By Andrew Smith, CAIA Given the recent economic turmoil globally, the low interest rate environment, and a search for safety as well as yield, many institutional investors have been looking to real assets. One sub class of real assets that is becoming more popular is farmland, with institutional investors expected to drastically increase their allocations to the asset class for many years to come. While farmland is becoming more popular, the investor public, both retail and institutional, questions the best way to access farmland, and whether to invest in cropland, pastureland or a combination of the two. This article is the first of a series of four articles and focuses on the first of three ways to access farmland, buying directly. In this article we focus on the returns, barriers to entry and risks involved when purchasing farmland directly.

By Andrew Smith, CAIA Given the recent economic turmoil globally, the low interest rate environment, and a search for safety as well as yield, many institutional investors have been looking to real assets. One sub class of real assets that is becoming more popular is farmland, with institutional investors expected to drastically increase their allocations to the asset class for many years to come. While farmland is becoming more popular, the investor public, both retail and institutional, questions the best way to access farmland, and whether to invest in cropland, pastureland or a combination of the two. This article is the first of a series of four articles and focuses on the first of three ways to access farmland, buying directly. In this article we focus on the returns, barriers to entry and risks involved when purchasing farmland directly.

Direct Farmland Investment

The age old method of accessing farmland is to purchase a farm directly. Purchasing a farm directly can be rewarding, both financially and sentimentally, however there can also be significant barriers to entry and risks.

Return Expectations

Return expectations for a direct purchase of farmland can vary based on region and type of farmland (cropland or pastureland), and can be viewed many different ways, from absolute to relative to risk adjusted or factor based, unleveraged or leveraged, total return or price appreciation and yield separately, and lastly IRR or Compound Annual Growth Rate. These different measures may be more or less important to different investors, therefore we will look at all the above mentioned historical returns and volatility, and then extrapolate based on certain factors return expectation ranges for farmland in total. We determine “farmland in total” by value weighting regionally each sub class (cropland vs pastureland) and then value weighting each sub class.

Absolute Returns

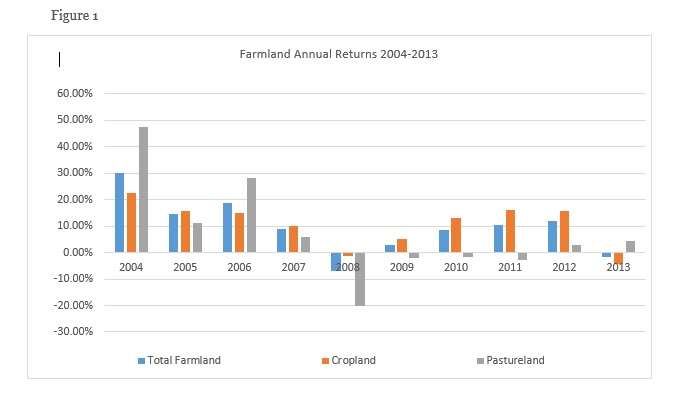

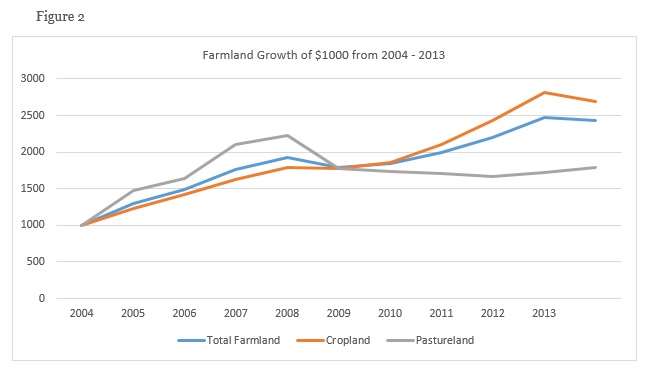

Absolute returns measure the non-risk adjusted annual and total returns of an asset, without comparing the returns to another asset. Absolute returns are a good measure to start with when analyzing an investment opportunity. Absolute returns do not determine how an investment fits within a portfolio, nor does it aide in determining the potential future expected returns. Direct Farmland investment, from an absolute return perspective generated a weighted average return 9.72% annually from 2004 – 2013. A $1,000 direct investment in farmland, in 2004 would have led to a value of $2,428 in 2013. Figure 1 shows the annual return of farmland (in total), cropland and pastureland from 2004-2013. Figure 2 shows the growth in value of a $1,000 direct investment in farmland (in total), cropland and pastureland in 2004.

Relative Returns

Relative returns are a measure of one asset’s (or asset class’) return as compared to, or relative to, another asset (or asset class’) returns. Figure 3 shows Farmland Returns, S&P returns, and the difference between the two, each year from 2004-2013. Figure 4 shows the value of $1,000 invested in the S&P 500 vs $1,000 invested in direct farmland from 2004-2013, as well as the difference between the accumulated value between the two investments. Farmland has outperformed the S&P 500 on average from 2004-2013 by 267 basis per year. A $1,000 direct investment in farmland in 2004 would have grown to $2,428 by the end of 2013, whereas a $1,000 investment in the S&P 500 in 2004 would have grown to $1,797 over the same period. That is a difference of 6,311 basis points or approximately $631 for every $1,000 invested.

Risk Adjusted

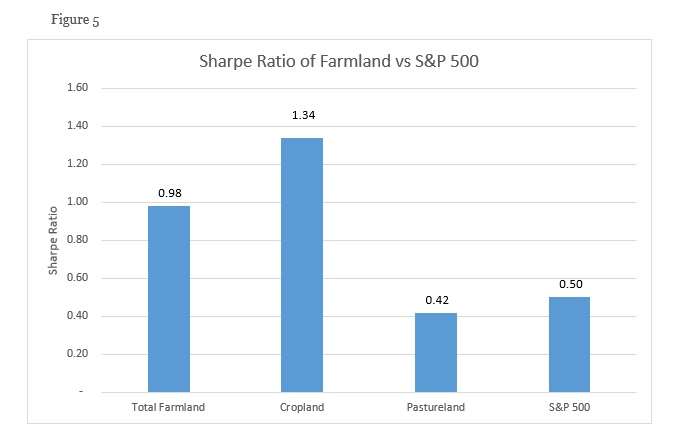

Risk adjusted returns are typically calculated using a ratio, most commonly a Sharpe Ratio, calculated as Sharpe Ratio=(Mean Return-Risk Free Rate)/(Standard Deviation) This ratio looks at the return of an asset per unit of volatility. There are also other risk adjusted return measurements, such as the Sortino Ratio and Return/Drawdown ratio. For the sake of keeping this article concise, we will focus on the Sharpe ratio. Farmland carried a Sharpe Ratio of 0.98 from 2004 to 2013. Cropland specifically has generated a Sharpe ratio of 1.34. Pastureland specifically carried a Sharpe ratio of 0.42. Compare these numbers to the Sharpe ratio of the S&P 500 over the same time which was 0.5.

Leveraged

Leveraged investments use debt to purchase an asset that is expected to appreciate by more than the interest rate. For the leveraged returns of a direct farmland investment, we have assumed that the loan is fully amortizing over a 20 year period, that the interest rate is 5%, require a 30% down payment, and that the returns are measured as total returns, that is that the income generated from the investment is reinvested into new direct purchases. We then look at the returns on an absolute, relative and risk adjusted basis. For absolute returns, we measure the returns from both a percentage return annually, as well as a dollar return over the life of the investment. We also compare these returns to the returns on an investment in the S&P 500 over the same time period, using the same amount of leverage. We also look at absolute and relative returns on an annual basis, as well as over the life of the investment, for the sake of this article, the life of the investment is from the beginning (January 1) 2004 to the end (December 31) 2013.

Absolute

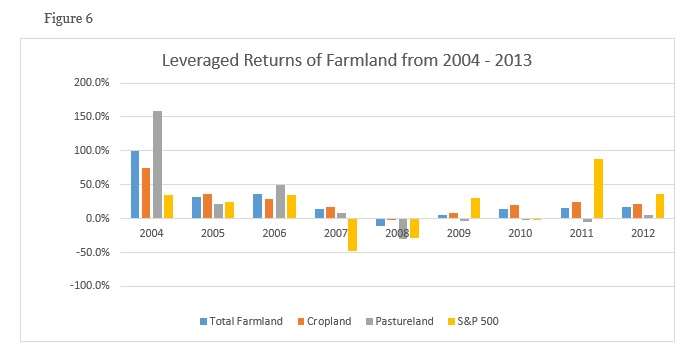

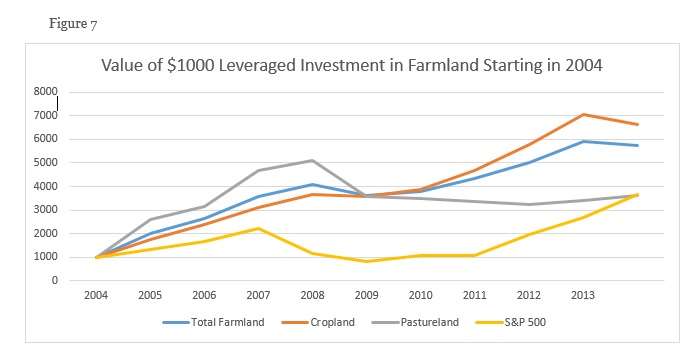

From an absolute return perspective, leveraged total farmland (70% cropland, 30% pastureland) returns averaged 24.73% and ranged from 100.1% to -10.9%. Leveraged cropland returns alone averaged an annual return of 25.78%, ranging from 75.0% to -2.0%. Leveraged pastureland annual average returns were 22.57% with a range of 158.4% to -29.5%. During the same time period, assuming the same amount of leverage, S&P 500 returns were 18.69%, with returns ranging from 88.1% to -48.3%. At the end of 2013 a $1,000 leveraged investment in total farmland made at the beginning of 2004 would have been worth nearly $6,000, while a leveraged $1,000 investment in cropland alone would have been worth nearly $7,000. A leveraged $1,000 investment in pastureland and the S&P 500 would have grown to slightly more than $3,500 during the same time frame, figures 6 and 7 below show these results graphically. You may notice that annual returns of pastureland are 4% higher, however due to the power of compounding returns the total returns of pastureland are very similar to those of the S&P 500. It is very important as an investor to consider the power of long-term compound returns, not just average annualized returns, when making an investment of any kind.

Relative

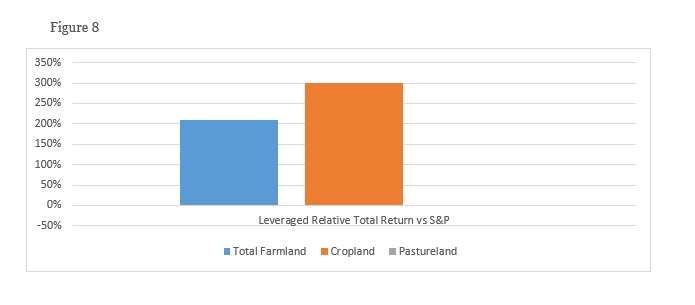

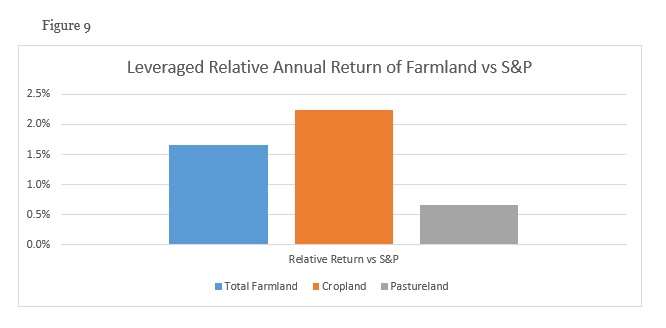

Relative leveraged returns of farmland, as compared to the S&P show that both total farmland and cropland alone outperformed the S&P 500 significantly from 2004 – 2013, while pastureland slightly underperformed the S&P 500 during the same time period. Leveraged total farmland outperformed the S&P 500 from 2004 – 2013 by over 20,000 basis points, while leveraged cropland outperformed the S&P 500 by nearly 30,000 basis points over the same time period. Pastureland however, underperformed the S&P 500 over the same time period, but only slightly. On an annualized basis, leveraged total farmland outperformed the S&P 500 by over 150 basis points, and leveraged cropland outperformed the S&P 500 by over 220 basis points. Leveraged pastureland, on an annualized basis, outperformed the S&P 500 by over 65 basis points. These results are represented graphically by figures 8 and 9.

Risk-adjusted

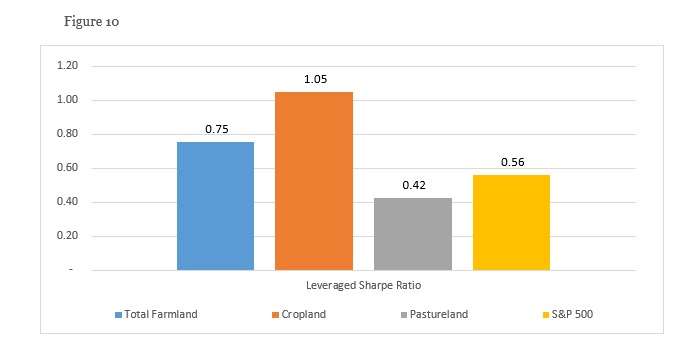

Leverage can affect risk adjusted returns much differently than it does absolute or relative returns. Consulting figure 5, and comparing it to figure 10 below, you will see that leverage lowered risk adjusted returns for both total farmland and cropland, while slightly increasing the risk adjusted returns of the S&P 500. Pastureland risk adjusted returns over the time frame measured were not affected by the use of leverage. Unleveraged risk adjusted returns for total farmland carried a Sharpe ratio of 0.98, while leveraged total farmland risk adjusted returns exhibited a Sharpe ratio of only 0.75. For total farmland, unleveraged risk adjusted returns were 30.7% higher than leveraged total farmland risk adjusted returns. The unleveraged cropland Sharpe ratio was 27.6% higher (1.34) than the leveraged cropland Sharpe ratio (1.05). Pastureland, as mentioned before, was unaffected by leverage, with both unleveraged and leveraged Sharpe ratios at 0.42, while the S&P 500 exhibited risk adjusted returns that were 12% higher when leveraged with a leveraged Sharpe ratio of 0.56 compared to an unleveraged Sharpe ratio of 0.5. Investors should consider the effects of leverage on absolute, relative and risk adjusted returns before deploying leveraged capital to an asset. Figure 10 shows the leveraged risk adjusted (Sharpe ratio) returns of total farmland, cropland, pastureland and the S&P 500. Figure 5 show the unleveraged risk adjusted (Sharpe ratio) returns of the same assets.

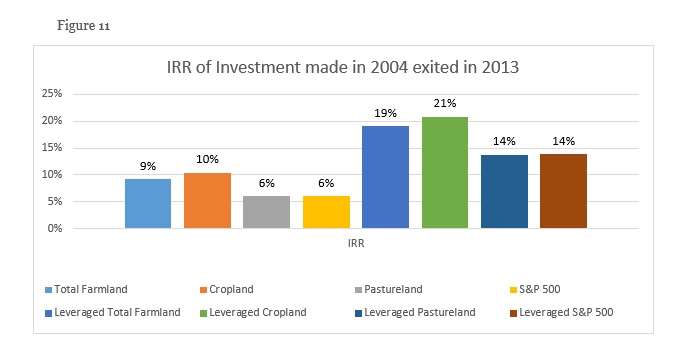

IRR

When measuring returns of real estate, real assets and private equity, the Internal Rate of Return (IRR) is often used. IRR is the discount rate that equates the net present value of an investment to 0. While considered flawed by many, it is still extremely common and popular among investors making private real estate, real asset or private equity investments. For the sake of the article, when measuring the IRR, we assumed a total return framework for measuring returns, that is that the income in between acquisition and exit of the asset was reinvested, therefore there are only two non-zero cash flows in the calculation, the initial negative cash flow and the positive cash flow at exit. For the IRR calculation we look at both the unleveraged and the leveraged IRR for Total Farmland, Cropland, Pastureland and the S&P 500. Figure 11 shows the unleveraged and leveraged returns for each asset. As can be seen from Figure 11, when measuring the investment return using IRR, cropland outperformed the other assets, with an unleveraged IRR of 10% and a leveraged IRR of 21% on a direct investment made at the beginning of 2004, exited at the end of 2013. Total farmland exhibited the second largest IRR with an unleveraged IRR of 9% and a leveraged IRR of 19%. Pastureland and the S&P 500 both demonstrated similar IRR returns over the time frame measured both exhibiting an unleveraged IRR of 6% and a leveraged IRR of 14%.

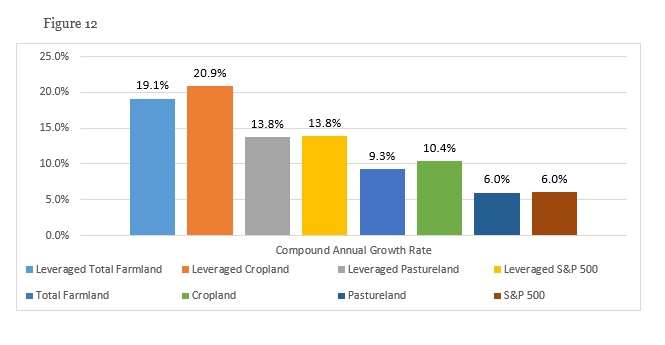

Compound Annual Growth Rate

To most long term investors, the compound annual growth rate is the most important performance metric for an investment. For the compound annual growth rate we measure both leveraged and unleveraged returns of total farmland, cropland, pastureland and the S&P 500, respectively. Figure 12 shows the compound annual growth rate of each asset, both leveraged and unleveraged in a graph. Cropland, once again, exhibits the highest return; both leveraged an unleveraged, at 20.9% and 10.4% respectively. Total farmland exhibited a CAGR of 19.1% leveraged and 9.3% unleveraged, while both the S&P 500 and pastureland demonstrated leveraged CAGRs of 13.8% and unleveraged CAGRs of 6.0%.  While making a direct investment in farmland can provide significant diversification and return enhancement, there are also some significant risks as well as significant skill required when managing a direct investment in farmland. However, compared to an investment in a farmland fund or a farming company, a direct investment in farmland can carry a large sentimental value.

While making a direct investment in farmland can provide significant diversification and return enhancement, there are also some significant risks as well as significant skill required when managing a direct investment in farmland. However, compared to an investment in a farmland fund or a farming company, a direct investment in farmland can carry a large sentimental value.

Sentimental Value

A direct investment in farmland can give the investor a lot of pride, knowing that they own that specific piece of land that produces or has a large role in the process of producing the food necessary for people across the globe to survive. The investor may also feel safer when buying farmland, as it can be a place to escape to in the event of a natural or man-made disaster. Farmland investments are also often made as both an investment in an asset and a vacation home. Often times investors in farmland use the piece of land to build a home, or renovate an existing home that they and/or their family can vacation to, allowing them to escape the hectic lifestyle of their urban or suburban primary residence. Further, many families have inherited farmland that has been in their family for generations, often homesteaded by ancestors that were among the earliest settlers to the region of the country in which it was located. Farmland can be more than just an asset purchased to benefit an investment portfolio, it can be or can become a family heirloom that generation after generation enjoy escaping to when they need some time away from home.

Barriers to Entry

When buying farmland directly there are some issues and risks that need to be considered carefully. The first group of issues is the barriers to entry. The vast majority of farmland is held privately, often within a family structure, and has often been held by the family for generations. As mentioned earlier, owning farmland directly can carry significant sentimental value, and therefore seldom comes onto the market. Another issue an investor may run into when looking to directly purchase farmland is that it can be a very regionally oriented investment. As such, some level of expertise on the region in which you are looking to purchase is required. Unless the new owner is a farmer, it will be necessary to hire a farm operator/manager, or to lease out the farmland to a local co-op. Finding a trustworthy farm operator or manager, or leasing the farmland out to the right farmer or co-op is not as easy as it may seem, as the farming industry, unlike many other industries, is not one in which a simple online search for a provider will do. Local knowledge, or even better, connections will make the process of finding the right farm operator/manager, farmer or co-op significantly easier. Again circling back to having an expertise in the region in which you plan on owning farmland, local knowledge and/or connections that can aide you in the process of finding the right operator will likely to lead to a better overall experience for the owner.

Risks

As with any investment buying farmland directly carries unique risks, some of which can be significant and lead to losses and/or under-performance. Farmland is a lumpy asset, in which it is not easily divisible. As such, farmland can be extremely illiquid and can take years to sell if the owner plans to exit. A direct purchase in farmland has to be viewed as a long term investment. Owning farmland is essentially owning a business that relies on good weather. Too much precipitation could lead to flooding, which could lead to an inability to grow and harvest a crop. Too little precipitation could cause a drought and make growing and harvesting a crop just as difficult. Other naturally occurring events such as a swarm of locust, or other pest invasion, crop diseases and other factors could lead to a lost year. An investor that owns pastureland faces many of the same issues. Also, issues that affect a crop harvest are likely to drive feed prices up the following year and cut into the already slim profit margins of farmers, making a pastureland owner likely to have to take a haircut on the lease rate. Farmland values and income in the US are insured, and therefore it is often viewed as a very low risk investment. However there are many political analysts who believe within the next few decades, the Farm Bill will not be renewed and that government insurance and subsidy programs for crops and livestock will cease to exits. If these programs go away it may be significantly more difficult for farmers to lease farmland, and a non-farmer owner of farmland may find they are unable to generate the income they desire. Other economic factors such as inflation or deflation could hurt the returns of farmland or lead to investment losses for the owner of farmland. New food regulations, new technology in food processing, loosening of food import regulations, slowing development of emerging and frontier markets, as well as other global macroeconomic factors could lead to lower income, lower value appreciation or even value depreciation in farmland. While historically farmland values have not carried extremely high volatility, those numbers may potentially be hiding something. As with other real estate and real asset investments, farmland prices are often stale and returns are auto-regressive, or in other words, as with many assets that rely on appraisal based pricing, the returns of the current year are often a weighted sum of the returns of past years, with most recent years carrying a larger weight. As we saw with real estate in the most recent economic crisis, in a true downturn, this could lead to fire sales and significant value depreciation. Finally, there is currently no way to hedge the risk of a decrease in income or value on farmland. While that may change in the future, it is important for investors to consider how the inability to hedge would affect their ability to efficiently manage a portfolio in which they directly own farmland. Whenever making an investment, the risks must always be considered in full prior to allocating capital. Conclusion Owning farmland directly can be very rewarding, both financially and otherwise. Farmland returns, both leveraged and unleveraged have outperformed the S&P 500; quite significantly I might add, over the past 10 years. Further, owning a farm that can be passed down to generation after generation can bring a family together, not to mention provide the owner(s) with significant sentimental value as an heirloom and give family members and friends a place to escape their hectic lives in urban or suburban America. Owning farmland can also make one feel safe and secure from potential urban disaster, whether it be man-made or chaos caused by nature, as a farm can be a safe haven to escape to during socially, financially, or politically tumultuous times. Owning a farm can be difficult and risky. Just finding a farm to purchase can carry both a financial and time burden when making due diligence trips to rural areas to see potential purchases. Having regional expertise is often necessary when searching for farms to purchase, when conducting due diligence, and when operating a farm. As with any investment the investor needs to be aware of and consider all the risks carefully. Farmland is illiquid and lumpy, and as a result prices are often stale and returns are lagged. Currently, and for many decades, farmland income has been subsidized and insured by the US government; shifts in the political paradigm may change this within the next couple decades, and could result in significant price and income depreciation. Economic factors as well as other political factors can adversely affect a farmland investment. Inflation or deflation may affect the income and/or value of farmland. Technological advancements in food processing and manufacturing and genetic modifications of seeds typically lead to income and value appreciation for agricultural lands; however preservation technology may decrease the demand for raw food products, and could lead to lower income for farm owners as well as value depreciation. Loosening of food import regulations and a slowdown in the development of emerging and frontier markets are just two of the many economic and/or political factors that could potentially lead to lower income or value depreciation of farmland. While farmland has historically carried fairly low volatility, past performance does not predicate future results. Farmland being illiquid, a downturn in the value trajectory and/or income generated by farmland could lead to fire sales, and thus increased downside volatility as it did with residential and commercial real estate in the most recent economic crisis. With no way to hedge, a farmland investor may potentially be hung out to dry, in a manner of speaking, if this were to happen. Not to overemphasize, but farmland as with most real estate and real asset investments is extremely illiquid. Investors must take a long term approach (10+ years) when allocating capital to the direct purchase of farmland, and must be ready to ride out any short term downturns if they hope to take advantage of the potential financial rewards an investment in farmland can provide. Andrew N. Smith, CAIA is a Co-Founder and Chief Product Strategist for OWLshares and serves as the chairperson of the Steering Committee for the Los Angeles Chapter of the CAIA Association.