 US venture deals in the first half of the year, only 4.9% have been down rounds – a historical low!

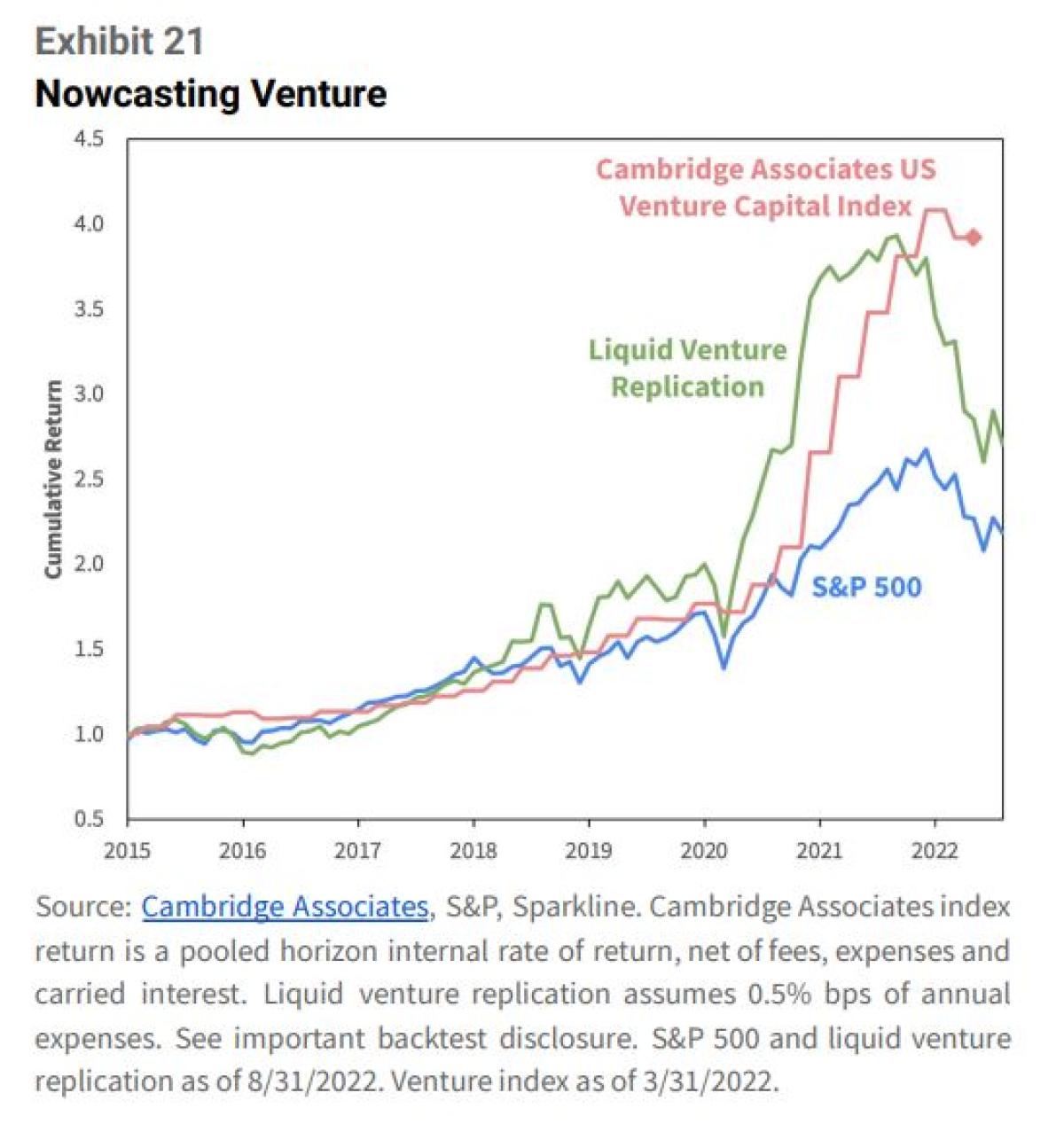

This inertia is problematic for allocators since it obscures the true valuation of their private investments. Fortunately, due to our replicationʼs tight correlation to the venture index, we can use it as a proxy for the true value of venture portfolios. The following exhibit plots the returns of the liquid venture replication, venture capital index, and S&P 500 on a monthly frequency. The venture index exhibits a “stair step” pattern as it only reports quarterly. It is also released with a few months lag, so the most recent datapoint is from 3/31/2022.

Even putting aside the reporting delay, the venture index lags the public markets. Venture funds were conservative marking up their books in the 2020 venture boom and are being similarly slow with write-downs in the bust.

Cambridge Associates recently published the (preliminary) Q1 2022 returns for its US Venture Capital Index. The index declined 3.98%. In contrast, our liquid replication fell 12% in Q1 2022 and tumbled 21% in Q2 2022. Even after rebounding the next two months, it is down 31% from its high.

From its peak, the venture index is down only 4% compared to 31% for the liquid replication. It is likely that the industry will continue to slowplay in the hopes the market turns and they never have to realize bad marks. But the longer public markets stay low, the less viable this approach will be.

Unpacking Venture

In Investing in Innovation (Apr 2022), we argued that investors in innovation funds, such as ARKK, are actually buying a bundle of factor exposures. This bundle includes not only innovation but also other unwanted factors such as “low profitability” and “high price-to-book.”

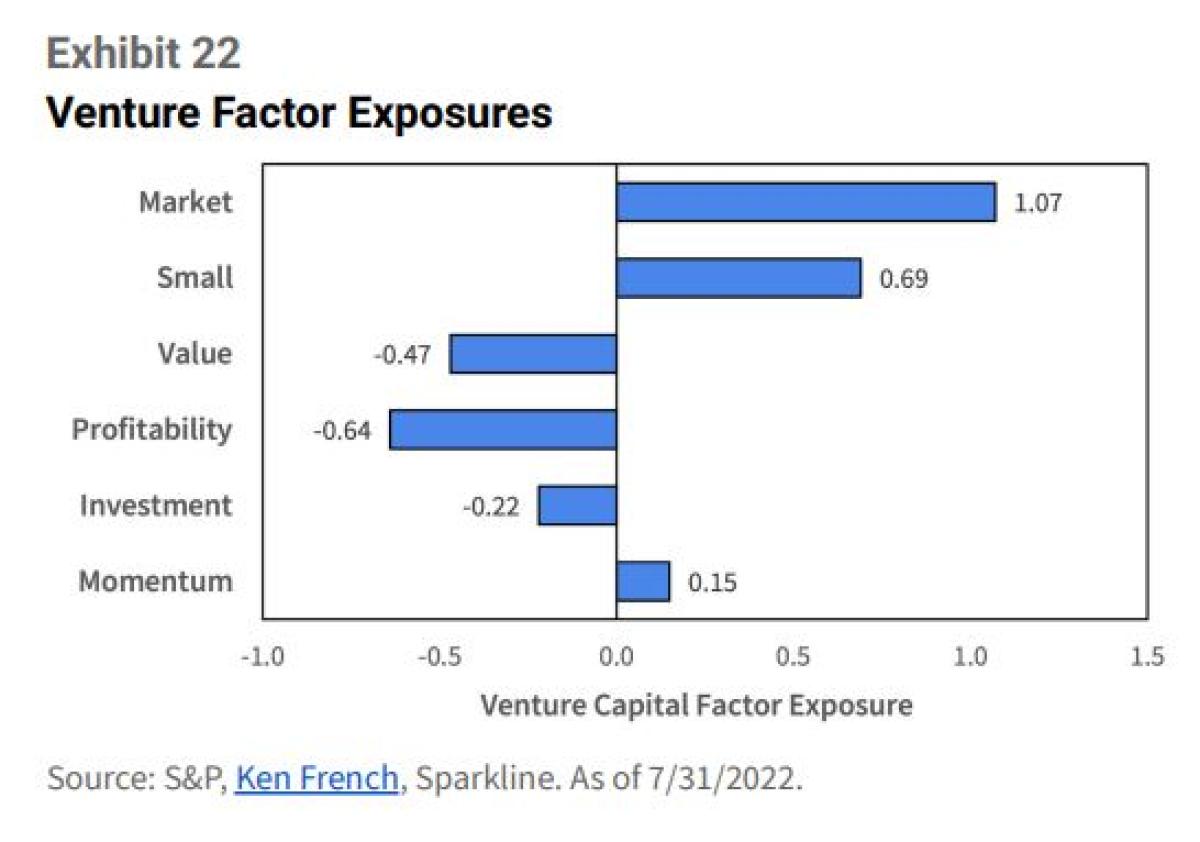

Now that we have created a liquid surrogate for venture capital, we can unbundle the sources of its returns using regression analysis. The next exhibit shows its exposure to the Fama-French factors widely used in the industry.

Venture capital is exposed to the overall stock market with a bias toward small, expensive, and unprofitable companies. Research shows that expensive and unprofitable stocks tend to underperform over the long run. Moreover, all six factors are commoditized “betas” that mainly contribute noise.

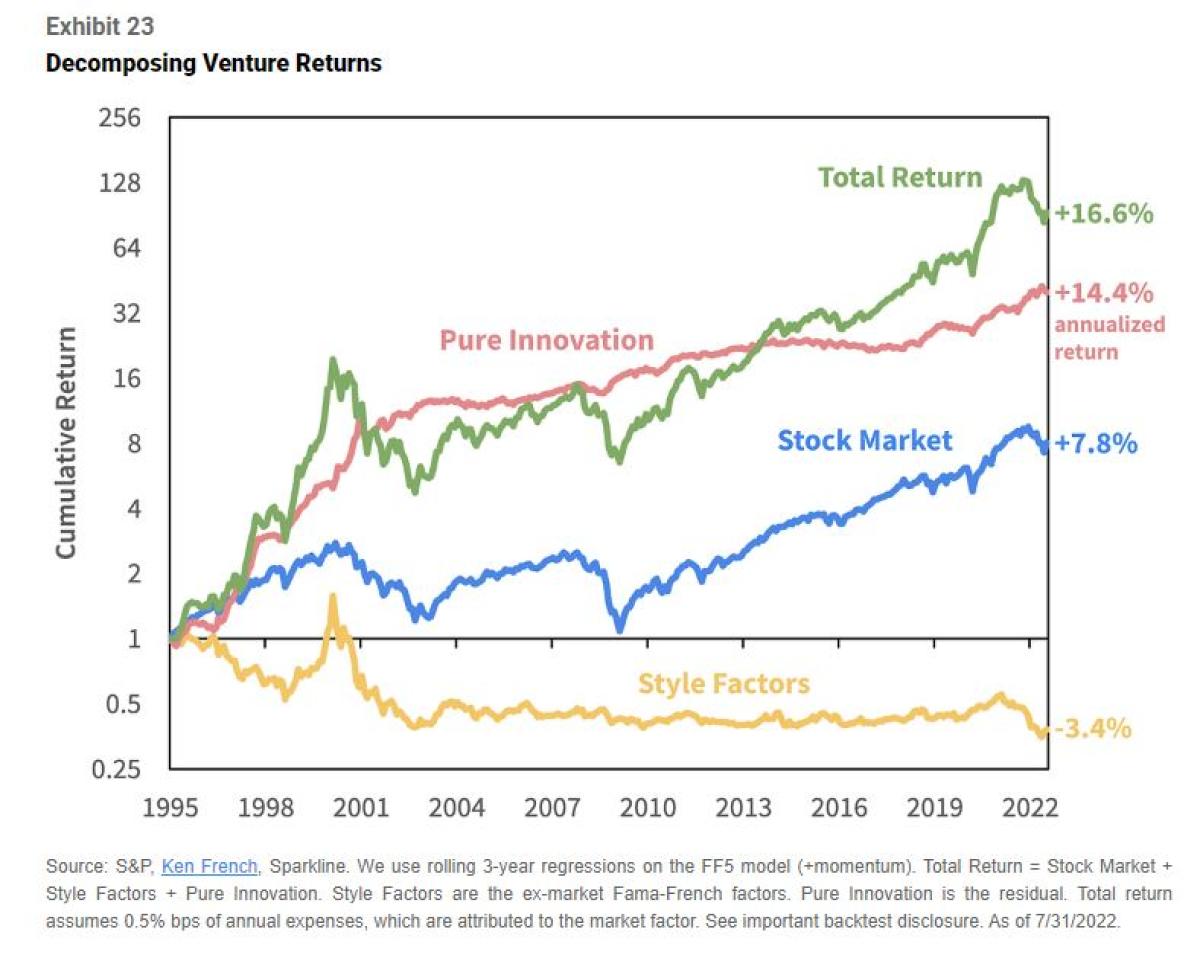

We can remove these unwanted factors to isolate the pure innovation driving venture returns. We decompose our liquid venture strategy’s returns into three categories. First, we carve out the market factor. Second, we combine the remaining five style factors into a single bucket. Finally, we consider the residual returns to be pure innovation.

Total Return = Market + Style Factors + Pure Innovation

The next exhibit decomposes the liquid venture strategy’s historical total return into the three components.

Pure innovation is the driving force behind the liquid venture strategy’s impressive historical returns. Not only is it remarkably consistent but it does not lose money in the major tech selloffs. On the other hand, style factors not only detract from the overall return, but explain the large relative losses of the strategy in the 2000 and 2021 tech busts.

Venture capital returns are indeed all about innovation. In fact, venture capital actually has adverse style exposures (i.e., unprofitable and expensive). Fortunately, the driving force of innovation has more than offset the headwinds from these unfavorable factor tilts.

Sleeping Giants 💤

“Large corporations welcome innovation … in the same way the dinosaurs welcomed large meteors.”

🦖Scott Adams

It is a popular myth that innovation only occurs at startups, as large firms are too bureaucratic and risk averse. However, this overlooks the innovative legacy of large industrial labs, universities, and government agencies. The information age owes much to researchers at large organizations, such as PARC, Bell Labs, IBM Research, ARPA and CERN.

Even today, many of the largest companies are carrying on this tradition. Big firms have virtually unlimited resources and the customers to predictably monetize breakthroughs. Last year, companies in the S&P 500 spent a combined $487 billion on R&D. Google and Facebook are at the forefront of artificial intelligence research, while Tesla is a trailblazer in electric vehicle and battery technology.

In order to assess the performance of innovation at large firms, we build a companion strategy to our liquid venture replication. However, this time we select stocks from the large-cap instead of small-cap universe (i.e., Russell 1000 v. Russell 2000). We also relax the age constraint.

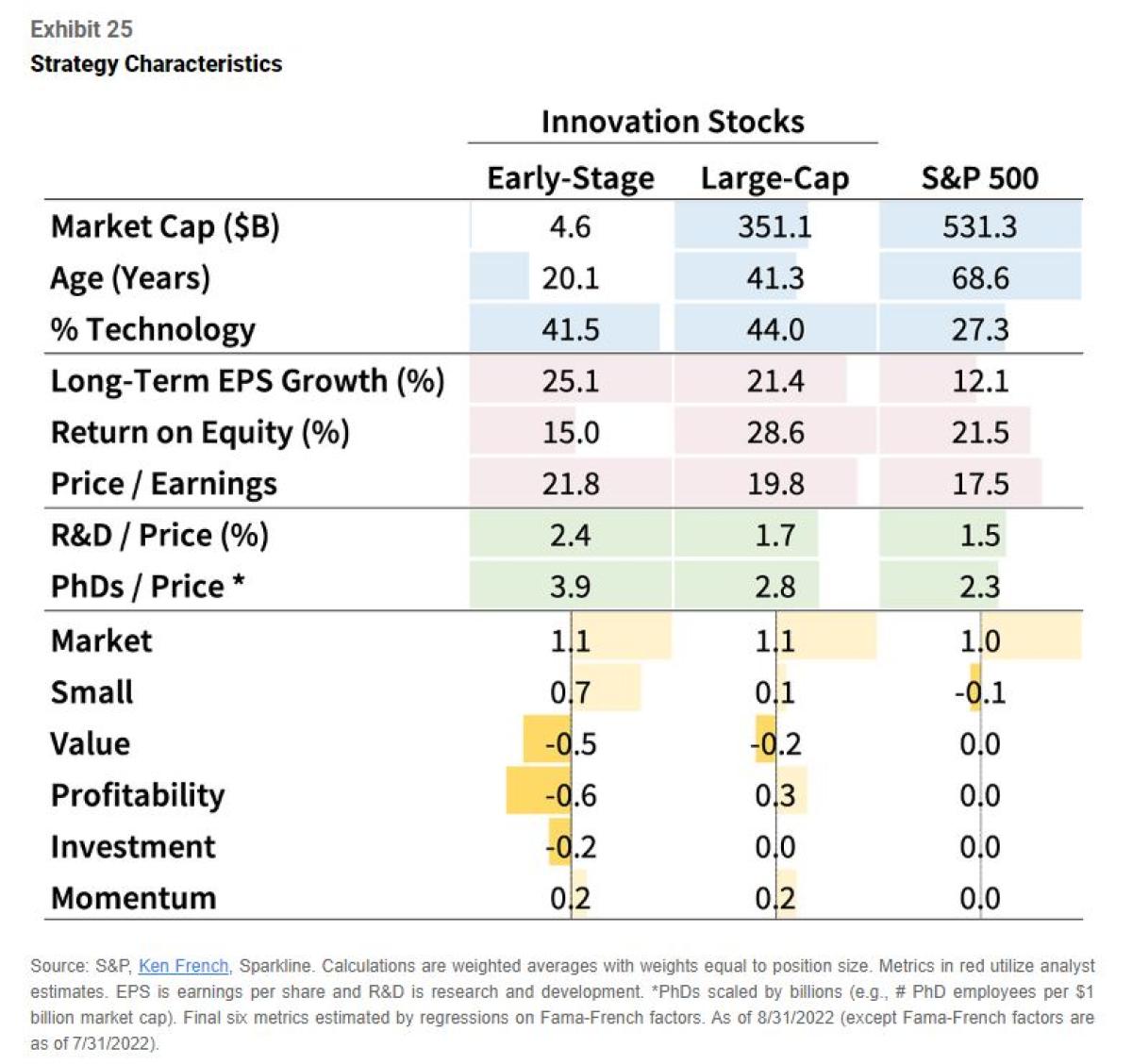

The next table compares the characteristics of large-cap and early-stage innovative stocks to those of the S&P 500. It shows both the headline portfolio characteristics from Exhibit 18 and Fama-French factor exposures from Exhibit 22 (the latter are in yellow).

Our large-cap innovators are much larger and older than our early-stage innovators. While they are a bit slower-growing and less intangible-intensive, they still enjoy a lead over the market. On the other hand, they are less expensive and significantly more profitable than their smaller brethren.

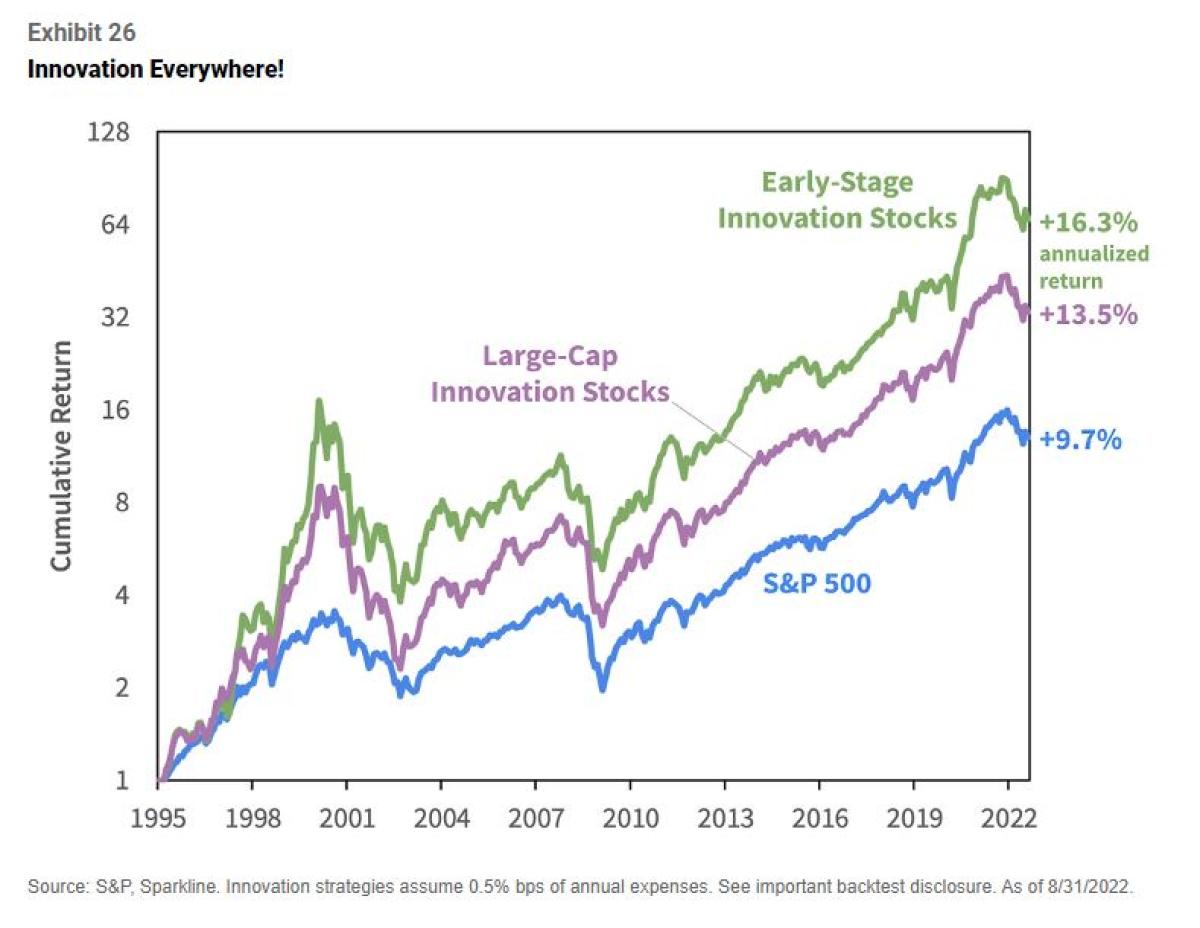

The next chart compares the performance of our large-cap and early-stage innovators to that of the S&P 500.

Large and small innovation stocks both beat the market. While early-stage innovators have higher returns, they also have higher risk (e.g., volatility and drawdown). Innovation at smaller firms is more “boom or bust.” Unlike larger firms, they cannot diversify their R&D across many projects.

Importantly, the returns of large and small innovators ebb and flow in tandem. The two strategies’ monthly returns are 93% correlated. Even the correlation of their returns relative to the market is a robust 85%.

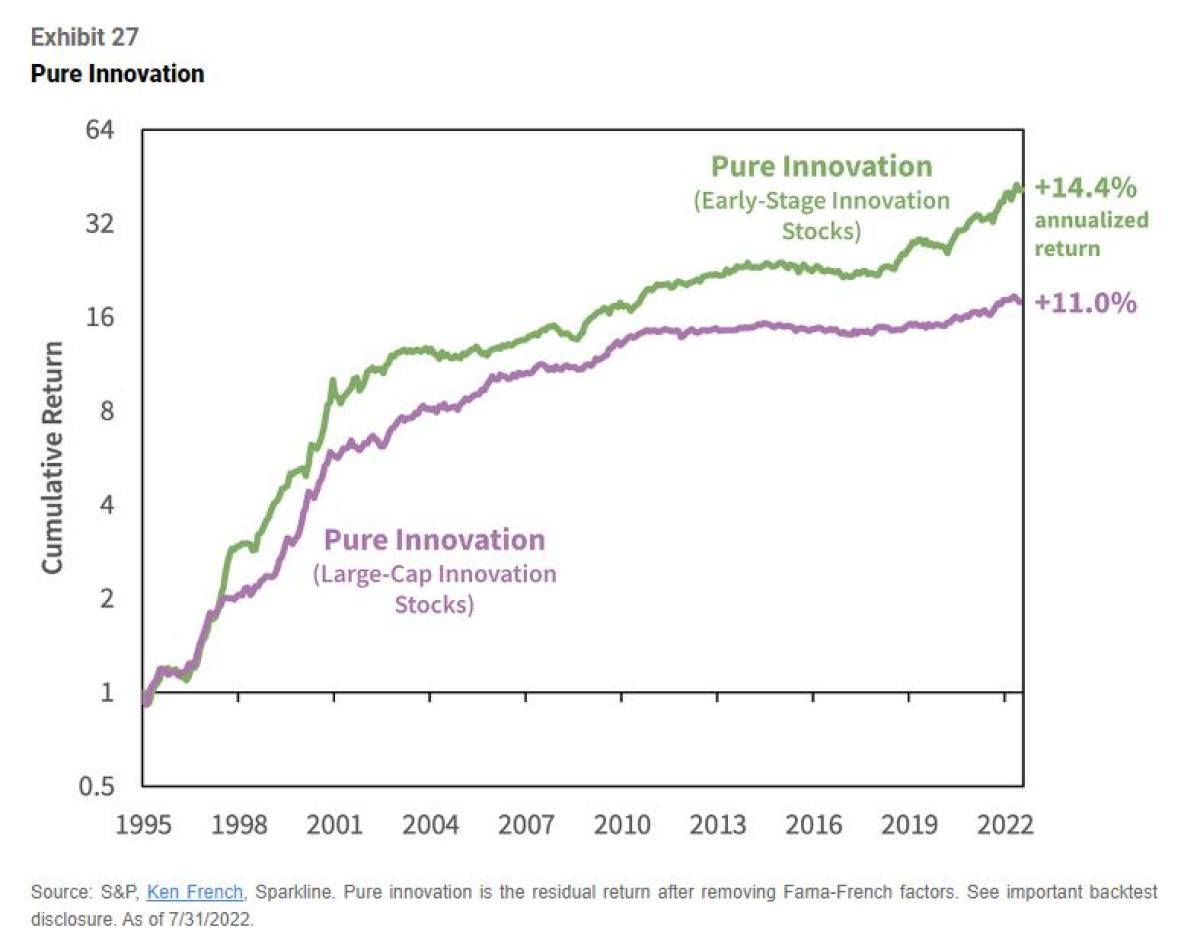

We next show the returns of “pure innovation” for both large and small innovators. As a reminder, pure innovation strips out the impact of the market and Fama-French style factors. The returns look very similar and have a 63% correlation.

Small innovation and large innovation are not two separate factors. Instead, there is a single universal innovation factor driving the returns of venture capital, early-stage innovation stocks, and large-cap innovation stocks. Innovation matters for all companies – private and public, small and large.

In summary, we were able to faithfully replicate the returns of the venture capital index using liquid public stocks. Next, we isolated the pure innovation factor driving the strategy’s returns. Finally, we found that this innovation premium exists not only in small but also large stocks.

Crypto Tokens/Crypto Venture Capital

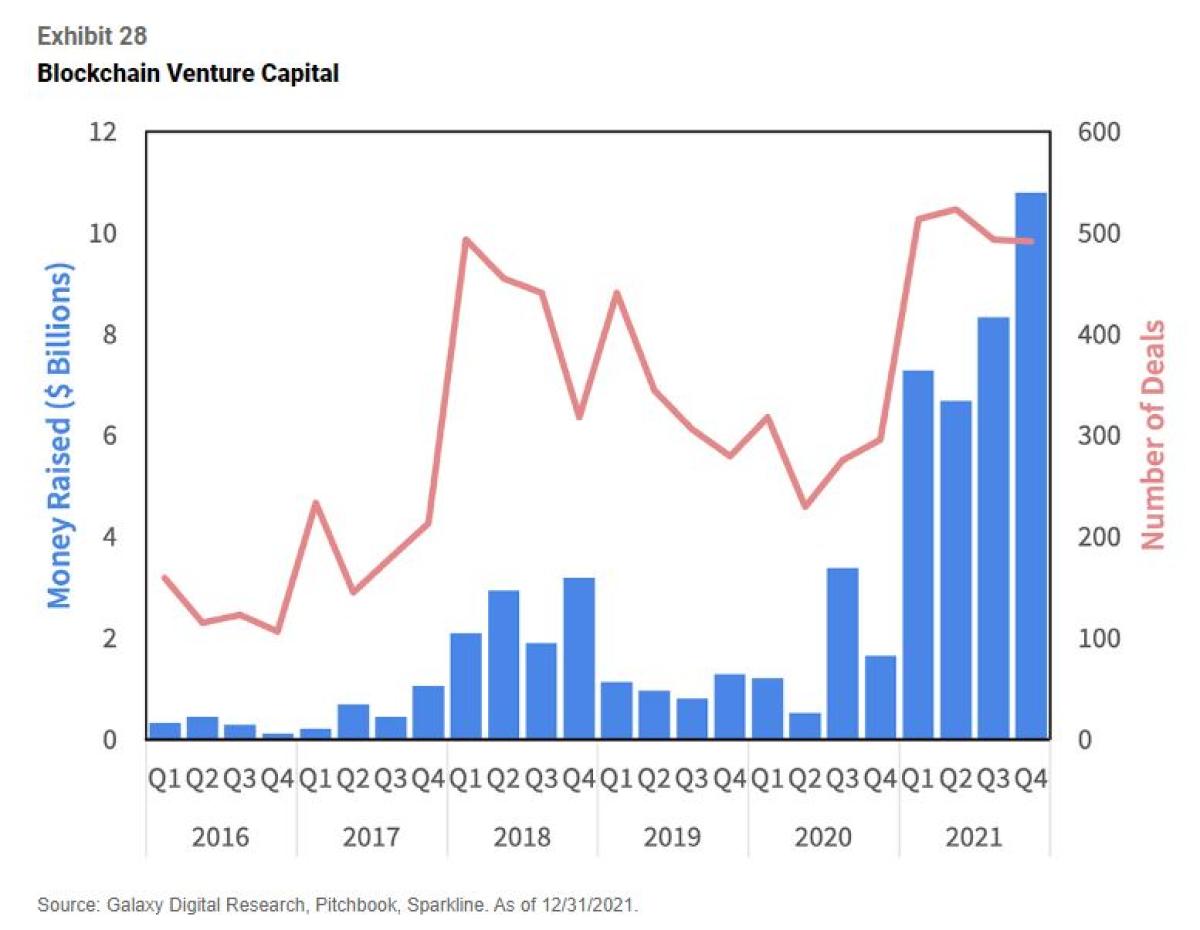

As we saw, crypto is the hottest theme in venture capital. Many venture investors view blockchains as a platform as transformative as the internet in the 1990s. In 2021, venture firms invested $33 billion in crypto companies, representing around 10% of total venture funding.

Venture capitalists have reaped extraordinary returns from their equity investments in crypto startups. Below is a list of top crypto unicorns. The valuations may be a bit generous inasmuch as they may not yet reflect write-downs from the recent crypto rout (i.e., only Coinbase is publicly traded).

Equities are not the only way venture funds get exposure to early-stage crypto projects. Venture firms can also invest in crypto tokens issued by these organizations. They may negotiate discounted allocations from protocol treasuries or simply buy on the open market. In other cases, they receive token distributions due to their equity stakes.

Crypto tokens can be even more lucrative than equities. For example, in July 2019, venture funds invested $20 million into Solana Labs but received SOL tokens rather than Solana Labs equity. Investors reaped an epic windfall when the SOL token subsequently surged over +20,000% to a peak market cap of $78 billion (although it has since fallen a lot).

Tokenomics 101 🍎

In order to understand why venture capitalists opted for SOL tokens instead of Solana Labs equity, we need to understand the economics of tokens. Perhaps the most intuitive way to explain “tokenomics” is by analogy to equities.

💰Dividends

Companies reward shareholders with dividends (paid in either cash or stock). Similarly, crypto projects may reward tokenholders with additional crypto. Such yields can be generated from a variety of underlying sources, such as exchange trading fees or staking rewards.

🔥Buybacks

Companies also reward shareholders with buybacks. By reducing share supply, buybacks increase the value of remaining shares. Crypto token burns remove coins from circulation to the same effect. In August 2021, Ethereum started burning a portion of tokens sent as transaction fees, deflating supply.

🖨️Issuance

Companies issue shares to raise capital and incentivize employees. There is no cap on equity issuance or total supply. In contrast, token issuance and supply are often capped. Bitcoin caps total supply at 21 million, while Ethereum caps annual issuance but not total supply.

🦺Vesting

Startup equity granted to venture capitalists and key employees often has a vesting period before it can be sold. Tokens have similar provisions. This is especially important as token liquidity generally occurs sooner.

🗳️Governance

Common shares carry voting rights on key matters of corporate policy, such as board composition and M&A. Governance tokens grant similar voting rights, such as over the use of the DAO treasury, tokenomics, and key technical proposals.

Of course, there are many ways that crypto and equities differ. Token rights are enforced by software code, whereas equity rights are enforced by the legal system. There are also regulatory differences (but we are not lawyers and don’t give legal advice). Most interestingly, smart contacts open up an exciting range of unique token features (e.g., airdrops, NFTs).

Crypto Opportunity Set 🌎

As mentioned in Value Investor’s Guide to Web3 (Jan 2022), there are four ways to get exposure to the crypto industry:

🐘 Mega-cap Crypto (BTC, ETH)

🪙 Small-cap Crypto

🏛️ Venture Equity

🏭 Public Equity

Crypto and equities provide access to distinct opportunity sets. For example, OpenSea, an NFT marketplace, is a private firm with no token. In contrast, its competitor LooksRare distributes 100% of its profits to its tokenholders. Investors can only own OpenSea via equity and LooksRare via token.

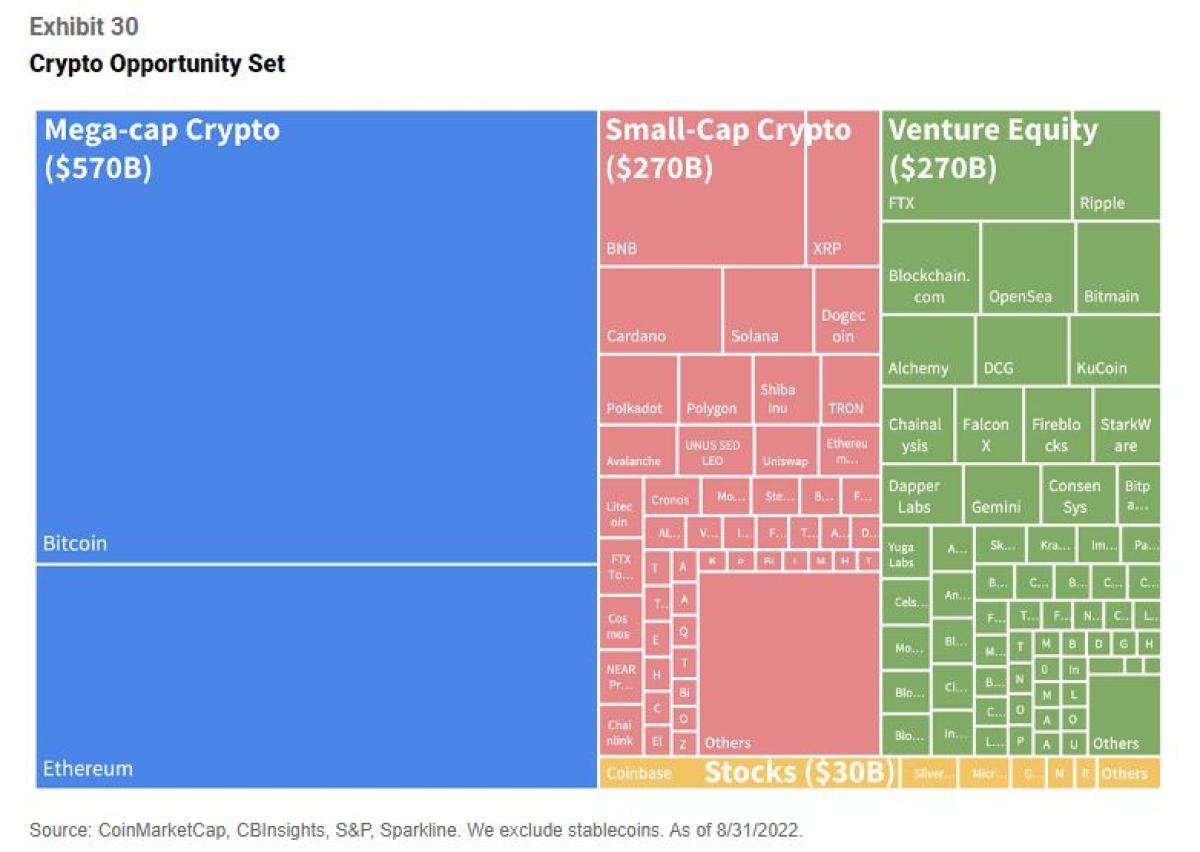

Cryptocurrencies are a large asset class. In total, crypto has roughly $1 trillion in market cap spread across 9,000+ assets. However, most of this value is in mega-cap crypto. Excluding Bitcoin ($380B), Ethereum ($190B), and stablecoins ($150B) leaves $270 billion in market value for small-cap crypto.

While private markets are opaque, we estimate another $270 billion in value is spread across several thousand private crypto startups. As mentioned, these most recent valuations may not reflect impending markdowns, so perhaps it would be fairer to haircut this estimate by 25 to 75%.

Finally, we counted only a couple dozen “pure play” crypto stocks. The total market cap of these stocks is a mere $30 billion, of which Coinbase alone is half (i.e., $15 billion). At least for now, the overwhelming majority of crypto firms are not listed on stock exchanges.

The next exhibit maps the full crypto opportunity set. While mega-cap crypto comprises half of the industry by market value, its two constituents offer very limited breadth. The other half is split evenly between small-cap crypto and venture equity. These groups offer a much broader and more diverse opportunity set with thousands of assets. Finally, public stocks are basically a rounding error.

Most institutional investors have used venture capital as their entry point into crypto. However, venture equities only cover around 25% of the opportunity set by market value and 50% by names. Investors seeking full coverage should also consider allocating to tokens.

Crypto Winter ☃️

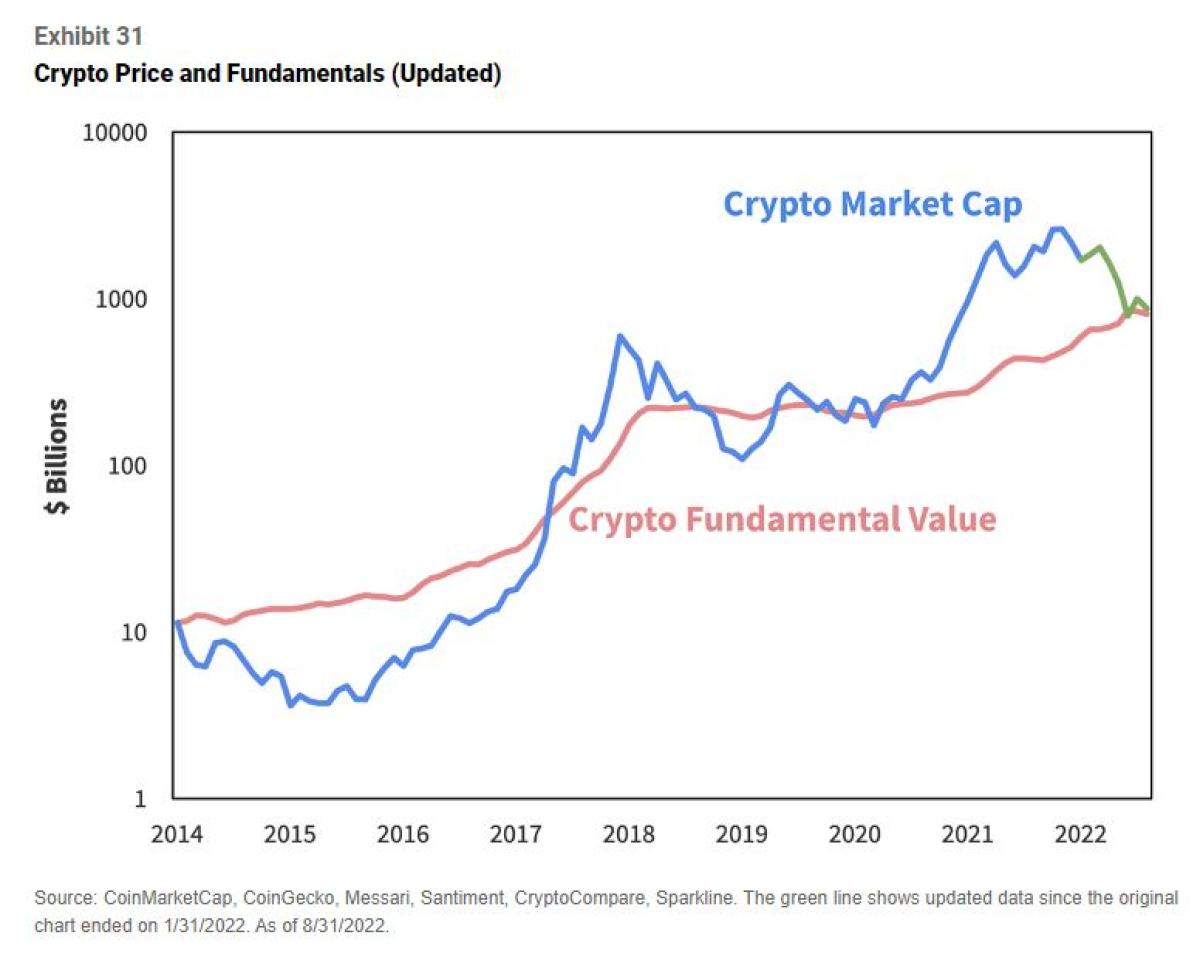

In Value Investor’s Guide to Web3 (Jan 2022), we introduced a framework for assessing the fundamental value of digital assets. Using data from GitHub, blockchains, and social media, we build metrics for crypto projects’ human capital, brand equity, intellectual property, and network effects.

Since 2014, the total fundamental value of the crypto asset class grew at a remarkable 50% compound annual rate. Our paper included a chart comparing total crypto market cap to fundamentals. The next exhibit updates this chart.

We originally showed this chart as of 1/31/2022 (blue line). We argued that despite strong fundamental growth, prices had overshot to the upside. Several months later, with prices down 67% from their peak, the market now appears more in line with fundamentals (green line).

Interestingly, total fundamental value has remained steady this year. While network activity has markedly slowed, this decline has been offset by stickiness in developer and social engagement. Despite the large outflow of speculators, the builders have mostly stayed. For what it’s worth, we saw this pattern in previous crypto winters as well.

As discussed, venture equities have yet to suffer many down rounds. The venture capital index is down only 3.98%. While the embattled BlockFi was forced to take a 90% hit, most crypto firms raised immense warchests in the boom and are unlikely to be in need of cash for a while.

In contrast, crypto tokens are liquid, and price discovery has not been kind. Most small-cap tokens are trading 60 to 90% below last year’s highs. All else equal, we believe this presents a more interesting opportunity for value-oriented investors building long-term allocations to Web3.

Innovation Investing

Venture Alpha

“Emphasizing inefficiently priced asset classes with interesting active management opportunities increases the odds of investment success. Intelligent acceptance of illiquidity and a value orientation constitute a sensible, conservative approach to portfolio management.”

🎓David Swensen, former Yale Chief Investment Officer

David Swensen’s genius was realizing decades ago that the nascent venture industry was rife with inefficiencies. His pitch for venture was less about the beta of the asset class than his belief that skilled managers could find alpha.

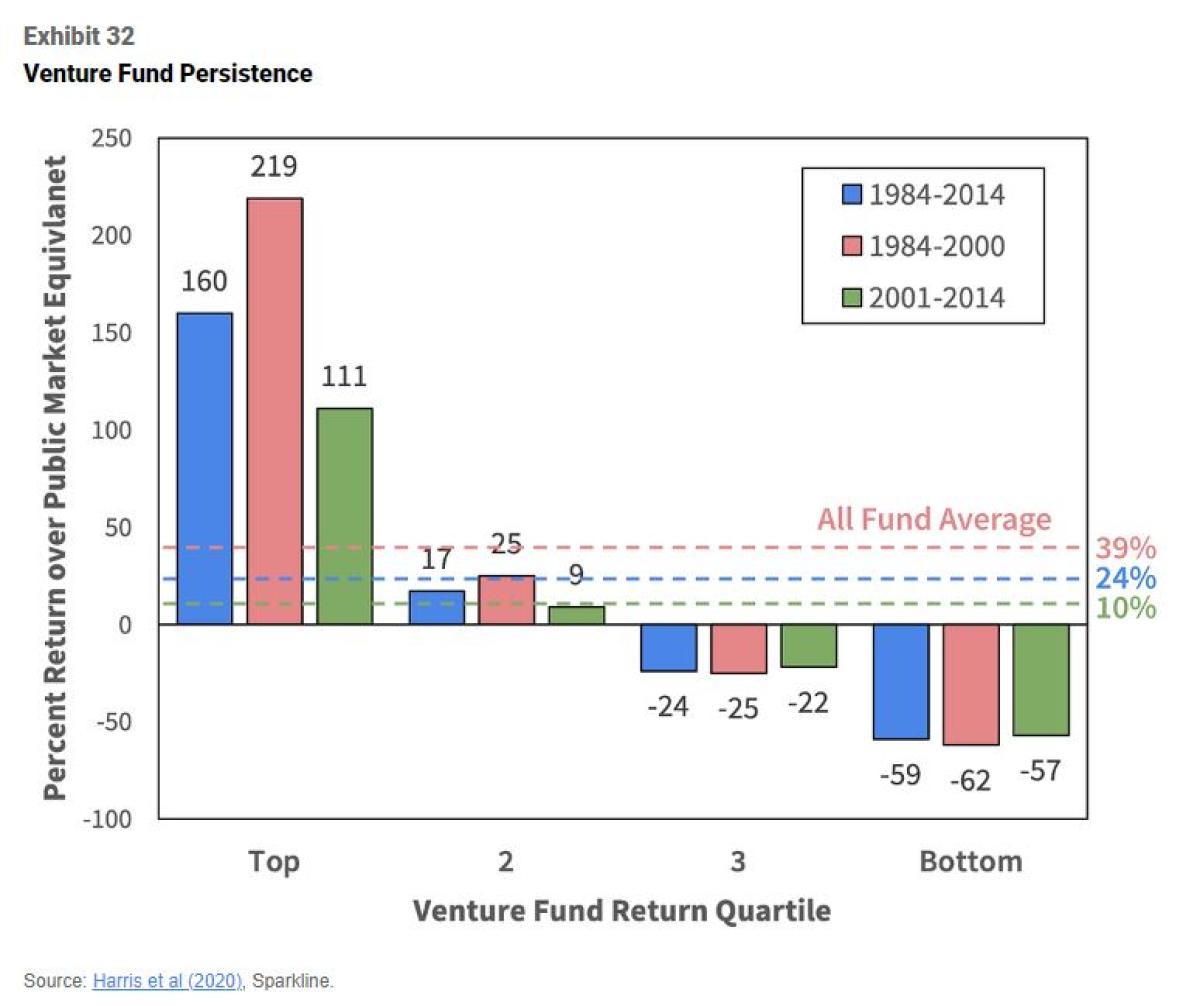

Swensen’s argument is reflected in the now conventional wisdom that venture index returns are driven by top funds. Harris et al (2020) found that venture capital funds outside of the top quartile either barely outperformed or greatly underperformed the stock market. Fortunately, the top quartile did so well that they more than made up for the other 75%, leading to a respectable average return.

Importantly, the researchers also found that venture fund returns have been highly persistent. Managers with top quartile funds are significantly more likely to have future funds in the top quartile. This persistence is likely due to the ability of top-tier venture firms to attract deal flow. As an allocator, if you are lucky enough to be in a top manager, sticking with them is generally a good idea.

The problem is that most of the best venture managers are at capacity and closed to new investors. And, as we just saw, the bottom 75% of funds are less than inspiring. Moreover, the authors found that the mean, dispersion and persistence of venture manager returns have all weakened since 2000.

This is the logical result of the institutionalization of private markets. Swensen was early in identifying the inefficiencies. However, venture capital has matured into a $2 trillion industry. This influx of capital has likely eroded much of the advantage Yale enjoyed as an early mover in the late 1980s.

Option Value of Liquidity

One big unlock for Swensen was his belief that Yale could withstand a considerable allocation to illiquid assets. Yale’s multi-decade investment horizon and wealthy alumni donor base made it particularly well suited to commit heavily to illiquid funds with decade-long lockups.

One common justification for allocating to illiquid assets is the so-called “illiquidity risk premium.” This is the excess return investors should expect (in theory) to earn for bearing illiquidity. Yale was early to embrace private equities when the illiquidity risk premium was very large. However, a lot of capital has flooded the private markets since then.

Some believe that the pendulum has swung too far. AQR has argued that allocators now view illiquidity as a “feature not a bug.” As we saw, venture returns are highly smoothed. AQR posits that investors may even be willing to accept a lower return for the ability to bury mark-to-market volatility. AQR’s Cliff Asness has cleverly called this “volatility laundering.”

Investors should remember why liquidity is valuable in the first place. Liquidity is effectively an “option” that grants investors the ability to change their mind or respond to new investment opportunities. Conversely, investors who lock themselves into the current opportunity set forgo the ability to take advantage of future opportunities.

We can model the option value of liquidity as a function of the implied volatility of the future opportunity set. If we don’t expect any interesting opportunities to crop up, there is little cost to forgoing liquidity. Conversely, if we expect the future to be very exciting, illiquidity has a high cost.

Investments in early-stage innovation have very high implied volatilities. The range of startup outcomes is extremely wide due to the power law. Crypto tokens allow us to directly observe this volatility, which often runs at 100% annualized.

Therefore, investors in innovation should place an especially high premium on liquidity. Technological trends can shift abruptly, and the best startups today may not be the best tomorrow. Liquidity allows investors to course correct in the face of a rapidly evolving landscape.

Lifecycle of Innovation 👶👦👨👴

“We think the VC model is outdated. It creates an odd dynamic between us and founders, where on the eve of an IPO they're asking if we're going to have to get off their boards and quickly distribute the stock. Why should that be the default, particularly when so much value creation happens later?”

🌲Roelof Botha, Sequoia Capital

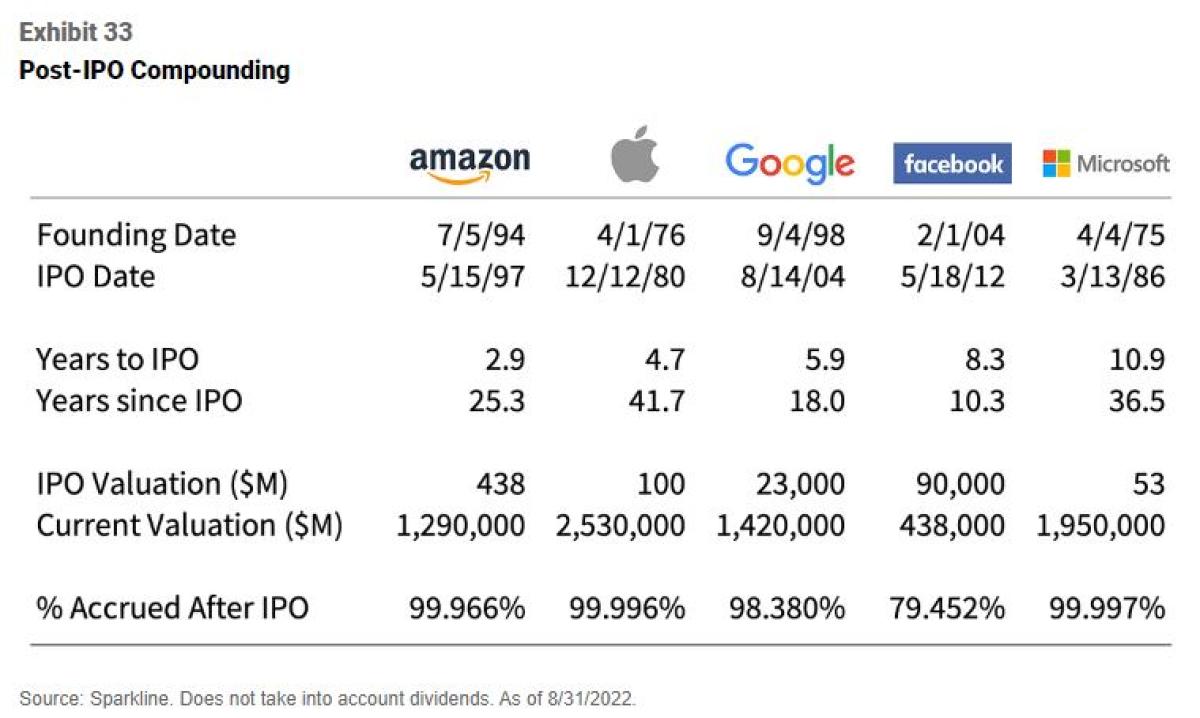

Sequoia Capital, arguably the most well-respected venture capital firm, recently restructured around an evergreen fund and registered as an SEC advisor. This allows them to hold onto the public shares of their winners long after the IPO. As of Oct 2021, Sequoia already held $45 billion in the public shares of firms such as Unity and DoorDash.

Sequoia’s argument that most value creation happens after the IPO is patently true. Sequoia uses Square as an example. They helped Square build to a successful $2.9 billion IPO but missed out on most of the post-IPO gains on its way to a $117 billion valuation. This has been the case for most iconic companies. As the next exhibit shows, 99.966% of Amazon’s value came after its 1997 IPO.

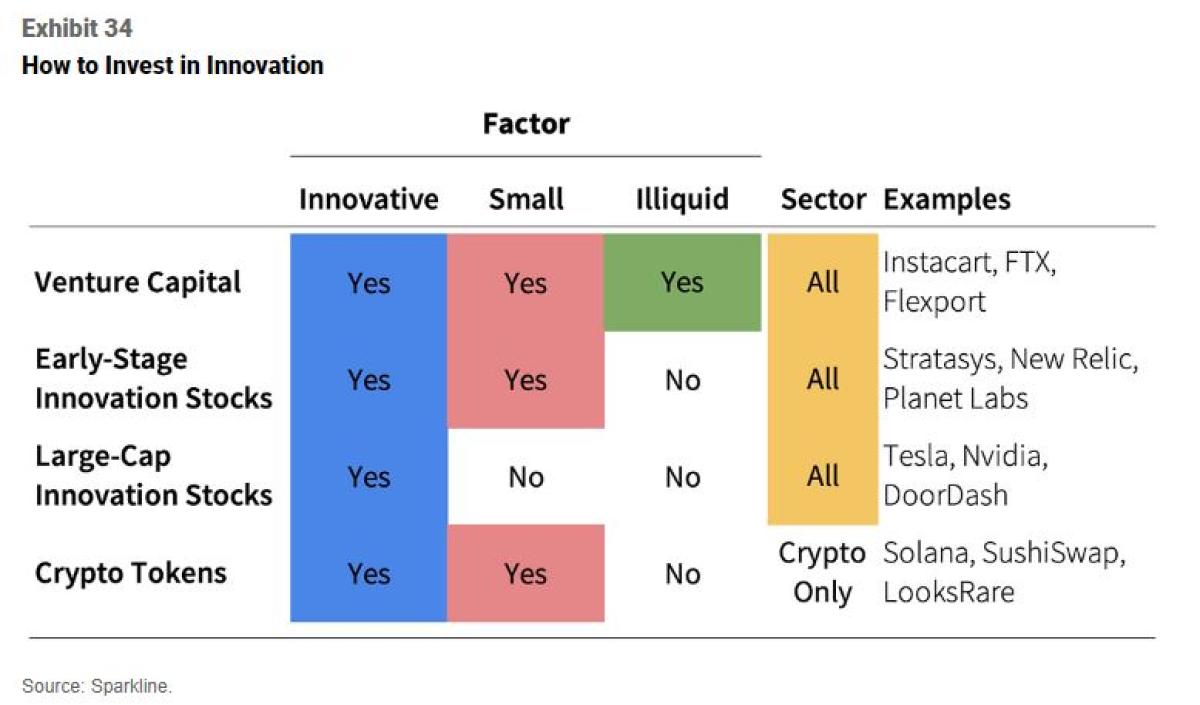

Investors should consider following Sequoia’s lead. The full lifecycle of innovation extends far beyond the IPO. Investing in innovation means owning more than just private startups. Innovation is not only the driver of venture capital returns but has also delivered excess returns in small-cap stocks, large-cap stocks, and crypto tokens.

Innovation investors should consider a portfolio of all four pieces, balanced to obtain the desired blend of size, liquidity and sector exposure. Very large allocators could consider cap-weighting for capacity reasons. Meanwhile, those with alpha views could allocate more to certain categories (e.g., crypto tokens, an inefficient “frontier market”).

Value Investing

“All markets have boom and bust cycles, and I think the venture capital market has even more exaggerated boom and bust cycles.”

🗽Fred Wilson, Union Square Ventures

In his quote from earlier, Swensen argued that investors should employ a value orientation. We believe this is especially true in the innovation sector. In Investing in Innovation (Apr 2022), we showed that technological revolutions are especially prone to hype and speculative bubbles (e.g., canal mania, railroad mania).

Our mission is to bring the time-tested principles of value investing into new frontiers. While we are excited to apply innovation investing into liquid venture capital and crypto tokens, we believe investors must first arm themselves with the tools of value.

We have published several papers on “intangible value.” This idea extends traditional book value to encompass intangible assets, such as innovation, brand equity, human capital and network effects. We believe this framework enables us to apply value principles to new frontiers.

If you’re interested in learning more, we would recommend the following papers:

🏛️ Intangible Value: Stocks

🪙 Value Investor’s Guide to Web3: Crypto tokens

🧬 Investing in Innovation: Innovation stocks

Conclusion

Venture capital has been the killer app for elite institutional investors. However, as capital has flooded the asset class, investors are looking for other ways to harness its returns without the illiquidity and adverse selection.

The true source of venture returns is innovation, which also occurs at public companies, both large and small. We believe that investors should extend their “innovation allocation” from venture capital into public equities. This should help investors capture the full innovation lifecycle while enjoying greater liquidity.

In addition, while many investors have used venture capital as their beachhead into crypto, liquid tokens offer at least as interesting an opportunity set. In line with Swensen’s original thesis, we believe that tokens provide exposure to blockchain innovation in an inefficient frontier asset class.

About the Author:

Kai Wu is the founder and Chief Investment Officer of Sparkline Capital, an investment management firm applying state-of-the-art machine learning and computing to uncover alpha in large, unstructured data sets.

Prior to Sparkline, Kai co-founded and co-managed Kaleidoscope Capital, a quantitative hedge fund in Boston. With one other partner, he grew Kaleidoscope to $350 million in assets from institutional investors. Kai jointly managed all aspects of the company, including technology, investments, operations, trading, investor relations, and recruiting.

Previously, Kai worked at GMO, where he was a member of Jeremy Grantham’s $40 billion asset allocation team. He also worked closely with the firm's equity and macro investment teams in Boston, San Francisco, London, and Sydney.

Kai graduated from Harvard College Magna Cum Laude and Phi Beta Kappa.