By Dan Krivinskas, Head of Real Estate Research, Aksia.

During the depths of the COVID-19 crisis in 2020, the world’s largest traditional hotel chain, Marriott International, reported that the pandemic had “a more severe and sustained financial impact on Marriott’s business than 9/11 and the 2008 financial crisis, combined”[i]. According to metrics compiled by STR, occupancy in 2020 fell 33.3% from 2019’s level to 44%. Average daily revenue (ADR) dropped 21.3% to $103.25. Revenue per available room (RevPAR) declined 47.5% to $45.48[ii]. It’s no surprise that the American Hotel and Lodging Association (AHLA) reported that the sector has lost nearly 5 million jobs and the economic impact on the industry was “nine times greater” than the September 11 attacks[iii]. The year was just as bleak in most Asian and European markets, where we saw similar—and in some cases, more severe—impacts from COVID-19.

The implications for managers in the hotel space have been severe—delinquency rates of hotel commercial mortgage-backed security loans are at an all-time high, more than double the highest volume of delinquent hotel loans during the financial crisis more than decade ago. GPs have been rattled. For full-year 2020, hotel deals were down 52% from 2019 — with 79 single-asset trades compared to 164. Total transaction volume was $5.3 billion in 2020 compared to $17.7 billion in 2019, a decline of 70%, and the average sale price per key was $273,000 in 2020 compared to $364,000 in 2019, a 25% decline. A surprisingly large number of transactions—8%—were properties that are going to be repositioned or turned into an alternative use (e.g., converted into apartments or repurposed by the government for at-risk housing)[iv].

Some properties have sold for discounts as high as 40% compared to 2019 levels, but there are far fewer transactions that many distressed managers had initially anticipated during the depths of the COVID-19 crisis. Indeed, most “stressed” hotels are not transacting at all. Many owners have worked out forbearance agreements, and the question about whether lenders will actually foreclose is very much in the air. We believe it could be a compelling opportunity for managers who have raised significant capital geared toward distress opportunities. The good news is that COVID-19 cases are in steep decline, and there has already been a huge bounce in hotel occupancies and rates in 2021. We believe that 2021 and 2022 could be some of the best years to be a hotel owner, particularly in “drive-to” and “leisure” destinations, given that many families can attest to wanting to “get out of the house” (the definition of “pent-up” demand, as any parent can attest to).

Look at the Long-Term Supply Fundamentals . . . And Be Critical of Hoteliers Ability to Consistently Charge Silly Rates

Since the entry of Airbnb into the hospitality industry in 2008, many have claimed that Airbnb offers a supplementary service, not a competitive service, to hotels. But there is increased evidence that it does, particularly in markets with high average revenue per available room (RevPAR) rates. And that impact varies across different segments of the industry.

Customers make comparisons, so Airbnb’s listings/offers are increasingly seen as substitutes for hotel rooms. The higher the average satisfaction score of an Airbnb property, the lower the RevPAR for hotels in the area. More specifically, every increase in the review score of an Airbnb property had a negative impact of -$25.54 on hotel RevPAR. Hotel managers therefore need to be aware of the level of service and price offered by Airbnb and other sharing platforms in their market. In the Austin market, where Airbnb has the highest supply/penetration rate, hotel revenue is negatively impacted by 8% to 10%[v].

Obviously, Airbnb offers in a locality can no longer be ignored and should be considered when developing revenue management strategies. Hotels have long relied on popular one-time or annual events that attract big crowds like the Sundance Film Festival, Kentucky Derby and Lollapalooza to get some of their highest room rates of the year. The industry buzzword for this is “compression nights,” and they have long served as opportunities for hoteliers to achieve peak pricing. But this is changing—during the pope’s visit to New York city in 2014, as one example, Airbnb increased the lodging supply by 17%[vi]! Nothing crimps a hoteliers’ buzz during Coachella more than a tsunami of pop-up rooms that saps their pricing power. In hotel-speak, the inability to raise prices diminishes a hotel’s “value capture.”

Airbnb is doing more than offering a “local, cultural, immersive experience,” for folks willing to sleep on some stranger’s floor in downtown San Francisco. The threat of entry and growth of Airbnb used to be directly felt by low-end hotels and traditional B&Bs because private room prices are generally on par with offerings of 1- and 2-star hotels. Hotels catering to business travelers and upper-scale hotels were less affected.

Not so anymore. In a bid to attract work-related travel, Airbnb is now actively collaborating with convention bureaus, conference hosts, and state governments. Airbnb has partnered with Delta Airlines, so airlines guests can earn miles by booking Airbnb properties through the airline’s website and piloted Airbnb Corporate Travel targeting business travel managers by offering properties with business amenities.

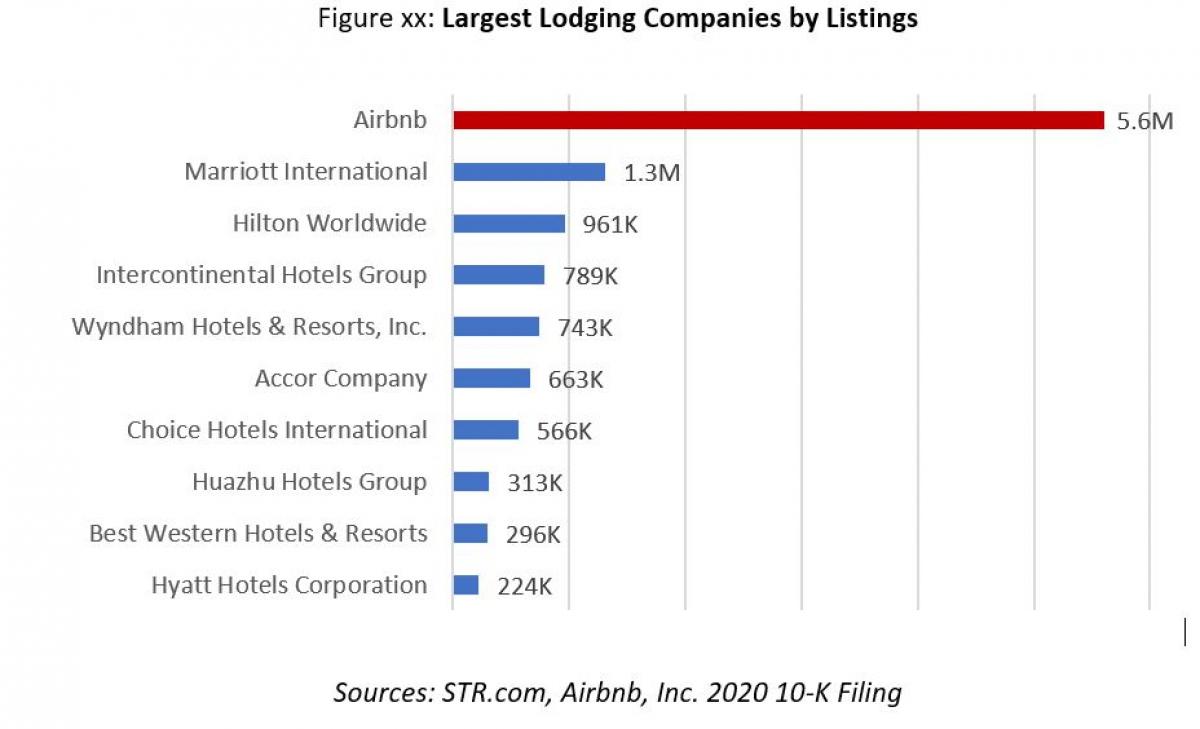

The next best thing to doubling, tripling, and even quadrupling room rates during the Super Bowl (or when an unprecedented weather event hits Texas) is gouging mid-week business travelers in tight supply markets. This has been a good steady business. However, today Airbnb has more room inventory than the largest hotel players, and it has been adding more luxury offerings on the platform.

Every time Airbnb’s supply doubles – which is its average yearly pace since inception – hotel revenues fall 2%[i].

Can Hotels “Disrupt” the Disruptor? Sure . . . But at What Price?

Airbnb’s—along with VRBO and a host of competitors’—secret sauce is the digital booking system, allowing consumers to easily compare a wide variety of options. Hotels looking to compete need to provide an equally impressive mobile-centric experience. All the fast-growing peer-to-peer lodging sites and online travel agencies allow guests to check-in without going to the front/reception desk. Some even sync with business expense apps.

Two-thirds of the services provided via Airbnb’s app do not relate to the booking itself but rather to the stay and experience of the guests who not only book a space but also concerts, cooking and fitness classes and other experiences[ii]. How hard is that? Hilton and Intercontinental are probably up to the challenge of coming up with audio walks and food scene recommendations. Harder to replicate is the fact that people want to book interesting and engaging places and most hotels offer generic spaces. Today, in addition to inflatable mattresses, Airbnb offers designer homes, private islands, and everything in between, including treehouses, castles, and boats.

Small urban units are Airbnb’s real game, and new models like Yotel, Moxy, and Tru Hotel are imitating the upstart by ditching the opulent lobbies and offering limited-service and minimalist micro rooms with less closet space and no desks. Some even offer dual and king-size bunk beds – something that was unthinkable in the hotel industry ten years ago. You want dense? You want affordable? This is where hotels can deliver—but the consistent ability to charge higher rates (getting that “value capture”) at times of significant demand might be challenged longer term.

[i] Marriott International, Statement on Marriott International’s COVID-19 Update to Associates, May 2020

[ii] Business Travel News, STR: 2020 Worst Year on Record for U.S. Hotels, Jan 2021

[iii] American Hotel & Lodging Association, AHLA’s State Of The Hotel Industry 2021

[iv] CoStar, Hotel Deals Pace To Pick Up After 2020 Volume ‘Fell off the Cliff’, Feb 2021

[v] Airbnb's effect on hotel sales growth, International Journal of Hospitality Management. Blal, I., Singal, M., & Tempal, J. (2018)

[vi] The Wall Street Journal, Airbnb Crimps Hotels’ Power on Pricing, Sep 2015

[vii] The Conversation, As Airbnb grows, this is exactly how much it’s bringing down hotel prices and occupancy, May 2019

[viii] Harvard Real Estate Review, A New Era of Lodging: Airbnb’s Impact on Hotels, Travelers, and Cities, Jan 2019

PRIVATE AND CONFIDENTIAL: These materials are strictly confidential and proprietary, intended solely for the use of the individual or entity to which Aksia LLC, and/or its affiliates, as applicable (collectively, “Aksia”) has sent these materials (“Intended Recipient”) and constitute Aksia’s trade secrets for all purposes, including for purposes of the Freedom of Information Act or any comparable law or regulation of any government, municipality or regulator. These materials may not be reproduced or distributed, posted electronically or incorporated into other documents in whole or in part except for the personal reference of the Intended Recipient. If you are not the Intended Recipient, you are hereby requested to notify Aksia and either destroy or return these documents to Aksia. The Intended Recipient shall not use Aksia’s name or logo or explicitly reference Aksia’s research and/or advisory services in the Intended Recipient’s materials.

NO OFFERING: These materials do not in any way constitute an offer or a solicitation of an offer to buy or sell funds, private investments or securities mentioned herein. These materials are provided only for use in conjunction with Aksia’s research and/or advisory services, as such services are defined in an executed agreement between Aksia and the Intended Recipient (hereinafter, the “Agreement”). In the event that an executed Agreement does not exist between Aksia and the Intended Recipient, these materials shall not constitute advice or an obligation to provide such services.

RECOMMENDATIONS: Any Aksia recommendation or opinion contained in these materials is a statement of opinion provided in good faith by Aksia and based upon information which Aksia reasonably believes to be true. Recommendations or opinions expressed in these materials reflect Aksia’s judgment as of the date shown, and are subject to change without notice. Actual results may differ materially from any forecasts discussed in the materials. Except as otherwise agreed between Aksia and the Intended Recipient, Aksia is under no future obligation to review, revise or update its recommendations or opinions.

NOT TAX, LEGAL OR REGULATORY ADVICE: An investor should consult its tax, legal and regulatory advisors before allocating to a private investment fund or other investment opportunity. Aksia is not providing due diligence or tax advice concerning the tax treatments of an investment or an investor’s allocations to such private investment fund or opportunity. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future.

RESPONSIBILITY FOR INVESTMENT DECISIONS: The Intended Recipient is responsible for performing his, her or its own reviews of any funds or other investment vehicles or opportunities described herein including, but not limited to, a thorough review and understanding of each vehicle’s or opportunity’s offering materials. The Intended Recipient is advised to consult his, her or its tax, legal and compliance professionals to assist in such reviews. For clients who receive only research services or non-discretionary advisory services from Aksia: the Intended Recipient acknowledges that he, she or it (and not Aksia) is responsible for his, her or its investment decisions with respect to any investment vehicles or opportunities described herein.

No assurances can be given that a particular investment or portfolio will meet its investment objectives. Any projections, forecasts or market outlooks provided herein should not be relied upon as events which will occur. Past performance is not indicative of future results. Use of advanced portfolio construction processes, risk management techniques and proprietary technology does not assure any level of performance or guarantee against loss of capital.

PERFORMANCE DATA: In cases where an investment manager or general partner implements an investment strategy through multiple investment vehicles (for tax purposes, participation in side pockets and new issues, domicile, currency denomination, etc.,) Aksia may use the returns of one class or series of an investment vehicle in a particular program in its reports to represent the returns of all the investment vehicles in such investment program. The returns for the particular class or series used in Aksia’s reports may be different from the returns of the class or series in which the Intended Recipient is invested. To obtain the actual performance of the particular class or series in the Intended Recipient’s portfolio, the Intended Recipient should contact the investment manager or general partner directly.

RELIANCE ON THIRD PARTY DATA: These materials reflect and rely upon information provided by fund managers and other third parties which Aksia reasonably believes to be accurate and reliable. Such information may be used by Aksia without independent verification of accuracy or completeness, and Aksia makes no representations as to its accuracy and completeness. For the avoidance of doubt, these materials have not been produced, reviewed, verified or approved by the fund managers and other third parties to which the materials relate. As such, they do not necessarily reflect the views or opinions of such fund managers and third parties. Furthermore, any reference to EBITDA (or ratios using EBITDA as a component) included in the report, reflect Adjusted EBITDA provided by the fund manager as defined in the loan agreements. Adjusted EBITDA may be higher than EBITDA figures calculated based on GAAP or IFRS compliant financial statements, which may result in relatively lower debt/EBITDA and higher interest coverage ratios.

RATING DOWNGRADES: Aksia client assets, in aggregate, may represent a large percentage of a manager’s or fund’s assets under management, and, as such, a rating downgrade by Aksia’s research teams could result in redemptions or withdrawals that may have an adverse effect on the performance of a fund.

CONFLICTS OF INTEREST DISCLOSURE: Family members of Aksia personnel may from time to time be employed by managers that Aksia recommends to its clients. While this may pose a potential conflict of interest, we monitor such relationships to seek to minimize any impact of such potential conflict.

PRIVATE INVESTMENT FUND DISCLOSURE: Investments in private investment funds and other similar investment opportunities involve a high degree of risk and you could lose all or substantially all of your investment. Any person or institution making such investments must fully understand and be willing to assume the risks involved. Some private investment funds and opportunities described herein may not be suitable for all investors. Such investments or investment vehicles may use leverage, hold significant illiquid positions, suspend redemptions indefinitely, provide no opportunity to redeem, modify investment strategy and documentation without notice, short sell securities, incur high fees and contain conflicts of interests. Such private investment funds or opportunities may also have limited operating history, lack transparency, manage concentrated portfolios, exhibit high volatility, depend on a concentrated group or individual for investment management or portfolio management and lack any regulatory oversight.

For a description of the risks associated with a specific private investment fund or investment opportunity, investors and prospective investors are strongly encouraged to review each private investment fund or opportunity’s offering materials which contain a more specific description of the risks associated with each investment. Offering materials may be obtained from the fund manager.

FOR RECIPIENTS OF REPORTS DISTRIBUTED BY AKSIA EUROPE LIMITED: Aksia Europe Limited is authorized and regulated by the Financial Conduct Authority; such authorization does not indicate endorsement or approval by the FCA of the services offered by Aksia.