By Vincent Weber, CEO and Head of Research at Resonanz Capital, an investment advisory firm specializing in absolute return strategies.

Examining the rise of Payment-In-Kind (PIK) debt in private credit markets and its implications for investors and lenders.

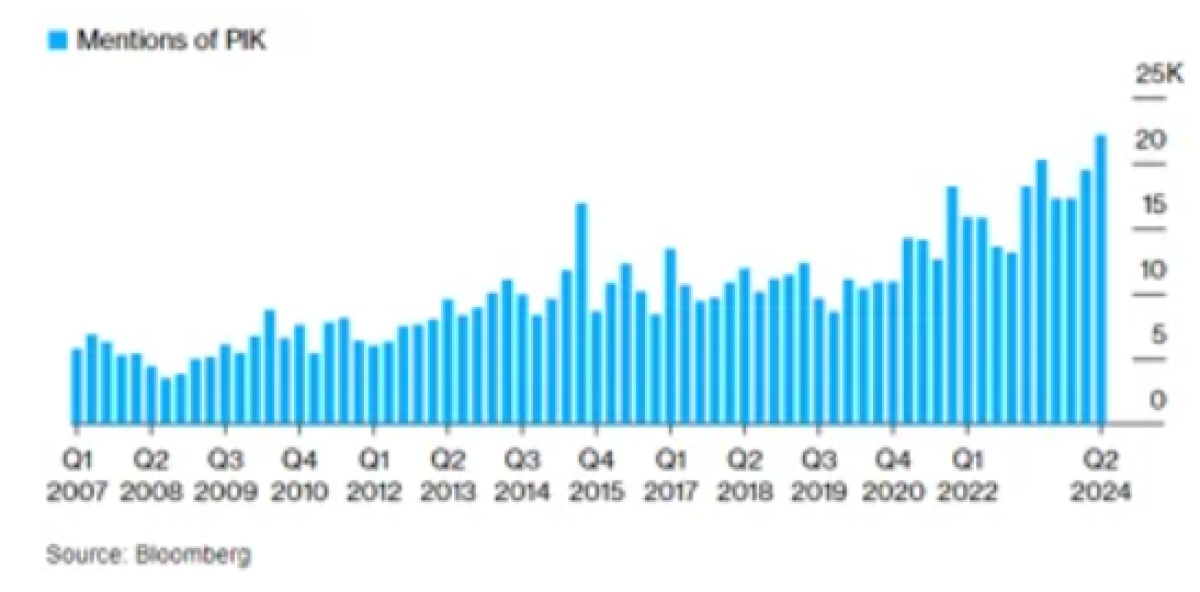

In recent years, a significant shift in the private credit landscape has emerged with the increasing use of Payment-in-Kind (PIK) financing. PIK, which allows borrowers to defer interest payments and instead add them to the loan principal, has garnered heightened attention from both investors and regulators. Traditionally viewed as a mechanism for distressed companies or junior debt, PIK is now creeping into the mainstream of the credit markets. The trend is raising concerns about the underlying health of companies, liquidity pressures, and the resilience of private credit funds. As private equity firms and business development companies (BDCs) increasingly turn to PIK to manage liquidity and navigate rising interest rates, the broader ramifications of this trend merit careful scrutiny.

What Is PIK and Why Is It Rising?

PIK debt allows companies to defer interest payments by adding the interest to the loan principal, effectively capitalizing the interest owed. This mechanism can provide immediate relief to companies facing cash flow pressures, especially in an environment of higher interest rates. However, the growing prevalence of PIK in the private credit market is more than a simple liquidity management tool; it reflects deeper issues within the financial ecosystem.

One of the key drivers behind the rise in PIK usage is the increased cost of borrowing. As interest rates remain elevated, companies that previously borrowed at low rates now face the challenge of refinancing at much higher rates. This pressure has led many to seek alternatives to traditional cash interest payments, with PIK emerging as a solution. The appeal of PIK lies in its ability to provide companies with breathing room, allowing them to avoid immediate cash outflows that would strain their liquidity.

However, the widespread adoption of PIK is not without its risks. The deferral of interest payments increases the overall debt burden on companies, making it more challenging to service debt in the long term. Moreover, the fact that PIK is no longer confined to junior debt but is increasingly seen in senior loans suggests that the companies utilizing it may be facing significant financial difficulties. This shift signals a growing reliance on creative financing solutions to maintain solvency, which could have far-reaching consequences.

What Does the Surge in PIK Mean for Private Credit?

The rise in PIK debt is raising concerns among investors and regulators alike. On the surface, PIK can appear to mask the underlying financial health of borrowers. By deferring interest payments, companies may be able to avoid default in the short term, but they are effectively kicking the can down the road. This approach can lead to a buildup of hidden leverage within the system, which could pose systemic risks if not carefully managed.

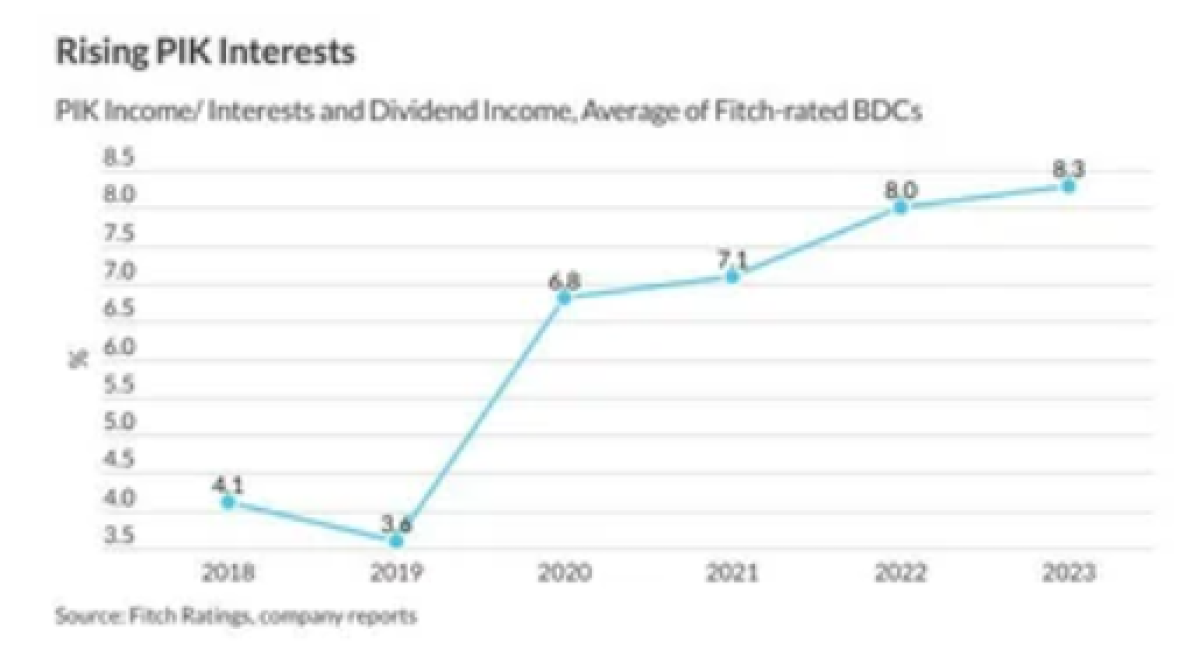

Private credit funds, which have become major providers of PIK debt, are particularly exposed to these risks. According to recent reports, PIK now accounts for a significant portion of income for many private credit funds, with some funds seeing PIK make up as much as 12% of their interest income. This trend is concerning because it suggests that these funds are increasingly relying on income that is not being paid in cash, but rather being capitalized and added to the debt principal. If the companies taking on PIK debt are unable to repay their obligations when due, the funds that provided this credit could face substantial losses.

Moreover, the increasing use of PIK is contributing to a more complex and opaque financial environment. Since PIK debt often results in higher leverage ratios that are not immediately apparent, it becomes more difficult for investors and regulators to accurately assess the risk profiles of these companies and the funds that lend to them. This lack of transparency could lead to mispricing of risk and potential market disruptions if defaults begin to rise.

Are We Heading Towards a PIK-Driven Crisis?

Despite the risks, PIK is not inherently negative. In fact, in certain situations, PIK can be an effective tool for companies looking to reinvest cash flows into growth opportunities rather than servicing debt. For example, high-growth companies with solid long-term prospects may prefer to use PIK to free up cash for investment, believing that future returns will outstrip the additional debt burden. For private credit funds, such situations can offer higher returns, as PIK loans typically come with higher interest rates to compensate for the additional risk.

Moreover, PIK can be a useful mechanism for lenders and borrowers to negotiate terms during periods of financial stress. In some cases, it may be preferable for a lender to allow a borrower to use PIK rather than force a default. This flexibility can enable companies to navigate temporary cash flow issues while protecting the lender’s investment.

Nonetheless, the potential for a PIK-driven crisis in the private credit market cannot be ignored. As PIK becomes more prevalent, the likelihood of widespread defaults increases, especially if economic conditions deteriorate. Companies that have deferred significant amounts of interest through PIK will eventually face a reckoning when their debts come due. If these companies are unable to generate sufficient cash flow to cover their obligations, they may default, leading to losses for lenders and potentially triggering a broader credit crunch.

Regulators are increasingly concerned about the systemic risks posed by the rise in PIK debt. The deferred interest payments inherent in PIK structures mean that companies are effectively taking on more debt than is immediately visible, which could lead to a wave of defaults if economic conditions worsen. This concern is particularly acute in the private credit market, where the lack of transparency and the complexity of financial structures can obscure the true level of risk.

Conclusion

The rise of PIK in the private credit market is a double-edged sword. While it offers short-term relief for companies facing liquidity challenges, it also introduces significant long-term risks. The deferral of interest payments increases leverage, creates hidden risks, and could lead to a wave of defaults if companies are unable to meet their obligations.

For investors and fund managers, navigating the PIK landscape requires a cautious and informed approach. It is crucial to differentiate between companies that use PIK as a strategic tool for growth and those that rely on it out of necessity due to financial distress. As the private credit market continues to evolve, the rise of PIK serves as a reminder of the importance of diligence, transparency, and risk management in an increasingly complex financial environment.

All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer.

About the Author:

Vincent Weber is the CEO and Head of Research at Resonanz Capital, an investment advisory firm specializing in absolute return strategies. Prior to founding Resonanz Capital in 2019, Vincent led the Absolute Return team at Prime Capital AG. He holds degrees from Imperial College London, Goethe University Frankfurt, and Dauphine University Paris.