By David Stevenson, a London-based financial writer for PitchBook News, covering private equity.

Investors in private equity have been gravitating towards large established firms in a tough fundraising environment although one sector has emerged that may well offer a glimmer of hope to even first-time managers, impact investing.

PE’s traditional institutional investor base’s capacity to allocate to the asset class has been diminished by the denominator effect. This is where public markets, both stocks and bonds, have fallen in valuation making the investors’ allocation to PE oversized for their respective investment mandates.

One of the results of this tightening fundraising environment is - as Paula Langton, co-head of fund placement at Campbell Lutyens says - a bifurcation of the market.

In our Q2 European Private Equity Breakdown, analysts noted that larger funds, which are often run by those with better-known track records, are able to secure capital more easily than smaller vehicles, run by emerging managers.

However, LPs may apply investment criteria other than return and risk, such as ESG, and impact on their GP selection process, potentially widening the pool beyond the large players.

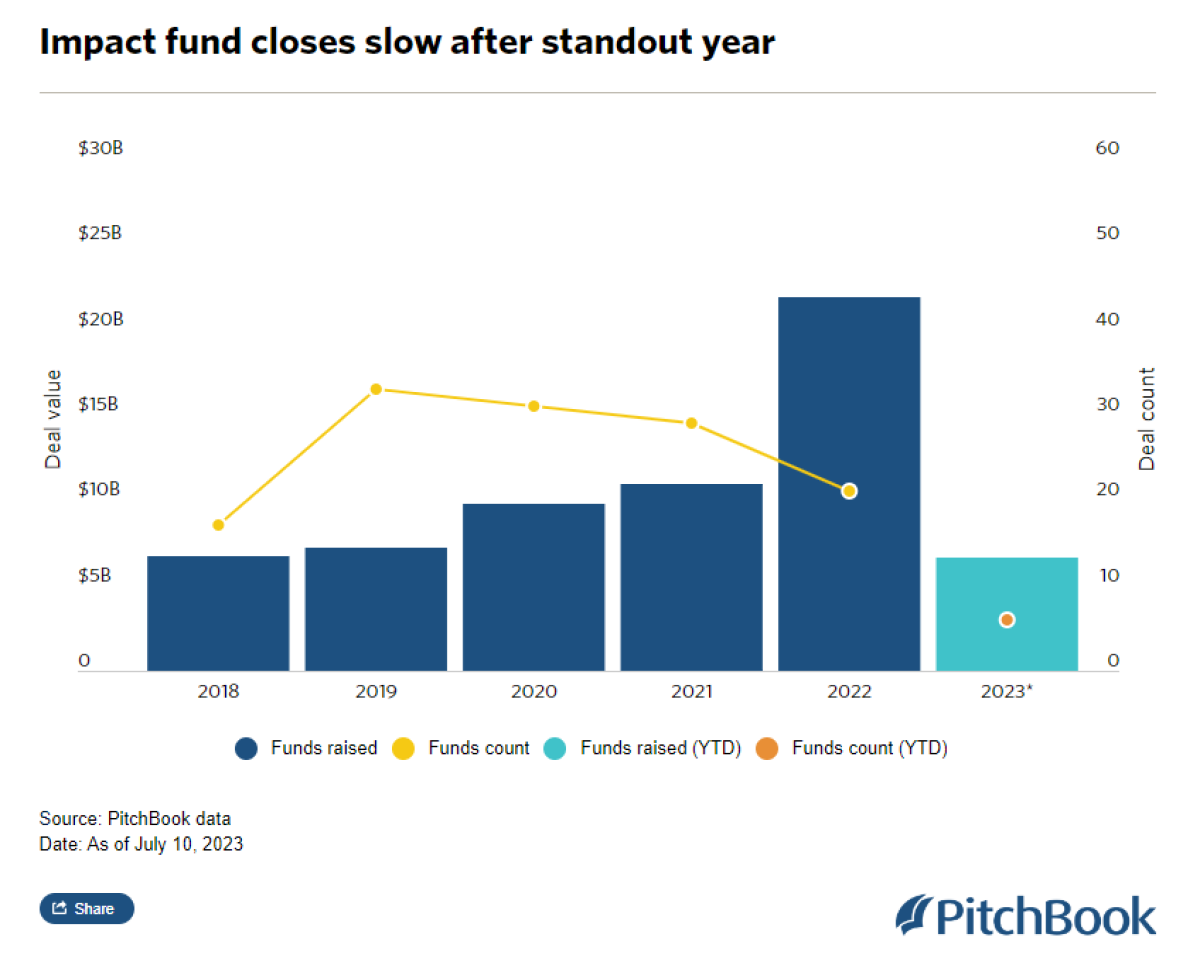

There has been a spike in impact fundraising, with last year seeing almost $22 billion raised globally in the space according to PitchBook data.

“We're seeing a lot more activity in sustainability. More new commitments going into sustainability, particularly climate. And LPs are a little bit more open to committing to people that they've never even heard of maybe six months before,” said Langton.

When it comes to the terms LPs are willing to accept in this area, it appears that they are more accommodating compared to plain vanilla buyout funds.

Langton said a few investors in the market have started to ask for impact-linked carry. This is where a proportion of the GP’s carried interest is reliant on the fund achieving certain impact goals. These could include reducing carbon emissions or improving gender or racial equality on the boards of the fund’s portfolio companies for instance.

Measuring the impact of portfolio companies may be easier said than done and could have adverse outcomes however. Luke Dixon, managing director of private markets investment platform Dot Investing said: “LPs need to be mindful that to get the necessary cooperation from portfolio company management over the data collection from their preferred investments, GPs may instead invest in companies where they may hold less investment conviction but where they can collect the necessary impact data.”

It’s not just GPs that are concentrating on collecting the relevant evidence to show an impact has been made through investment. Scott Church, co-founder of placement agent Rede Partners, said LPs and their consultants are pouring resources into what Church dubs “authenticity”. This is making sure a GP’s impact fund is doing what it says on the tin and not simply greenwashing, making claims with no substance.

“It's a whole specialism, this area of proving something’s authentically impactful. On the reporting side and what investors demand to see in terms of evidence that they're delivering the impact they're claiming, it’s huge,” Church enthused.

GPs are keen to show that impact investing is not just an “AUM grab”, according to Langton. She added that while there were maybe less than 10 GPs doing this just four years ago, this number is more like 50 to 60 today.

The roots of LPs seeking out impact investments and making sure they were done properly were in Europe, with the European Investment Fund being among the first movers in the space in 2008.

William Barrett, co-founder of Paris-based placement agent Reach Capital, said that one outcome of the reduced volume in fundraising is that it will have a medium-term impact on hiring and team development. “We have heard of several large PE firms on hiring freezes,” he said, in relation to the asset class as a whole.

Conversely, Rede Partners Church said he’s seeing institutional growth in the impact space including more people, teams and heads of the sector. Presumably, this growth from LPs is being reflected on the sponsor side, so while there may be issues for even large PE firms due to reduced fundraising, emerging impact managers may still be attracting commitments. And if the funds launched prove to be authentic, managers may not have to give too much away to LPs keen to show their green credentials.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

David Stevenson started his journalism career at Euromoney, covering the tax aspects of major corporate M&A deals including private equity in 2008. He has written for institutional investor-focused Funds Europe, wealth management and private bank-aimed PAM Insight as well as private markets data provider PitchBook among many others.