By Ken Miller, CFA, Portfolio Manager, and Michael Green, CFA, Portfolio Manager, Chief Strategist at Simplify ETFs.

Introduction

Asset allocation requires a balance between offense and defense. When traditional diversifiers like bonds fail to deliver in an equity market selloff, investors begin to look for alternatives that mitigate drawdown risk without burning capital through purchases of insurance. One such potential solution is managed futures.

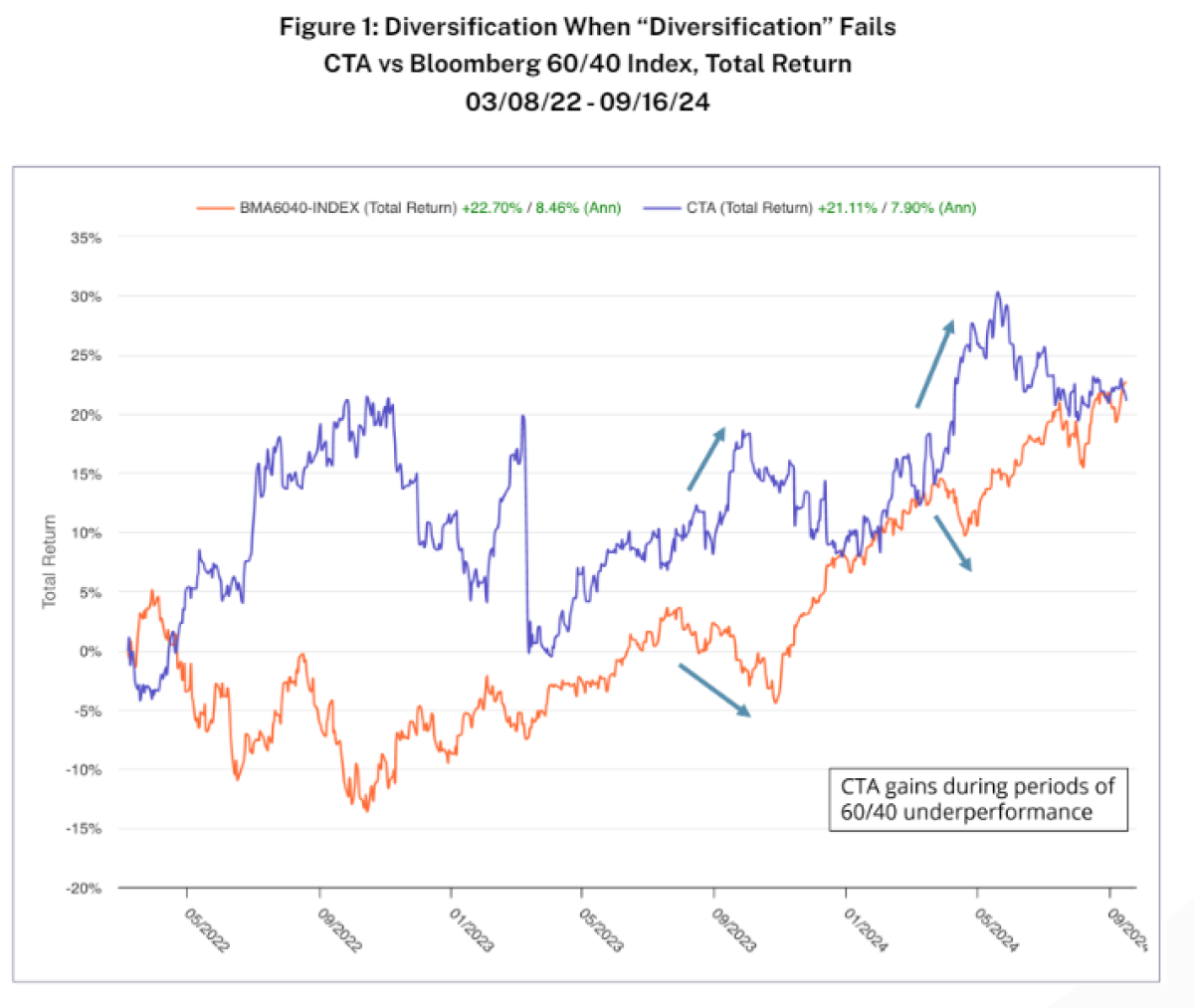

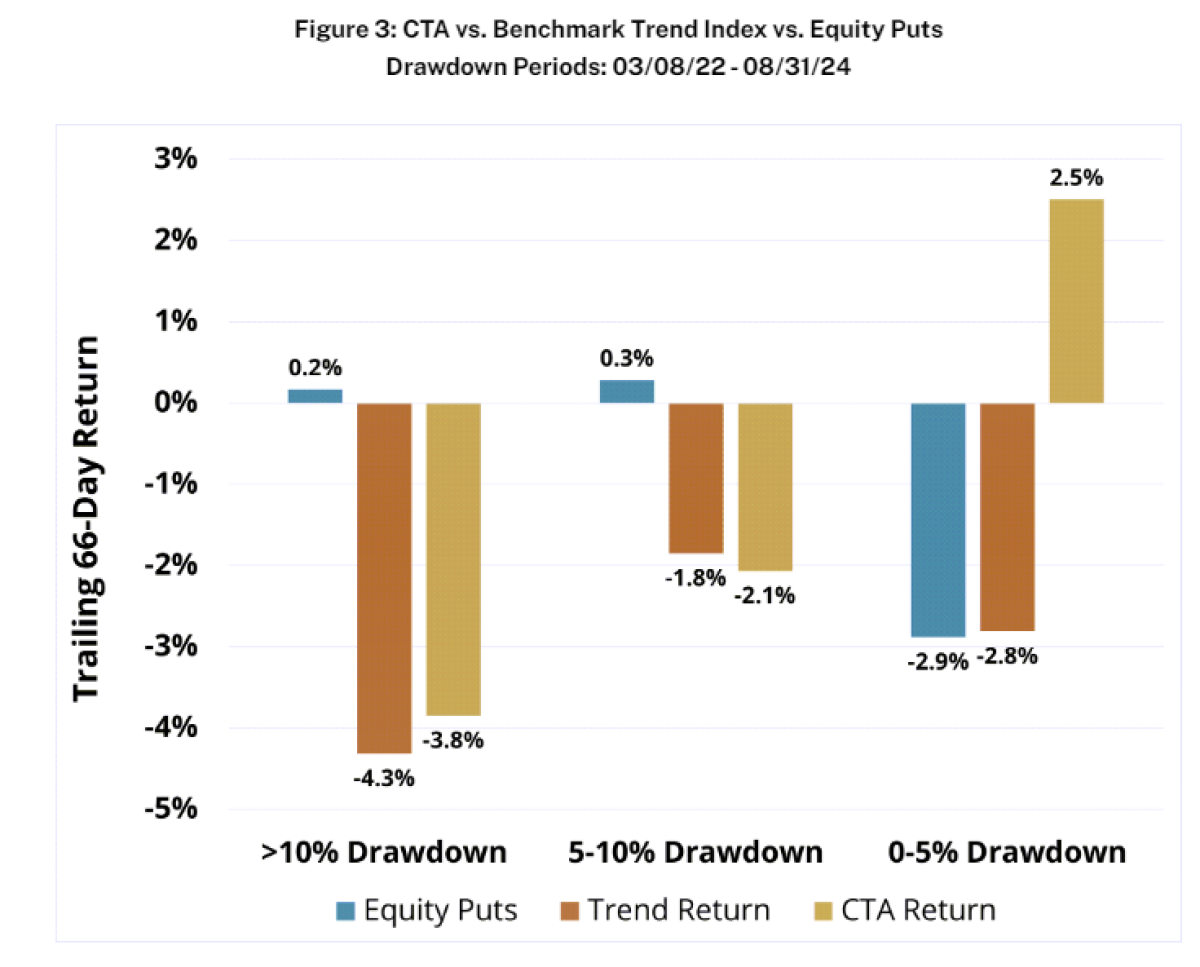

In this Fund Insights post, we discuss how the Simplify Managed Futures Strategy ETF (CTA) offers a compelling solution, providing both diversification and strong performance potential. CTA has not only helped bolster portfolios during an equity market downturn, e.g., 2022 but has also delivered impressive gains in 2024 as stocks have risen. This is shown in Figure 1, where we see CTA’s compelling return profile, which has produced strong absolute returns that can also offset periods when 60/40 portfolios suffer losses.

Negative Correlation When You Need It

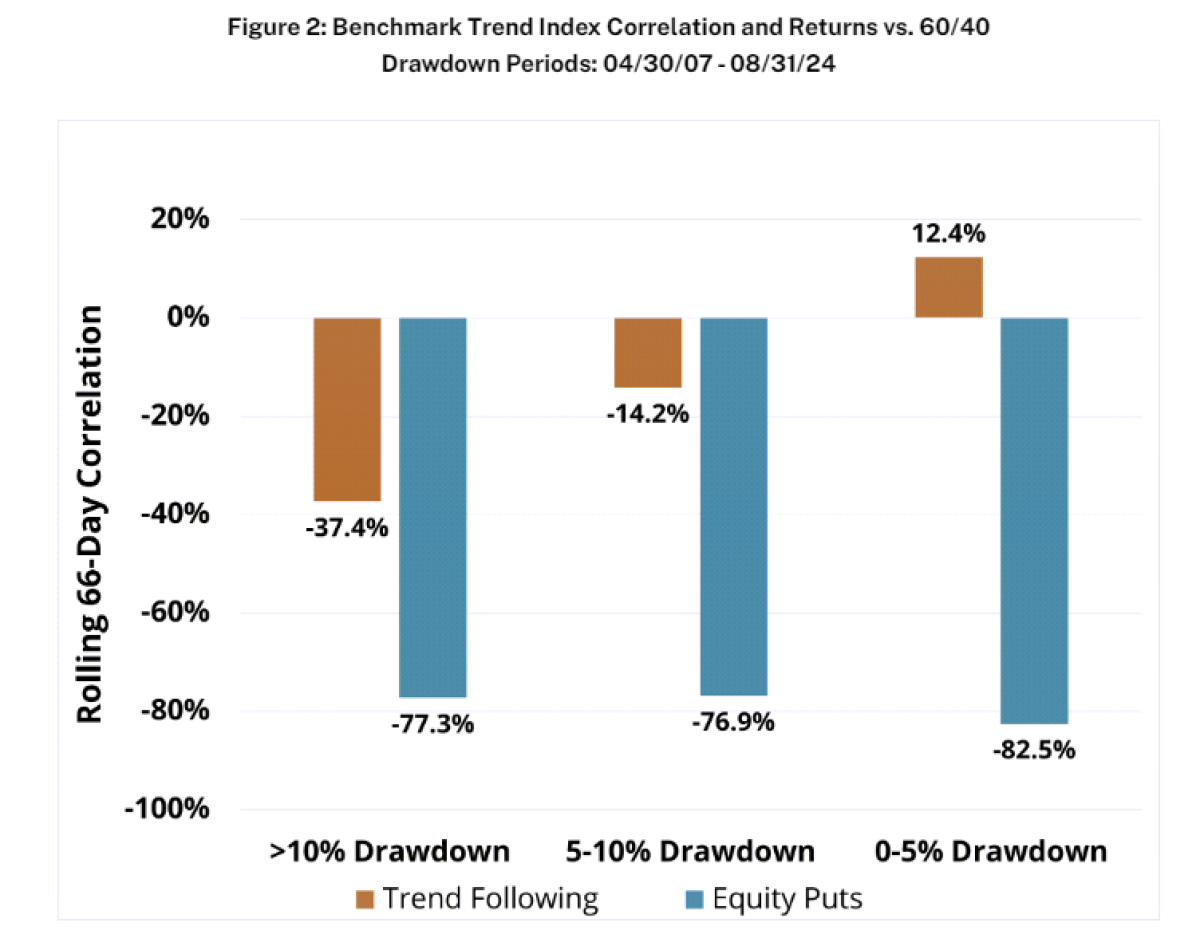

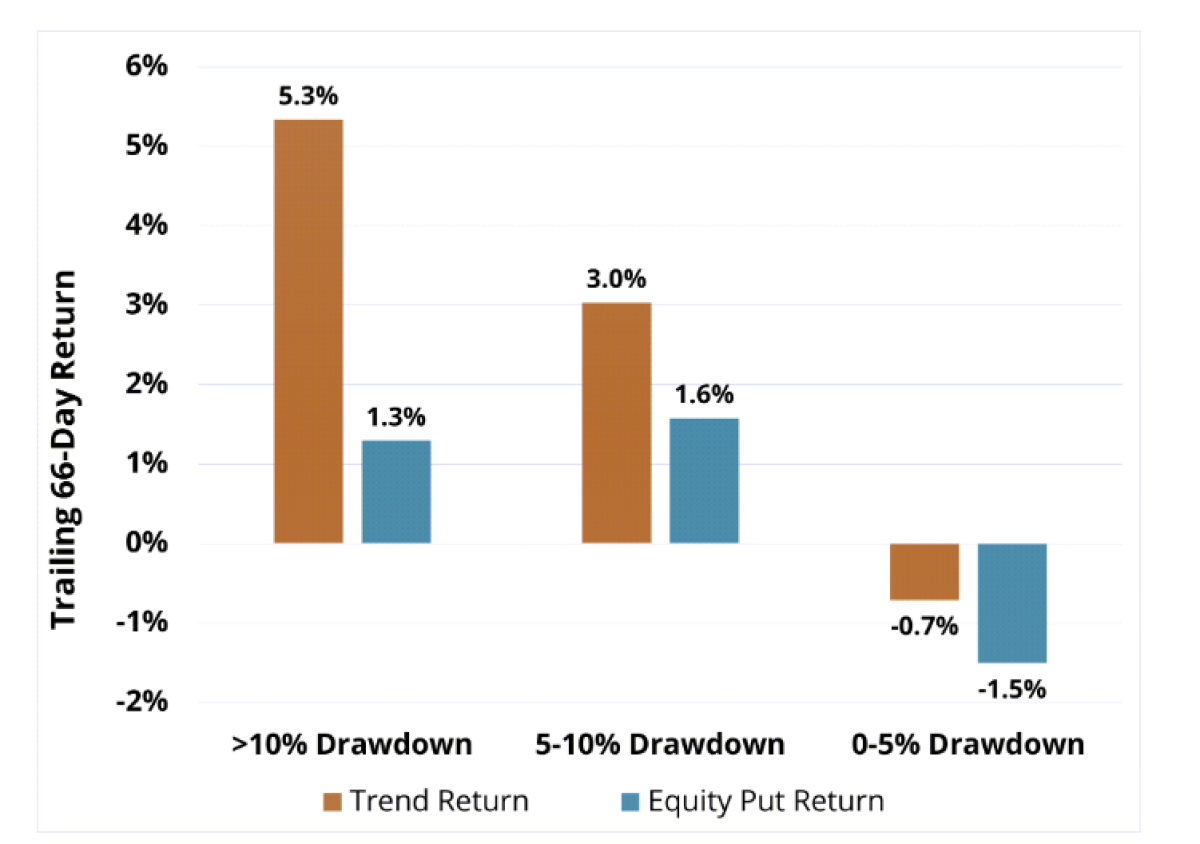

First, a note on what makes Trend-following, which is the primary driver of returns in managed futures, such a game-changer. Trend diversifies your portfolio with a unique convexity strategy. Unlike equity put options, which come with costly premiums and often underperform in choppy or sideways markets, trend strategies offer negative correlation AND increasing exposure (negative beta to the equity market) exactly when it is needed most—during deep market declines. Trend strategies act like an option, offering a hedge and “negative correlation when you need it” without the drag of high ongoing option premium costs, as shown in Figure 2 below.

All Other Times

But where do returns come from in more normal equity and rate markets, when a trend model is not generating convexity? Well, one can certainly have other assets trending while the core 60/40 is going about its normal course of business, e.g., CTA can trend follow in a large number of commodities. Another huge component of the strong absolute returns in CTA is the exploitation of structural carry opportunities across rate and commodity futures markets. Let’s dig into this feature a bit more now.

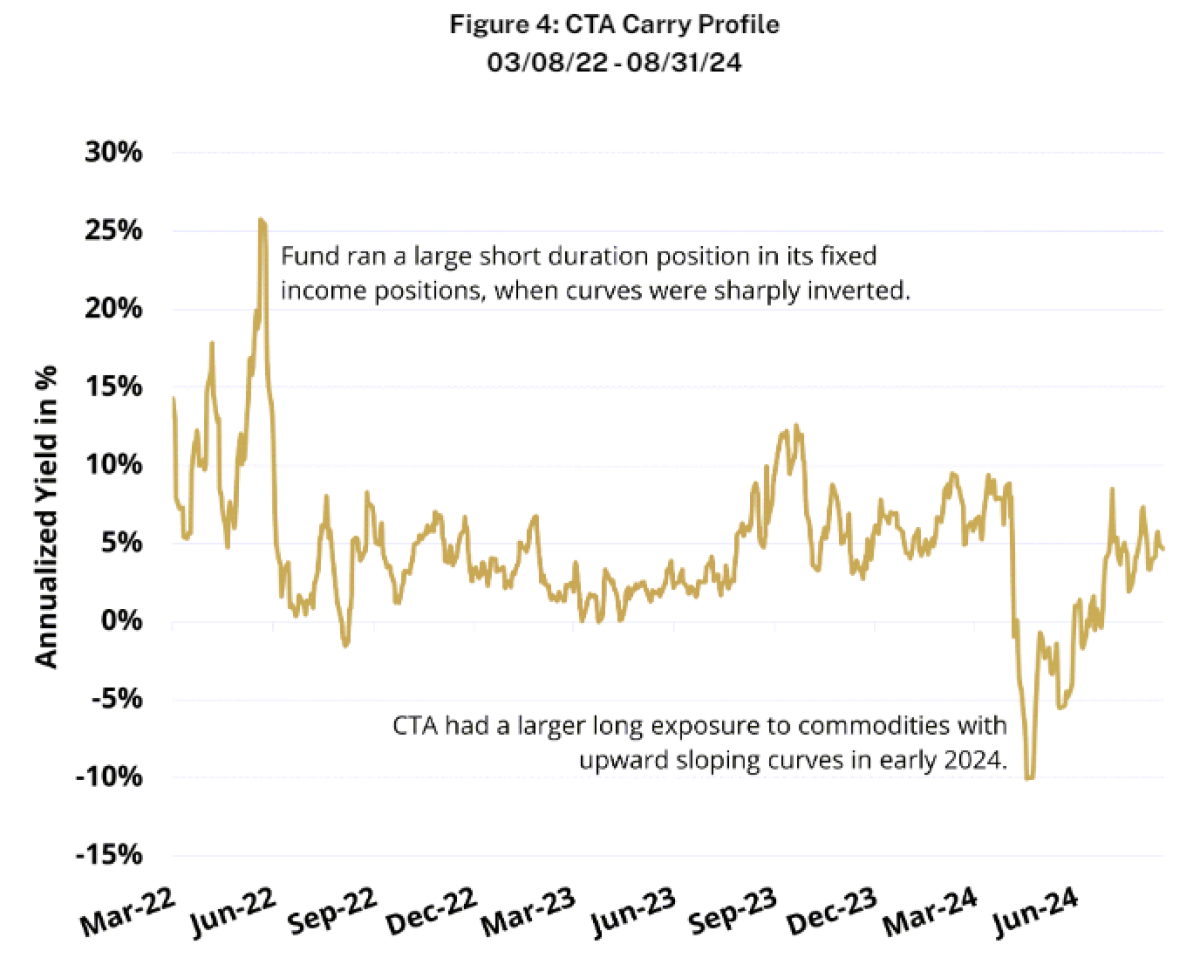

All futures markets have a “forward structure” with prices in the future either higher (referred to as Contango), flat (creatively called “flat”), or downward-sloping (“Backwardation”). The shape of the curve typically represents storage costs, financing costs, and sentiment; but these same factors can be used to generate income (“carry”). Additionally, sharply inverted yield curves can make long duration positions in bonds too expensive to hold while positioned for a decline in rates. CTA incorporates the curve shape in determining the trend and carry positioning biases.

This has been a critical driver of its outperformance. The chart below shows an estimate of fund annual carry or ‘yield’ over time (average 4.6%) and illustrates how active positioning across commodity and fixed-income curves adds to returns. From a return contribution standpoint, this was most evident since inception in the fund’s underweight position to the US yield curve front-end, where the sharp inversion and stubbornly high inflation prints made it very difficult for long positions in bonds to ‘beat the forwards’ and generate alpha.

All Other Times

But where do returns come from in more normal equity and rate markets, when a trend model is not generating convexity? Well, one can certainly have other assets trending while the core 60/40 is going about its normal course of business, e.g., CTA can trend follow in a large number of commodities. Another huge component of the strong absolute returns in CTA is the exploitation of structural carry opportunities across rate and commodity futures markets. Let’s dig into this feature a bit more now.

All futures markets have a “forward structure” with prices in the future either higher (referred to as Contango), flat (creatively called “flat”), or downward-sloping (“Backwardation”). The shape of the curve typically represents storage costs, financing costs, and sentiment; but these same factors can be used to generate income (“carry”). Additionally, sharply inverted yield curves can make long duration positions in bonds too expensive to hold while positioned for a decline in rates. CTA incorporates the curve shape in determining the trend and carry positioning biases.

This has been a critical driver of its outperformance. The chart below shows an estimate of fund annual carry or ‘yield’ over time (average 4.6%) and illustrates how active positioning across commodity and fixed-income curves adds to returns. From a return contribution standpoint, this was most evident since inception in the fund’s underweight position to the US yield curve front-end, where the sharp inversion and stubbornly high inflation prints made it very difficult for long positions in bonds to ‘beat the forwards’ and generate alpha.

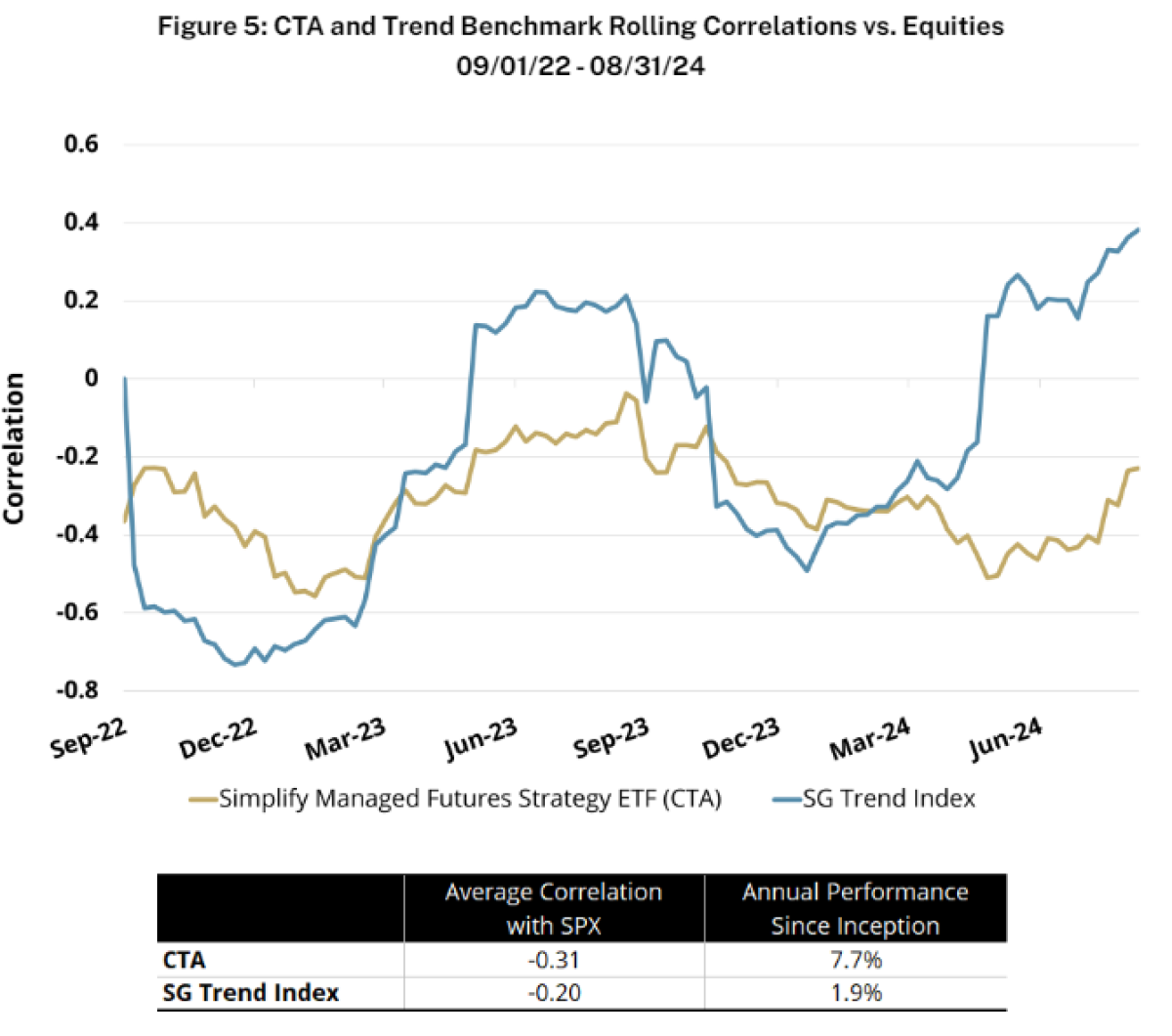

When combining the trend, fundamental reversion, and carry drivers of return in CTA, we see a formidable example of the benefits of low correlation to stocks alongside high annualized total returns, as displayed in Figure 5. Since its inception, CTA has averaged a -0.31 correlation to large cap stocks while displaying an annualized total return of 7.7%, making it a standout in terms of risk management and a constructive participant in both flat and trending markets. Contrast this with the broader trend benchmark, which has exhibited more variance in correlation and lower total returns due to its inclusion of equities and foreign currencies - two markets that CTA omits from its investable universe for this very reason.

Conclusion

By refining the trend following to exclude equities and foreign currencies, CTA improves upon trend-following’s defining feature: low-cost negative correlation to equity markets when needed and positive convexity in the return profile. By pairing this potential protection with a carry strategy that can offer positive returns in various market scenarios, the Simplify Managed Futures Strategy ETF has delivered high annualized returns while diversifying traditional portfolios, making it a “Hedge You Get Paid to Own.”

About the Authors:

Ken Miller has more than 20 years experience as a Portfolio Manager and Trader, designing and implementing global macro and systematic strategies for a range of institutional investors. Most recently at Longtail Alpha he formulated both absolute return strategies for unconstrained accounts and tail-risk hedge solutions to add alpha versus passive hedge benchmarks. He has developed cross-asset research and custom portfolio optimizations to meet specific client objectives, applying the results of analyses of major market drawdowns including 2008 and the 2020 episodes.

In his prior role at PIMCO, Ken managed G10 bond portfolios and traded equity, fixed-income and FX derivatives across the firm’s accounts. Ken engaged frequently with PIMCO’s Investment Committee to debate global macroeconomic portfolio strategy and to tailor and integrate investment positioning for portfolios. He was the lead portfolio manager on the firm’s $100 billion G10 currency overlay funds platform, for which he designed and managed the product’s evolution and its analytics since inception in the early 2000s. Other areas of focus include non-dollar macroeconomic strategy, FX research and options trading, and supranational/sovereign debt research and portfolio strategy.

Ken holds an MBA from the Marshall School at the University of Southern California and an undergraduate degree in Applied Mathematics from UC Berkeley, and is also a CFA holder. He lives in Coto de Caza, California with his wife, and has three adult daughters. In his spare time he is a competitive triathlete, having completed the San Francisco bay swim from Alcatraz; and has served on the board of local non-profit organizations and has done relief work in Haiti.

Michael Green, CFA, has been a student of markets and market structure, for nearly 30 years. His proprietary research into the shift from actively managed portfolios and investment funds to systematic passive investment strategies has been presented to the Federal Reserve, the BIS, the IMF and numerous other industry groups and associations.

Michael joined Simplify in April 2021 after serving as Chief Strategist and Portfolio Manager for Logica Capital Advisers, LLC. Prior to Logica, Michael managed macro strategies at Thiel Macro, LLC, an investment firm that manages the personal capital of Peter Thiel. Prior to Thiel, Michael founded Ice Farm Capital, a discretionary global macro hedge fund seeded by Soros Fund Management. From 2006-2014, Michael founded and managed the New York office of Canyon Capital Advisors, a $23B multi-strategy hedge fund based in Los Angeles, CA, where he established their global macro strategies, managing in excess of $5B of exposure across equity, credit, FX, commodity and derivative markets.

In addition to his work as a market theorist and portfolio manager, Michael has been noted for his work as a public speaker and financial media participant. He is a graduate of the Wharton School at the University of Pennsylvania and a CFA holder.