By David Moreno, CFA, Indexes Manager, Research & Indexes team, EPRA.

Inflation is in the eye of the storm for the majority of analysts, strategists and investors analysing expected returns and assessing strategic asset allocations for 2022. Inflation plays a key role in the real estate industry, impacting lease contracts, maintenance costs, development expenses and property valuations among others. Property companies face changes on both operational revenues and expenses when inflation rises, therefore it is necessary to have a closer look at the way these variables interact, in order to understand the final effect on listed real estate companies.

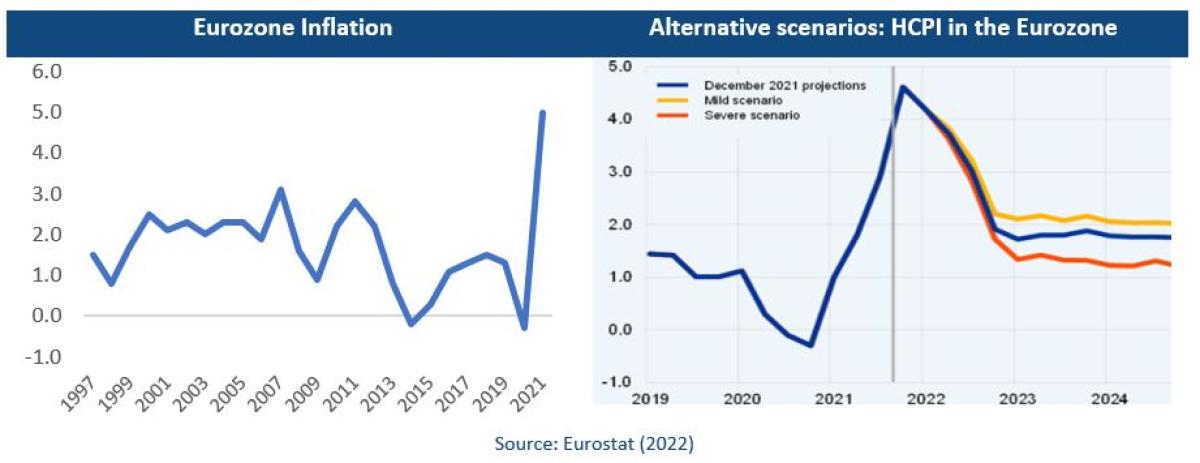

Since the beginning of 2021, inflation measured by the Consumer Price Index (CPI) has increased globally, both in advanced and emerging countries, driven by supply disruptions coupled with recovering demand, as well as rising commodity and housing prices (IMF, 2021). In the Eurozone, inflation reached a record level (5.1%) in January 2022, after years of low inflation. Similar trends have been observed in Sweden, Switzerland and the UK. This can be explained by three main reasons: A quick reopening of the economy, higher energy prices and base effects (ECB, 2021). The ECB expects the inflation to gradually decrease in 2022, while the Bank of England sees inflation peaking at 7.25% around April 2022 before gradually decreasing during the rest of the year. A similar view is shared by the central banks in Sweden and Switzerland.

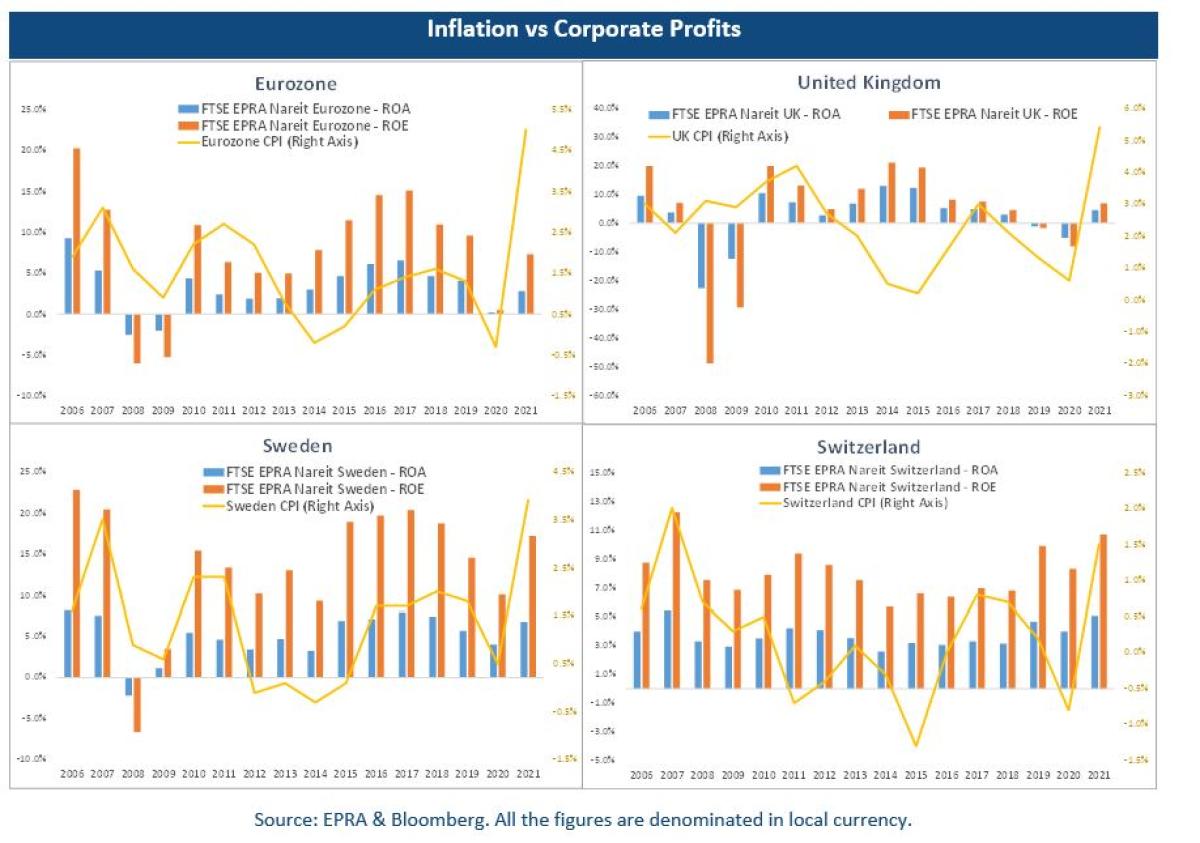

Property companies know how to react to changes in inflation. Rental practices in Europe facilitate the integration of inflation dynamics into the companies’ revenues and support rental growth. As a general market practice in Europe, rental escalation is based on CPI-linked indexation, so it reflects an automatic CPI adjustment. Other lease agreements have an annual CPI-linked indexation or 5-year rental review – mostly for the UK, where leases are subject to market review to evaluate between inflation-adjusted rents and actual market rent growth. However, higher inflation also means higher maintenance expenses, development costs and property acquisitions. So, what is the final effect of inflation on net profits and shareholders returns? EPRA has found evidence of a strong and positive correlation between corporate profits and inflation as well as shareholders’ returns and inflation.

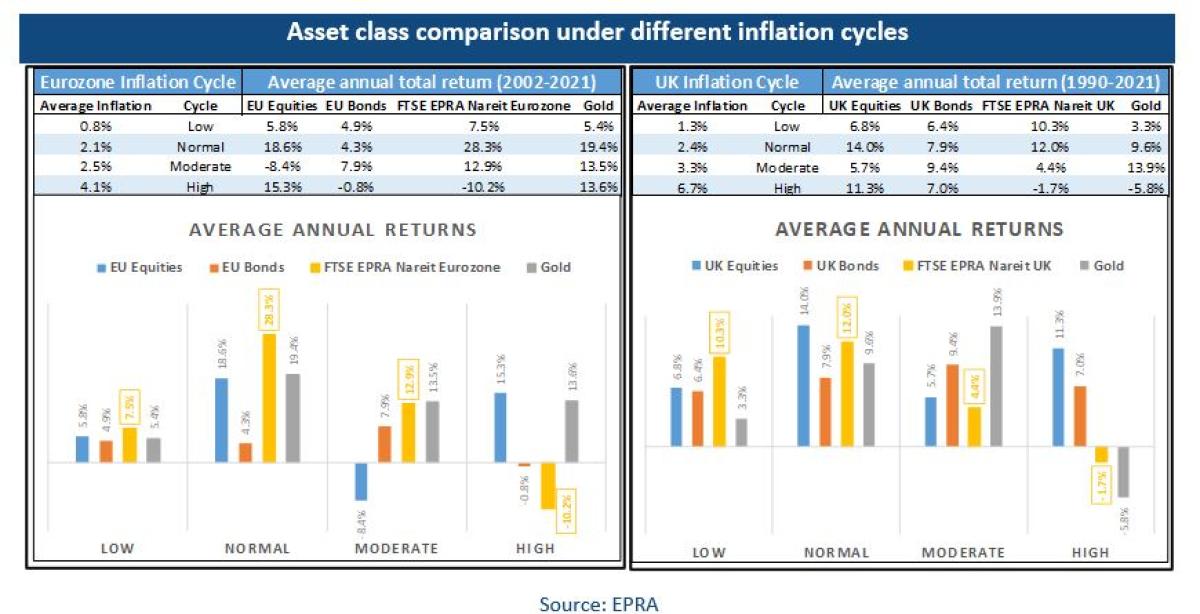

During the last 20 years, listed real estate in the Eurozone always outperformed general equity and bonds under low, normal and moderate inflation cycles. A similar case is observed in the UK for the period 1990-2021, showing a higher or similar return than general equities under the same cycles. However, under high inflation cycles (above 3.06% for the Eurozone and 5.04% for the UK[1]) listed real estate underperformed general equity and bonds, which is mainly the result of a combination of strong economic growth and low returns in real estate in anticipation of an economic contraction, such as the case of 1990-1991 in the UK and 2007 both in the Eurozone and the UK.

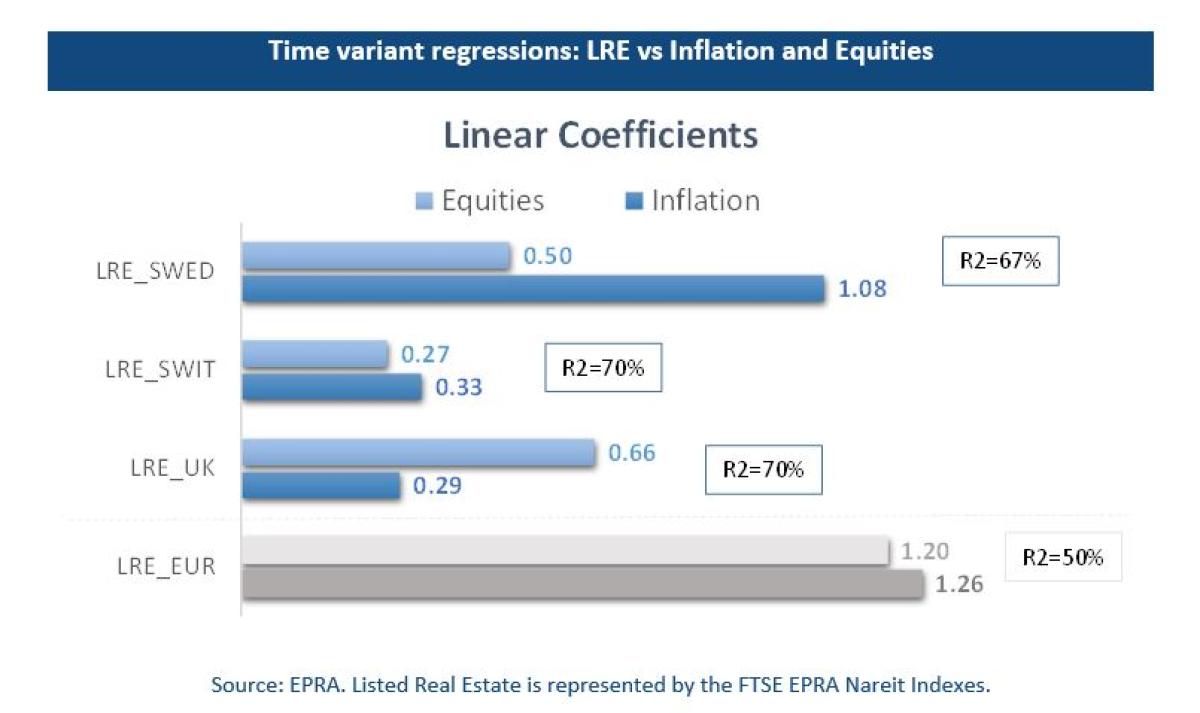

Using a time variant econometric model[1] for analysing the impact of inflation on listed real estate total returns and including general equity returns as a control variable, EPRA estimates that a 100 bps increase in the annual inflation has a positive effect of 33 bps in the annual total return from listed real estate in Switzerland, 29 bps in the UK and 108 in Sweden, reflecting a substantial efficiency of listed property companies to react to changes in inflation. In the case of the Eurozone, given the limited history of the currency with very few moderate high inflation cycles, the significant number of countries and drivers involved, as well as the diversity of property sectors, our model seems to be less precise and provides some coefficients that might be biased, therefore it is worth to look into country-specific models to have a more accurate estimation.

After a deep recession in 2020, last year was characterised by a clear economic recovery, forecasted by many analysts and institutions to continue on a more moderate path in 2022 and 2023. Current inflation levels are not associated with strong demand pressures but with several temporary supply disruptions. Therefore, following the market’s and central banks’ expectations, we are likely going to see a moderate inflation cycle in Europe in 2022 and 2023 that should represent a positive driver for corporate profits and returns of the listed real estate industry across the continent.

Check EPRA’s full report on inflation here: https://www.epra.com/research/market-research

[1] ARIMAX model in 1st differences with LRE returns as dependant variable and Equities and Inflation as independent variables.

[2] Moderate and High cycles are defined by the 70th and 90th percentiles respectively, 2.2% and 3.05% for the Eurozone, 2.91% and 5.04% for the UK.

About the Author:

David Moreno is Indexes Manager at the European Public Real Estate Association. For almost six years now, his work at EPRA has been focused on analysing the main drivers and evolution of the listed Real Estate markets in Europe and the management of the FTSE EPRA Nareit Global Real Estate Index series. He also has more than five years of experience as fixed income strategist and corporate finance analyst for financial institutions and corporates.

David holds degree in Finance and Economics from Universidad del Rosario (Colombia) and a joint Master degree in Quantitative Economics and Financial Engineering from Université Paris I Pantheón-Sorbonne (France) and Universitá Ca’Foscari di Venezia (Italy). Finally, he is also a CFA charter holder and cooperates actively in several CAIA events and research projects.

Linkedin: linkedin.com/in/david-moreno-cfa-8647b16a

E-Mail: d.moreno@epra.com