By Jeff Cohen, CAIA, Director of Capital Markets Integration and Head of Private Investments Initiatives at the Value Reporting Foundation.

2020 and 2021 were historic years for their level of global regulation related to sustainability disclosure – and more is likely on the way. In the US, the Securities and Exchange Commission’s (SEC’s) 2021 Regulatory Flexibility Agenda highlights disclosure on climate change, human capital, board diversity, cybersecurity risk, and ESG funds as key issues for rulemaking. In fact, Chairman Gary Gensler noted that disclosure rules on climate risk and human capital "will be the initial steps in our broader efforts to update our disclosure regime for modern markets," Indeed, the SEC’s recent consultation on climate change disclosures signaled a commitment by the Commission to give serious consideration to whether, and how, regulation might more effectively address the climate-related information needs of investors. Although any future rulemaking will likely effect publicly traded companies most, the second- and third-order effects on private firms – and their investors – should not be dismissed.

Climate Risk Is Business Risk

What the SEC will require companies to disclose regarding climate remains to be seen. However, it’s nearly certain that any rule will at a minimum call for information that is “material” to investors. In other words, the information about climate-related risks and opportunities most closely linked to a company’s financial condition and operating performance.

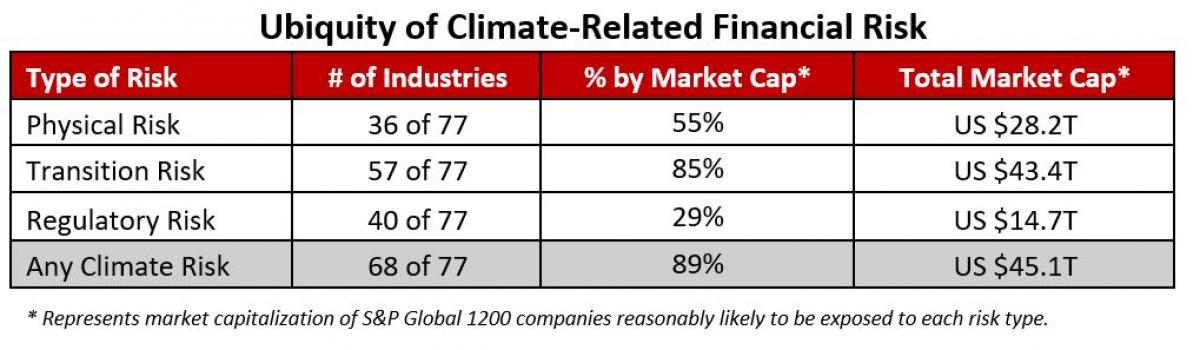

Of course, “climate change” is not just one issue, and the materiality of climate risks cannot be singularly defined. In the context of corporate disclosure, climate change is both ubiquitous and differentiated: although it is likely to have material financial implications in nearly every industry, research finds that it is also likely to manifest differently in each one. (See Figure 1.) For example, an agricultural operation will need to manage water as an increasingly stressed resource while a real estate firm will focus on the energy efficiency of its buildings and the vulnerability of its building stock to extreme weather.

Published in 2021 by the Value Reporting Foundation’s SASB Standards Board, the Climate Risk Technical Bulletin maps financially material climate risks across industries and highlights how company disclosure aligned with SASB Standards and the recommendations of the Task Force for Climate-related Financial Disclosures (TCFD) can help investors better understand, measure, and manage their exposure to climate-related risks and opportunities.

Honing In On Emissions

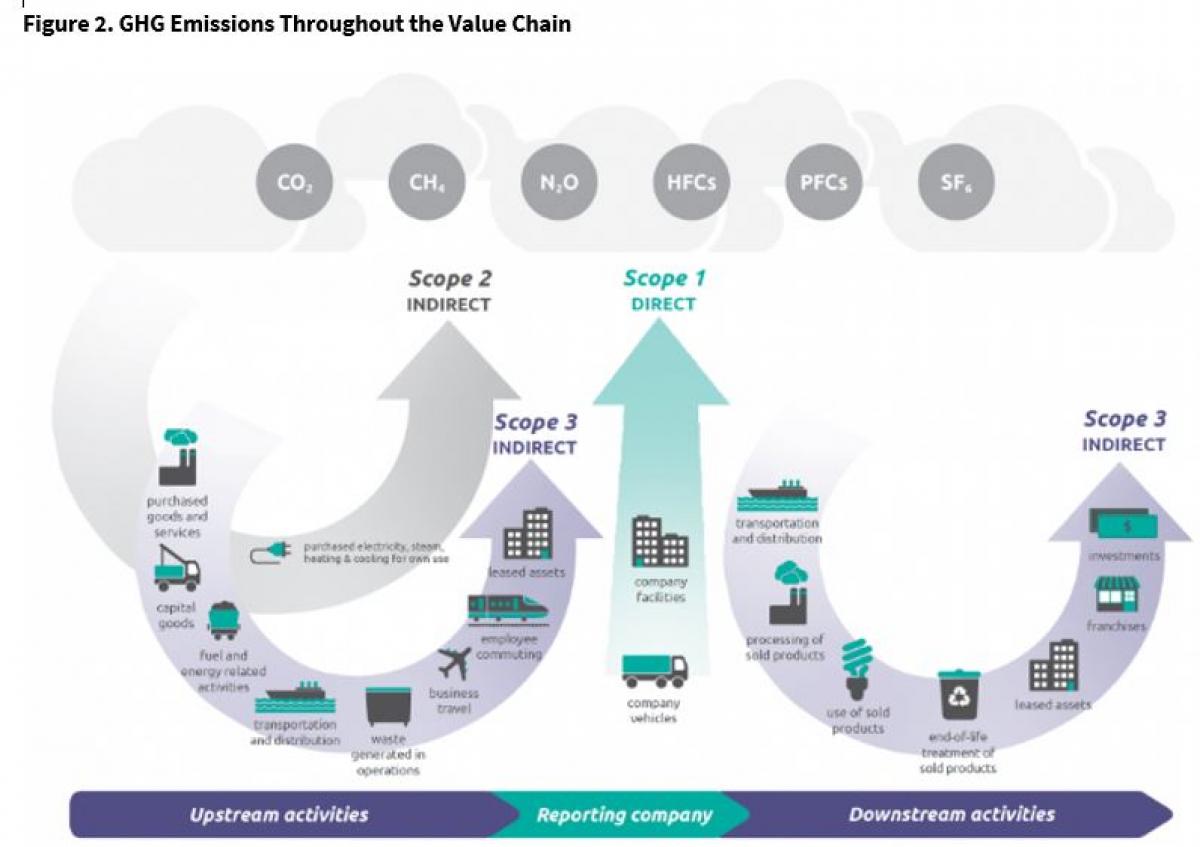

To understand how regulatory efforts around climate disclosure will impact private markets, it’s helpful to first look at just one type of climate risk. The Technical Bulletin identifies transition risk, or the risk that manifests through shifts in market forces, as the most prevalent type of risk companies face related to climate (think of changing regulation and innovation around the transition to lower-carbon economics). Transition risk is closely associated with the greenhouse gas (GHG) emissions intensity of companies’ products and operations. Not coincidentally, such emissions information has become a focal point for many investors and the SEC’s recent consultation. Should Scope 1, Scope 2, and particularly Scope 3 emissions reporting become mandatory for public companies across all industries, it will in effect become required of the private companies in their value chains. (See Figure 2.)

Source: Greenhouse Gas Protocol, “Corporate Value Chain (Scope 3) Accounting and Reporting Standard.”

As shown in Figure 2, a reporting company’s Scope 3 emissions include indirect emissions associated with both upstream and downstream activities and assets. Oftentimes, these emissions fall under the direct control of non-public, privately owned organizations. Should their value chain counterparties mandate or seek collection of emissions data to meet their own regulatory disclosure requirements, these companies would experience a form of knock-on effect, and in turn need to produce emissions data as well.

To help both public and private companies, SASB Standards and the TCFD recommendations offer a cohesive tool. The TCFD includes GHG emissions within its disclosure recommendations. SASB Standards offer further guidance for companies that wish to produce Scope 1, 2, or 3 GHG emissions data and identify the industry-specific ways in which they can be most effectively managed, including through energy and product lifecycle management.

Ripple Effects in Private Markets

Identifying emissions sources throughout the value chain also helps us identify disclosure responsibilities throughout the value chain, however for private companies the knock-on effects of ESG regulation are not the only factor driving demand for ESG disclosure. Consider the following: Walmart’s network contains over 2,800 suppliers. Amazon has more than 1.5 million active sellers on its marketplace. These business networks include a wide range of companies – including private companies owned by general partners (GPs). At the same time Walmart and Amazon may be required to request and disclose emissions data from their suppliers and sellers, the GPs of those suppliers and sellers also face increasing demand from their limited partners to disclose emissions and other climate-related information on portfolio companies. Both seek to communicate the climate change information relevant to interpreting future performance.

In this context, it’s important to note that when a sustainability issue is likely to have material financial implications for a firm, gathering data and other intelligence to better understand its associated risks and opportunities is simply good business. Reporting on and managing climate issues yields benefits beyond meeting ESG questionnaire requirements, both for the businesses themselves and the economies in which they operate.

For instance, food retailers source merchandise from a wide range of suppliers. These suppliers face a myriad of sustainability-related challenges, such as resource conservation, water scarcity, animal welfare, fair labor practices and, of course, climate change. These issues affect the price and availability of food. For example, in response to ongoing drought conditions, some almond growers in California have reportedly uprooted trees that they can no longer maintain. At scale, water scarcity can lead to the impairment of a core asset (in this case, tree stock), limit production output, and contribute to inflated almond prices. In light of such risks, consumers are increasingly concerned with the sustainability attributes of food products, like production methods, origins, and externalities associated with the foods they purchase, which may affect a company’s reputation. Companies that address product supply risks by assessing and engaging with suppliers, implementing sustainable sourcing guidelines, and enhancing supply chain transparency will likely be better positioned to improve supply chain resiliency, mitigate reputational risks, and potentially increase consumer demand or capture new market opportunities.

Meanwhile, a supplier to food retailers may find opportunities to enhance its shelf space and capture greater market share by leveraging SASB Standards and the TCFD recommendations to provide greater transparency around how it manages its own climate-related risks and opportunities. In either case, when private companies and their GPs are proactive in managing and collecting data on these issues, they can better satisfy the informational needs stimulated by regulators and LPs in a way that also benefits their business.

Materiality: A Win-Win

The Value Reporting Foundation, formed by the recent merger of the SASB Foundation and International Integrated Reporting Council (IIRC), supports the SEC’s increased interest and initiative in the area of sustainability-related financial disclosure and believes generally accepted sustainability disclosure standards can play a key role in addressing the clear market need for consistent, comparable, reliable sustainability information that is material to investment decision making. In fact, more than 225 asset owners and asset managers, representing approximately $72 trillion in assets under management across Asia, Europe, the Middle East, North America, and South America participate in the SASB Alliance, or have licensed SASB Standards for use in investment tools and processes.

To ensure that our views appropriately reflect those of market participants, we engaged with companies, investors, trade associations, and other experts to absorb a broad range of perspectives on SEC action and identify key areas of general agreement. Through this approach—which in many ways mirrored the consensus-building efforts that drive our standard-setting process—we submitted our response to the SEC’s request for input on climate change disclosures highlighting the following key points, among others:

- The SEC should facilitate investor-focused disclosure on the sustainability issues reasonably likely to be financially material for the typical company in an industry;

- Financially material sustainability information is market infrastructure essential to making informed investment decisions;

- Industry-specific disclosure is critical to investment decision making, including with respect to climate risk;

- The SEC should leverage existing standards and frameworks (including SASB Standards and the TCFD recommendations) to establish a common structure for sustainability-related financial disclosure that includes an appropriate mix of qualitative and quantitative information, as well as cross-industry and industry-specific metrics.

With these recommendations, we believe the SEC can develop an approach to sustainability-related financial disclosure that effectively serves its tripartite mission: to protect investors; maintain fair, orderly, and efficient markets; and facilitate capital formation. This outcome would address a clear and pressing market need, providing investors with decision-useful information in a manner that is cost-effective for companies.

Conclusion

Private companies should prepare now for the imminent ripple effects of disclosure requirements targeting public companies. Fiscal sponsors supporting these companies can leverage existing, market-tested tools like the SASB Standards and the TCFD recommendations to simultaneously help their publicly-traded business partners meet pending regulatory obligations and to better position their companies for sustained growth and profitability.

About the Author

Jeff Cohen, CAIA is the Director of Capital Markets Integration and Head of Private Investments Initiatives at the Value Reporting Foundation (Merged organization of the SASB Foundation and International Integrated Reporting Council). In his role, Mr. Cohen works with institutional investors and asset owners, facilitating integration of financially material, industry-specific ESG factors into investment decisions across asset classes. Prior to joining SASB, Mr. Cohen was Head of Business Development at Sonen Capital, an ESG & Impact dedicated OCIO and fund manager. Prior to Sonen, he was a Director of Investment Opportunities at Venovate where he led due diligence on alternative investment strategies ranging from timber, real estate, hedge funds, and secondary strategies. Mr. Cohen has spent his career working with sophisticated investors at organizations such as Deutsche Bank, Merrill Lynch, and Gerson Lehrman Group. He holds an MBA from Georgetown University and a BBA from the University of Michigan. Mr. Cohen is a CAIA Charterholder and FSA Credential Holder.