By Sylvia Kwan, PHD, CAIA, CFA, Chief Investment Officer at Ellevest.

Imagine if … … you could invest to mitigate climate change. Or reduce global homelessness. Or finance the growth of women-owned businesses — all while diversifying your portfolio and earning financial returns.

Sounds too good to be true? Then keep reading.

When it comes to investing, there really is no free lunch — but using alternatives to achieve both financial returns and positive impact can come awfully close. If you’re a long-term investor, adding alternative investments to your portfolio can be a powerful way to reduce overall portfolio risk, enhance returns, generate income, and make a direct positive social and/or environmental impact. With US public equity markets near record highs and bond yields at historical lows, alternatives can offer opportunities for capital appreciation and income from sources outside of traditional markets.

What are alternatives?

Alternative investments are broadly defined as investments that are different from traditional assets like stocks, bonds, or cash. Today, alternatives span a very wide range of assets, including:

- Gold and precious metals

- Commodities like wheat and oil

- Real estate including buildings, land, farms, and forests

- Infrastructure such as bridges, toll roads, and renewable energy

- Art, wine, and coin collections

- Equity in a private company, including venture capital

- Debt of a private company

- Hedge funds

- Futures, options, and derivative trading strategies

- Cryptocurrencies

- Non-fungible tokens (“NFTs”)

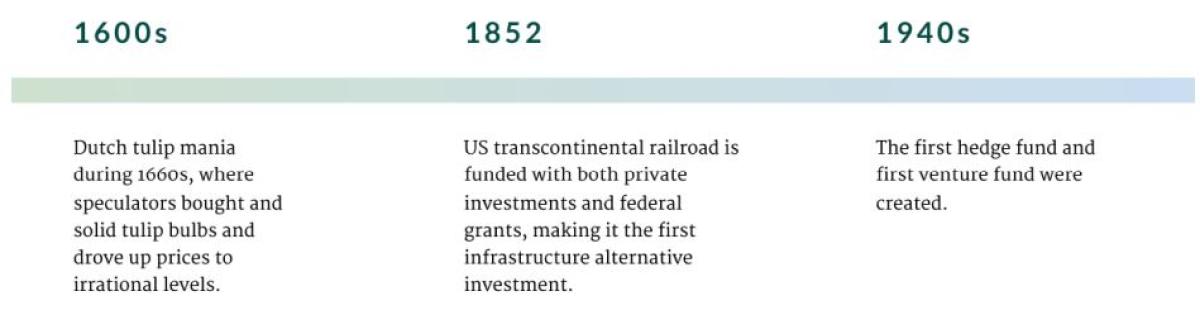

Investing in alternatives isn’t new. In the 1600s, speculators bought and sold tulip bulbs during the Dutch tulip mania, driving prices to irrational levels. The first infrastructure alternative investment, in 1852, was the US transcontinental railroad, which was funded with both federal grants and private investments. Individuals have been investing in land and real estate for centuries, and collecting baseball cards, coins, fine art, and rare wines for decades. The first hedge fund and first venture fund were created in the 1940s. And the most recent alternatives on the scene: cryptocurrencies, NFTs, and other digital assets.

Today, the lines are starting to blur between public and private investments; as a result, so have the criteria for what truly defines an alternative. An equity allocation may include both public and private investments, and a fixed income allocation may include both public and private debt. Any investments that fall outside these parameters would be considered an alternative investment. However, for the purposes of this paper, let’s stick to the current definition of alternatives: “investments that are not publicly traded stocks or bonds,” which includes all private investments.

What’s driving alternative investing?

Alternative investing has grown significantly over the last decade, with assets under management (AUM) rising from $4 trillion in 2010 to over $10 trillion in 2020, according to one report by Preqin. By 2025, AUM in alternatives are expected to grow to over $17 trillion.

This growth has been driven by several factors. Investors who were burned by the global financial crisis in 2008–09 have turned to alternative investments in search of returns that aren’t correlated with the stock market. (Correlation is a measurement of how two securities move in relation to each other. The lower the correlation, the less likely the two will react in the same way during an economic event or market cycle.) Alternative investments were also previously only available to large institutions like endowments and foundations, but innovation, technology, and the JOBS Act of 2012 have lowered many of the barriers that have kept individuals from investing in alternatives. In fact, some recent investing platforms offer alternatives at minimums as low as $10.

Today’s high US stock market valuations, coupled with low bond yields, have some investors questioning the sustainability of traditional investments to generate the returns they’ve enjoyed in the past. For decades, investors have been able to achieve successful outcomes with a portfolio comprising 60% equities and 40% bonds (commonly referred to as a 60/40 portfolio). Historically, equities and bonds have exhibited low correlation with each other. When stock prices go down, bond prices generally rise, remain stable, or at worst, decrease but less than stocks do. As a result, the 60/40 portfolio has historically provided the balance of risk and return that’s led to successful investment outcomes over the long term.

Looking forward, however, some investors are concerned with whether bonds will continue to provide downside protection if stocks decline, especially if the Federal Reserve increases interest rates. (Recall that when interest rates rise, bond prices fall.) Their fear is that stocks and bonds may fall at the same time, thereby fracturing the diversification benefits of the 60/40 portfolio that have been so dependable in the past.

We cannot predict whether equities will continue their rise or correct, taking bonds down with them. What we can do is position your portfolio with different types of investments that can perform, regardless of which scenario plays out.

How? By adding alternative investments.

Not all alternatives are created equal. The key to reducing investment risk in a portfolio is including those alternatives that have both low correlations to public stock and bond markets and differentiated risk and return characteristics designed to perform under varying market scenarios. At Ellevest, we intentionally seek alternative investments that are not dependent on how stocks or bonds perform, how the economy is faring, or whether interest rates or inflation are rising or falling. Instead, we seek alternative investments with returns driven by other sources, such as supply and demand imbalances that we believe will persist, whatever the health of the overall economy might be.

Why invest in alternatives?

Adding alternatives to a portfolio has several important benefits:

- They can decrease overall portfolio risk through diversifying characteristics

- They can enhance portfolio performance by adding sources of returns that are differentiated from those of stocks or bonds

- They can generate income

- In the case of impact alternatives, they can even drive direct positive social and environmental impact

Private alternatives can also give fund managers the opportunity to play a more active role in their portfolio companies. Managers of private debt and equity strategies invest in significantly fewer companies than managers of publicly traded funds, which can own hundreds, sometimes thousands, of companies. They also generally have deeper relationships with the companies’ management teams and a greater understanding of their businesses, which allows them to actively monitor and manage these investments. Also, in times of economic stress, or if companies are experiencing particular challenges, private fund managers have the flexibility to work with companies to address them. This can include seeking or supplying additional financing, providing specific business or operational expertise, assisting with restructuring or capital market transactions, and/or extending or modifying deal terms. It’s also common for managers to have an active or observer board seat. This kind of hands-on management is an advantage of private funds that can help mitigate risk.

Alternative investments can also enhance portfolio returns by providing access to investment strategies that aren’t available in public markets. Large endowments and foundations have used private alternatives for decades, and many have significant allocations to these types of investments. 2020–21 was a banner year for a number of large college endowments, with some earning returns of 50% or more. The driving force? High allocations to alternative investments.

Drawbacks and risks of alternative investing

Although alternatives have significant potential benefits for long-term investors, they do also come with higher fees, unique risks, and in many cases, long hold times. Most alternatives are illiquid, meaning they can’t be bought or sold, or exchanged for cash, easily or quickly. Such private investments are not traded on a public exchange like the New York Stock Exchange or NASDAQ, and they aren’t subject to registration or oversight by the Securities Exchange Commission (SEC).

Long hold times

Illiquidity and long hold times are often seen as disadvantages in alternative investing. Yet while not being able to sell at your preferred timing is a risk, illiquidity can also be a benefit for long-term investors. First, an investment that cannot be bought and sold from day to day isn’t as susceptible to fluctuations caused by irrational (or even rational) investor behavior. The fund manager can focus on executing on the investment strategy instead of worrying about having to sell assets at suboptimal times to satisfy redemptions. Second, even professional investors are known to sell at the most inopportune times. The inability to make those blunders — especially those in reaction to headlines, fear, and emotions — can help investors stay the course over the long run. (Of course, any funds needed over the near term should not be invested in an illiquid investment, regardless of its attractiveness.)

But not all alternative investment strategies are illiquid; some strategies, like long-short investing or global macro, are offered in the form of public mutual funds and ETFs. Because these funds are publicly traded, they’re also subject to the herd behavior of investors. They’ve historically exhibited high correlations with the equity markets, which can dampen the diversification benefits of using alternatives in the first place. While publicly traded alternative funds do have a place in portfolios that can’t access private alternatives, they still can’t offer the range of diversification, income, and impact that make private alternatives such a powerful addition to investment portfolios.

Fees

Management fees for alternatives typically range between 1.5% to 2.5% annually, plus a performance fee that could be 20% of any profits above a specific return threshold (often called a hurdle rate or preferred rate). While these fees are common across most alternatives, they’re high relative to an indexed-based equity mutual fund, which can have fees of 0.05% or lower and no performance fees. It’s in part because alternative strategies are generally more costly to implement and manage. It’s important to take these higher fees into account when evaluating the target returns of alternatives, and to understand the potential source(s) and sustainability of those returns, and how well the managers have executed against strategy to achieve those returns.

Other risks

Many private funds hold far fewer investments than publicly traded funds. Fewer underlying companies — particularly if they’re focused in one or two industries or geographies — can expose investors to concentration risk. That means that, if the specific industry experiences a downturn or challenge, the private fund could be negatively impacted compared with a fund that’s well diversified across many different industries and sectors.

The success of private investing relies heavily on the skills and execution abilities of the fund manager. The loss of a key investment professional, or the lack of robust investment decision-making or operational processes, can negatively impact the performance of the fund. Contrast this with a publicly traded index fund, where investment decisions are made using a set of rules and algorithms with little (if any) human intervention or judgment.

In considering alternatives, investors should be mindful of each strategy’s unique risks and understand how private fund managers manage and mitigate them through robust processes, specialized expertise, and active oversight.

The importance of due diligence

Because of the unique risks of alternatives and the wide range of different alternatives strategies, one must have a robust due diligence process for evaluating an alternative investment’s suitability and potential. At Ellevest, sometimes over a period of several months, we conduct three levels of due diligence: investment, operations, and data security.

Investment due diligence involves assessing the investment strategy, opportunity, competitive advantages, implementation, and decision-making process. Specifically, we seek managers that demonstrate:

- A differentiated investment strategy with sustainable competitive advantages that are implemented using a disciplined, repeatable investment process. The strategy should also demonstrate low correlation between asset classes in the portfolio to reduce overall portfolio risk.

- A strong track record of investment performance, disciplined execution against strategy, and active risk management processes.

- A high degree of specialization, experience, and expertise; transparency in both their investment process and investor communications; and demonstrated alignment with investors’ interests.

For operational due diligence, we evaluate the strength and adequacy of the managing firm’s trade operations and controls, human capital, cash management, internal valuation procedures, compliance program, and financial reporting and legal processes.

Lastly, for data security due diligence, we assess the security of client data as it flows from the managing firm to Ellevest and vice versa, and the adequacy of the firm's data security and privacy policies.

An alternative investment must meet our investment, operations, and data security criteria before we recommend it in client portfolios.

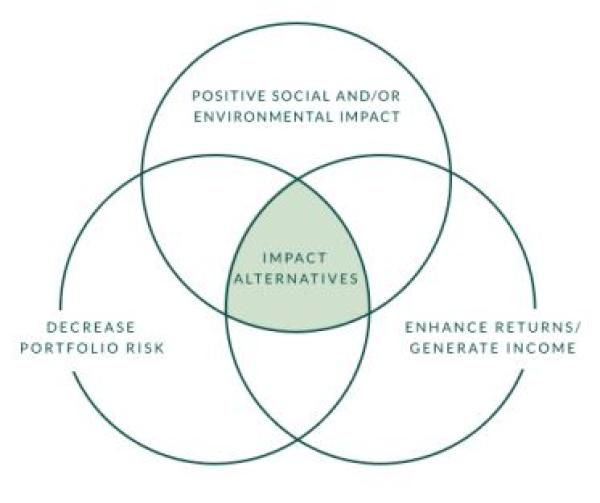

Impact alternatives: The potential for double (and even triple) bottom lines

As mentioned, alternative investments can reduce risk and enhance returns, both of which help with long-term portfolio success. But the case for adding alternatives is even greater for impact investors. In fact, they make impact investing — investing to drive direct measurable positive social and environmental impact — more possible than ever.

Any investment, regardless of its potential for impact, must meet our fiduciary standards and investment criteria. If they do, only then do we consider its impact. But using capital to address some of the world’s largest societal and environmental issues — all while earning financial returns — has the potential to create two bottom lines: financial and impact performance. But it doesn’t end there: In some cases, we’ve found alternative investments that aim to close more than one social or environmental gap, creating a potential third bottom line.

Some of today’s most challenging socioeconomic and environmental issues, from homelessness to climate change to racial and gender equality, cannot be solved by government intervention alone. To make meaningful progress, we must catalyze both public and private capital. And today, there are more opportunities than ever for private capital to address these issues through investing — in the form of impact alternatives.

Investing for financial returns and positive impact is one of the most powerful and rewarding ways to invest, and we couldn’t be more excited to be helping our clients to get involved with this type of investing.

The following examples are illustrations of how we use alternatives to help our clients invest with impact.

Renewable energy

The demand for renewable energy — electricity produced by wind, solar, and hydro power — continues to grow, driven by consumer demand, regulation and incentives from governments and municipalities, and efforts from corporations to reduce their carbon footprint. Over the past decade, the cost of solar panels has dropped significantly, making renewable power very price-competitive with traditional energy sources. Solar has grown from less than 1% of the world’s electric-power capacity to an estimated 9%. By 2040, the International Energy Agency expects solar to be our largest single energy source.

Compared with stocks, operational renewable energy assets can be low-risk, stable-yield investments. While this asset class isn’t expected to produce equity-like annual returns, it also isn’t likely to be buffeted by market volatility. It generates power using natural resources that are readily available — sun, wind, water — so disruptions to supply chains are unlikely, even in a global pandemic. Plus, the demand for electricity that these energy assets produce is an essential service that isn’t expected to ebb and flow with the equity markets. Its very low correlation with equity markets makes it a risk-reducing addition to traditional stock and bond portfolios. These assets also provide a steady source of income at significantly higher yields than fixed income.

Another approach, albeit one with a higher risk-and-return profile, is to invest in renewable energy development projects, both in the US and abroad. Just like with real estate development projects, renewable energy development projects are capital- and time-intensive — they don’t typically generate income until they’re operating and producing electricity. Renewable projects in developing countries, such as those in sub-Saharan Africa, can create a positive impact both socially and environmentally by bringing power to towns and villages that didn’t have electricity before.

Sustainable Agriculture

Climate change caused by increased carbon emissions has taken center stage around the world, and alternative managers have been actively seeking solutions and different approaches to address these issues. Some funds acquire and manage natural forests and lands both in the US and abroad to improve their environmental value through sustainable timber harvesting, water conservation, and the restoration and protection of natural ecosystems and biodiversity. Such funds can generate economic value not only from the sale of timber but through conservation easements and the sale of carbon credits as well.

Other funds may invest to preserve water quality and supply, or transition traditional farming to regenerative farming, the latter of which can significantly reduce agriculture’s environmental footprint and naturally sequester carbon emissions.

Affordable and workforce housing

The US is currently facing a shortage of affordable housing, which will likely worsen as the national homelessness crisis grows. At the same time, the supply continues to shrink, as fewer affordable housing developments are built, and as homes originally designated as affordable get acquired, renovated, and converted into market-rate homes.

This supply and demand imbalance will continue to widen, regardless of how the economy is faring, or whether stocks rise or fall. In fact, recessions and market downturns — and most recently the coronavirus pandemic — tend to exacerbate the demand for affordable housing even further. Studies show that, historically, affordable housing has performed well during recessions because its returns are driven by increasing demand and declining supply, not by the volatility of stocks or bonds. This means its financial performance will likely have a very low correlation with the performance of stocks. So as long as demand continues to outstrip supply, affordable and workforce housing is likely to perform through strong and weak markets. (Real estate investments have also historically offered a hedge against inflation.)

Capital invested in these assets directly benefits low- to moderate-income residents by providing housing they can afford. One real estate fund manager with whom we partner at Ellevest also focuses on environmentally friendly renovations to each property, like the installation of energy-efficient washers and dryers, better insulation, solar panels to heat swimming pools and common areas, and low-water landscaping. An investment like that has a potential triple bottom line: financial return to investors, positive social impact (for residents) and positive environmental impact (planet-friendly enhancements that help reduce energy and water usage).

Private equity describes a wide range of companies and strategies — from venture capital to growth financing to buyouts and mergers and acquisitions. The primary objective of private equity financing is to increase the value of a company and sell it for a profit. Many private equity firms (excluding venture capital) seek to acquire distressed or stagnant companies that present opportunities for the firm to increase efficiencies, or repackage or restructure them in an effort to improve profitability, with the end goal being to sell them or take them public. Sometimes these firms are successful, and the companies are stronger as a result; other times, they can drive the companies to bankruptcy, costing many hundreds of jobs. While private equity has developed a poor reputation — short-term profit-seeking at the expense of jobs and long-term value creation has led to a number of high-profile bankruptcies in recent years — it can also create meaningful, positive impact.

At Ellevest, we choose to work with private equity managers who seek returns by helping companies achieve their financial goals and create a positive impact on their employees, communities, and the planet. We’ve found that managers who set an intention for impact alongside returns tend to share our values and commitment to making the world a better place.

Venture capital offers many opportunities to invest for both positive impact and financial returns. Today, many venture funds provide seed-stage financing exclusively to start-ups led by women, people of color, and other underrepresented entrepreneurs. In 2020, only 2.4% of venture capital dollars went to supporting women-founded teams, leaving both a huge financing gap as well as underappreciated investment opportunities.

Some venture capital managers invest in underrepresented founders with start-ups building solutions and technologies that address environmental and socioeconomic problems — for example, a company founded by women that designs and manufactures personal shelters to address homelessness, or a women-founded company that developed a technology platform for farmers to sell imperfect produce to reduce food waste (ie, one of the largest contributors to carbon emissions). These types of companies, and the funds that invest in them, have the potential to generate multiple levels of positive impact while also seeking venture capital financial returns.

But what about hedge funds?

Hedge funds are alternative investments that attempt to generate returns whether markets are up or down, employing various strategies intended to protect and hedge against downside scenarios. Most, however, implement these strategies by buying and shorting publicly traded companies, and by using derivatives and nontraditional techniques for hedging. But these strategies have historically yielded mixed results. Our perspective is that most hedge funds — due to the nature of their strategies and investment activities — don’t diversify traditional equity markets nearly as well as other types of alternatives. And some hedge fund strategies even amplify equity market risks, which defeats the purpose of adding diversifying alternatives to a portfolio.

Moreover, most hedge funds follow pure investment strategies with little, if any, regard for positive impact. And in general, it’s more difficult to invest with a direct positive impact with publicly traded securities. Because hedge funds lack the diversifying and impact properties we seek in alternatives, we do not recommend hedge funds for our clients’ portfolios.

Private Debt

Private global debt markets offer investors unique opportunities to earn enhanced yields compared to those offered in public, liquid markets. Loans to US-based small- and medium-sized businesses seeking growth capital have historically generated higher yields than public corporate debt. An example of private debt is a fund that provides revenue-based loans to mid-sized private companies in the US. Returns are tied to a percentage of the company’s revenues, instead of at a fixed interest rate. Because the debt repayment is tied to a contractual agreement, such debt has low sensitivity to the direction of interest rates; plus, investors can earn additional upside if the borrowing company performs well or gets acquired.

This strategy has many of the investment characteristics we seek, but we wanted to offer an opportunity like this with an even greater impact. So a fund manager we work with created a private offering that provides capital exclusively to businesses owned and led by women, people of color, and those who identify as LGBTQIA+. These underrepresented business owners have traditionally had greater challenges finding growth capital, and this strategy aims to help close that gap.

To take another example, trade finance and growth-stage loans to profitable small- and medium-sized enterprises in emerging economies offer investors a way to invest in emerging markets without the volatility associated with emerging market equity. These loans also provide capital critical to growing firms in countries experiencing financial dislocation. A fund manager in this space adds additional impact by selecting borrowers that meet specific environmental, social, and governance (ESG) standards and commit to goals to increase its positive impact in one or more of those areas. Another example of an impact private debt strategy involves providing micro-loans to low-income households in emerging countries.

These micro-loans have had low default rates, and they have exhibited low, if any, correlation with US public markets. One strategy specifically provides micro-loans for obtaining clean water and sanitation. Such a strategy positively impacts millions of low-income families, primarily women, who bear the responsibility of obtaining clean water and often spend the better part of each day doing so.

These types of alternative investment strategies — private revenue-based loans in the US, private debt and micro-loans in emerging countries — have unique risk-and-return characteristics that distinguish them from traditional strategies in public equity and debt markets. They diversify portfolio risk while providing the opportunity for enhanced yields and income. And while illiquid, their high yields relative to current US bond yields, combined with low correlations to both US equity and fixed-income markets, make them a compelling investment in well-diversified portfolios.

Conclusion

For those seeking to positively impact their portfolio and the world, alternatives can be one of the most powerful and meaningful ways to invest. No one can predict what will happen in the future, and as stewards of our clients’ assets, we actively seek investment solutions that we believe can perform through all kinds of markets. We believe that alternatives, through their diversifying properties and unique risk and return characteristics, can play a significant role in achieving long-term investing success. Many of the alternatives that meet this and other investment criteria also have the kinds of social and environmental impact our clients seek.

But we don’t want to stop there.

Rather than wait for the industry to create the kinds of alternative investments with the impact we want, we continue to proactively seek opportunities with alternative fund managers.

to co-create investment strategies that leverage the expertise of these managers and apply the impact lens our clients tell us they care about. Together, we can use the power of private capital to create change in our communities and in the world.

Original Article: Impact Alternatives: Seeking Double (or Triple) Bottom Lines (ellevest.com)

About the Author:

Dr. Sylvia Kwan, Ph.D., CFA, CAIA Sylvia is the Chief Investment Officer at Ellevest, a technology-enabled financial services company built by women, for women. In this role, she is responsible for creating the investment solutions, strategies, portfolios, and proprietary algorithms that drive Ellevest’s investment recommendations across both automated digital and customized private wealth advisory services. She guides the firm’s investment philosophy and leads the development and due diligence of Ellevest’s impact and gender forward investments. Prior to joining Ellevest, Sylvia was a founding member of the investments team at Financial Engines, L.L.C. one of the first successful digital advisors.

During her tenure, she developed scalable, robust investment processes to manage over $14B in AUM for over 200,000+ client accounts. In 2010, Sylvia co-founded the boutique RIA firm SimplySmart Asset Management, serving individual investors with fully customized global investment solutions. Her financial services experience also includes portfolio management positions at Charles Schwab Investment Management, where she was director of equity quantitative research, and at the Boston Company, where she managed over $500 million in institutional fixed-income assets. Sylvia is a Director of Exit 182 Group, LLC where she shares responsibility for the fiduciary oversight of Grinnell College’s $3B endowment. She recently joined the Board of Lotus Campaign, a startup non-profit focused on housing-driven solutions to homelessness. Sylvia holds both Chartered Financial Analyst® and Chartered Alternative Investment Analyst® designations. She earned a B.S. in applied mathematics and computer science from Brown University and a Ph.D. in engineering-economic systems from Stanford University. Her doctoral dissertation on investor behavior and social interaction was one of the first in the field of behavioral finance.

Disclosures Last updated January 2022 | © 2022 Ellevest, Inc. All Rights Reserved. Investopedia (“Solicitor”) serves as a solicitor for Ellevest , Inc. (“Ellevest”). Solicitor will receive compensation for referring you to Ellevest. Solicitor will be paid $10 when an individual activates a membership. You will not be charged any fee or incur any additional costs for being referred to Ellevest by the Solicitor. The Solicitor may promote and/or may advertise Ellevest’s investment adviser services. Ellevest and the Solicitor are not under common ownership or otherwise related entities. Information was obtained from third-party sources, which we believe to be reliable but not guaranteed for accuracy or completeness. The information provided should not be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation or particular needs of any specific person. Diversification does not ensure a profit or protect against a loss in a declining market. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Investing entails risk including the possible loss of principal and there is no assurance that the investment will provide positive performance over any period of time