A new report by Greenwich Associates looks at the pros and cons of central clearing from the point of view of participants in the interest-rate derivatives markets.

A new report by Greenwich Associates looks at the pros and cons of central clearing from the point of view of participants in the interest-rate derivatives markets.

The report is the result of a two-round survey. First, in 2014, GA interviewed 4,036 global fixed-income investors about their dealer relationships and use of various fixed-income products including interest-rate derivatives.

Separately, GA conducted another 72 more in-depth interviews about market participant “views on systemic risk, the impacts of central clearing and … expectations for the interest-rate derivatives market going forward.”

The participants came both from Europe (taking that term in its broadest sense) and the U.S. More than two fifths come from Europe (in the narrower sense), other statistical chunks hailed from the U.K. and the Nordic countries.

The Basics

The Basics

GA begins with the basics. Clearinghouses serve as the buyer to every seller and the seller to every buyer, turning a market that would otherwise be a patternless web into a multi-spoke wheel. Mandating this is an experiment, and the point of the experiment, of course, is the reduction of counterparty risk. Some participants will still default, but the burden of managing that risk is taken off the shoulders of other participants, because it is borne by the CCH itself.

Swaps-clearing mandates are now expanding the clearinghouses “well beyond levels the market has ever seen,” says Greenwich.

Some benefits that come from such a mandate go beyond the insurance-scheme aspect. They include overall market transparency, a definitive source for mark-to-market valuation, and a broadly more efficient market.

Costs v. Benefits

But it is all still something of an experiment, with costs as well as benefits, and with some uncertainty as to the ratio. The costs associated with central clearing have combined with the expectations that costs will increase also for swaps investors due to the Basel III capital rules, and the one-two punch has caused some anxiety. A majority of respondents answered “yes” to the question, “is the cost of mandatory clearing outweighed by the benefits it brings to your firm?” But it was only a bare majority: the question generated a 52/48% split.

Polarizing as that sounds, only 11% of respondents expect to reduce their use of interest-rate derivatives. Volumes in both Europe and the U.K. increased in 2014.

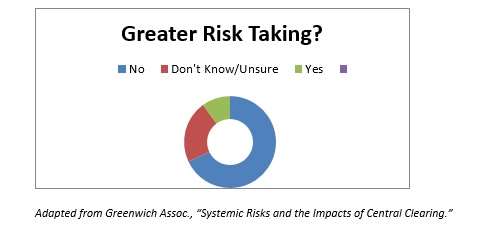

Is the extra security of central clearing creating a moral hazard, that is, more risk taking activity? Based on self reporting, it seems that consequence is slight. As indicated in the donut below, only 10% say they have taken on greater risk as central clearing has ramped up.

To the extent that participants do increase their risk taking, then it seems possible the greater risk is being shifted to the CCHs. Can they handle it? Are the clearing institutions themselves the new “too big to fail” entities of the international financial system?

The GA report allows its interviewees to speak to this issue as well. Sixty-nine percent of investors believe that the major clearinghouses now possess adequate financial resources to deal with a catastrophic event, in particular a “major multiple bank default.”

When asked what reforms might make it even less likely that a clearinghouse will fail, majorities favored two proposals in particular: that clearinghouses be allowed access to central bank liquidity, and that they have more “skin in the game.”

These are both, as GA says, “hot button” ideas.

In the United States, the major clearinghouses have been designated Systemically Important Financial Market Utilities (SIFMU), which would in fact and in accord with the first of those ideas allow them access to Federal reserve liquidity during a crisis.

Waterfalls

In the view of the author of this paper, GA’s Kevin McPartland, many institutional investors still fail to understand the specifics of how individual clearinghouses would absorb defaults, that is, their default-management “waterfalls.” Indeed, they say so themselves. Only 19% of investors who do business with the LCH say that they have a “strong understanding” of the waterfall of that CCP.

On a scale of 1 to 5, in which 5 represents “very familiar” and 1 represents the highest level of ignorance, 5 and 4 together added up to only 33% of those respondents who deal with the LCH.

Respondents whose clearing is done by others of the major houses were still less likely to consider themselves to have a strong understanding of the pertinent waterfall.

McPartland’s bottom line, though is that “the financial markets are in a safer place today than they were before the financial crisis,” in part because the central clearing of central derivatives has led the “charge toward systemic risk reduction.”