By Matthew Hoehn, Co-Head of Custom Asset Allocation at TIFF Investment Management.

INTRODUCTION

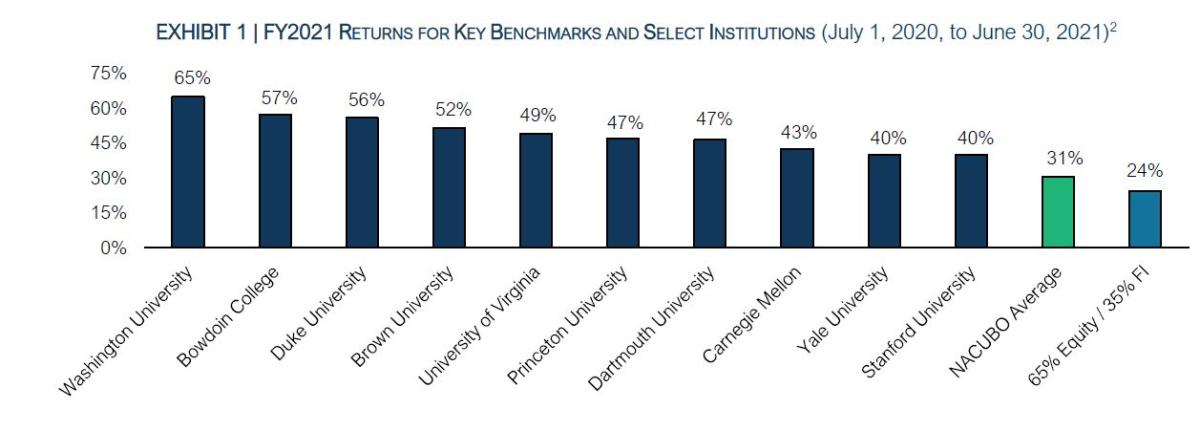

Each year, the nonprofit investing world eagerly awaits fiscal year (“FY”) investment results from US college and university endowments. As Exhibit 1 shows, FY2021 was particularly noteworthy for the strength of the overall returns and for the magnitude of returns from a handful of institutions. The FY2021 NACUBO-TIAA Study of Endowments aggregate return of 30.6% is the highest on record since 1991.1 Longtime standouts Bowdoin College and Duke University reported eye-popping figures of 57% and 56%, respectively. Less well-tracked investment offices at Washington University in St. Louis and Carnegie Mellon clocked in with similarly impressive results.

Unsurprisingly, this performance has attracted considerable attention. Given our 30+ years of experience at TIFF managing nonprofit portfolios, we wanted to share three observations on this year’s results. First, these returns were extremely strong, in part, because Equities and other risky assets posted equally outsized returns during FY2021. The returns were impressive by any measure, but the context of a meaningful equity tailwind certainly matters. Second, the atypical returns that markets delivered in FY2021 – high even in this current bull market – are unlikely to be sustained going forward. Below we will give some perspective on why we believe this to be the case. Third, we do believe that excess returns above market indices are achievable over the long-term. Indeed, many of the organizations with strong FY2021 results have a long history of outperformance. The same foundational investing principles that appear to underly these strong results have, we believe, contributed to our own long-term outperformance.

CONTEXT IS IMPORTANT

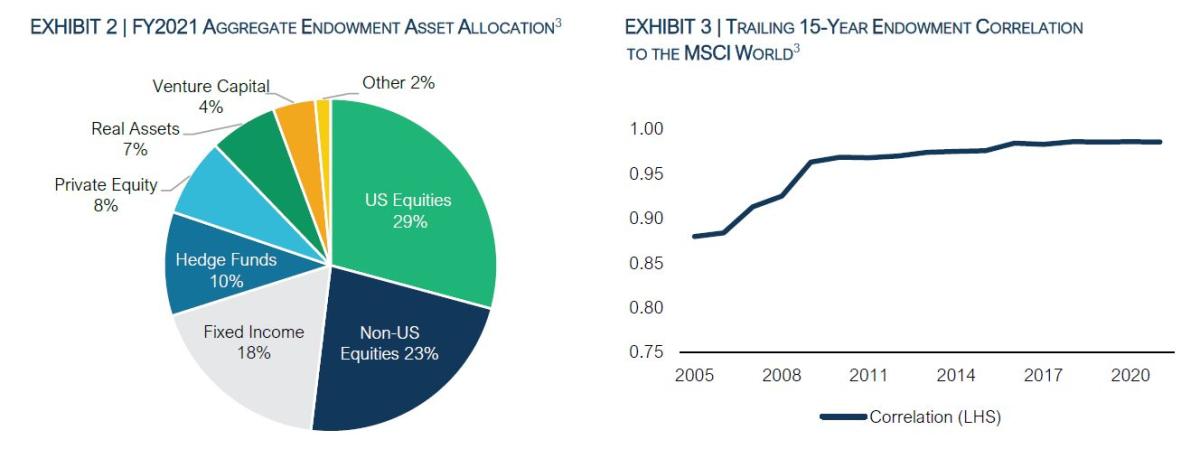

Exhibit 2 shows the latest available aggregate asset allocation for endowments. Less than 52% is invested in Public Equities, and such alternative asset classes as Private Equity, Venture Capital, Hedge Funds, and Real Assets are materially represented. Despite this, Exhibit 3 shows that endowment returns have moved nearly in lockstep with equity markets, with a trailing 15-year correlation of 0.99 since 2018. The take-away is that endowment portfolios that initially may appear highly diversified and insensitive to the gyrations of the market are in fact quite highly exposed to it. The reason, we believe, is that the returns of such asset classes as Private Equity, Hedge Funds, Venture Capital, and Real Assets, are largely driven by the very same factors that drive Public Equity returns.

Given this extremely high correlation, one would expect endowment performance to track the equity market quite closely; that is in fact what we saw in FY2021. Following the initial COVID-19 shutdown of the US economy in March 2020 and the subsequent market sell-off, policy makers responded with unprecedented amounts of both fiscal and monetary support over the course of March and April 2020. After its trough on March 23, 2020, the MSCI World Index quickly recovered its losses and then proceeded to return an extraordinary 39% over the course of FY2021. Private Equity, Hedge Funds, and Venture Capital, buoyed by this same policy support, posted similarly historic gains of 55%, 28%, and 82%, respectively.4

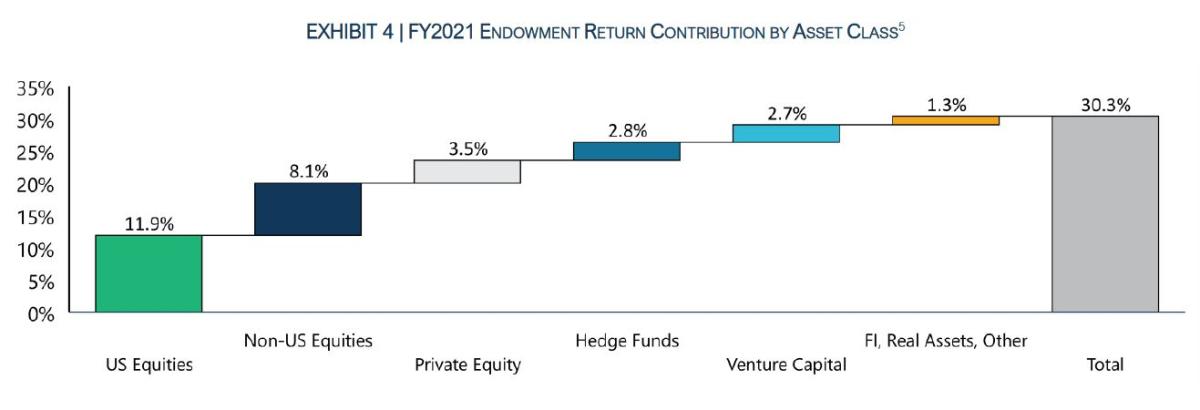

We will conclude this section by giving an indication of which asset classes contributed most significantly to the outsized 30.6% aggregate endowment return. Exhibit 4 below simply takes the asset class weights from Exhibit 2 above and applies the most appropriate index return to obtain a contribution for each asset class. As we have discussed in this section, Public Equities were certainly a key driver, but Private Equity, Hedge Funds, and Venture Capital, highly influenced by equity markets broadly, also contributed meaningfully. With the context and underlying drivers established, let us move on to discuss whether these types of returns can be continued in the future.

SUSTAINABILITY OF MARKET RETURNS

Equity bull markets can endure for longer than expected – and sometimes for longer than can be justified by fundamentals. And to be sure, there are reasonable arguments to be made as to why Equities – despite a challenging start in 2022 – will continue their ascent, namely:

- Economic Outlook – Equity markets typically do not decline for protracted periods outside of economic recessions. The risk of a recession has certainly risen in the recent past, but we still do not regard a recession as our base case scenario. That said, we do acknowledge the difficult task that the Federal Reserve and other central banks have: i.e., to dampen inflation without inducing a labor market slowdown and decline in economic growth

- Modestly Higher Interest Rates – Our base case is for rates to increase from here in a moderate and orderly fashion. This would likely induce investors to continue funding equity markets at roughly the valuation levels of the recent past

- Margins and Earnings – Economy-wide productivity increases and healthy consumer balance sheets may offset rising labor and financing costs, keeping corporate performance strong

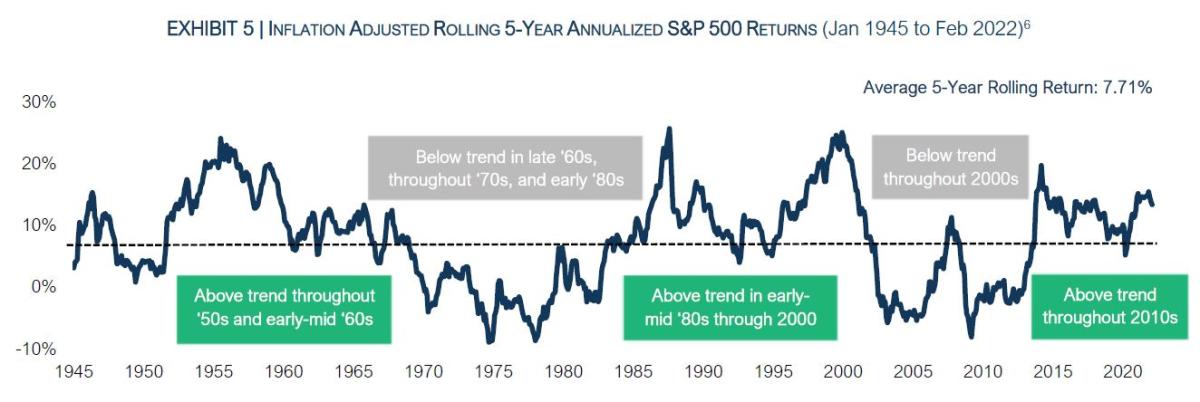

The long-term history of inflation-adjusted Equity returns, however, reveals a less-optimistic outlook. As Exhibit 5 illustrates, trailing 5-year real returns on Equities have been above their long-term trend for some time now. While each economic and market cycle is unique, it is noteworthy that, when returns are sustained above trend for years at a time, they will typically revert to a below-trend level.

There appear to be clear catalysts for a move toward secularly lower equity returns in the coming years. For instance:

- Fiscal policy – Stimulative fiscal policy was a massive tailwind for the economy and markets in the latter part of 2020 and throughout 2021, but could become a meaningful drag in 2022 and 2023

- Risk of Meaningfully Higher Rates – Although our base case is moderate increases, we cannot rule out something more pernicious as the Fed embarks on its tightening campaign to reduce inflation. Higher rates, of course, can become a headwind for equity prices

- Valuations – While there are a variety of reasons for secularly higher valuations in recent decades (e.g., the sectoral composition of the equity market, low and stable inflation, and the resulting lower interest rate environment), it is certainly noteworthy that the Cyclically Adjusted Price to Earnings Ratio (“CAPE”) stood at 37.5 as of December 31, 2021, the 95th percentile in the time period dating back to 1980. There is a lingering risk that investors, at some point, will grow weary of continually supporting these valuation levels

- Russia/Ukraine risks – In our view, the media and other commentators often overstate the impact of geopolitics on financial markets. That said, the war certainly risks tipping Europe into recession, will likely contribute to continued elevated commodity prices, and may have triggered an emerging “Cold War 2.0,” with the US and European coalition on one side and Russia, and potentially China, on the other. All of these developments represent downside risks to economies and equity prices

Turning briefly to Fixed Income markets, the outlook has improved in the recent past, but is still fundamentally unattractive: 10-year US Treasury yields are at 2.85% as of this writing, a 71 basis point move upward over the past month and a 128 basis point move over the past year. Although we do expect inflation to move down toward its target over the coming quarters, it could certainly persist in the system for longer and continue to make US Treasuries a steeply negative real return proposition. Further, credit spreads are still tight by historical standards, representing fairly modest compensation for the risk of default. Last, the Federal Reserve has just started a tightening cycle, which is likely to be a negative for bond investments.

In summary, when we look across the Equity and Fixed Income markets, we do foresee positive real returns for endowments in the coming quarters and years. However, we think the elevated return environment of recent years is less likely to persist.

PERSISTENCE OF EXCESS RETURNS

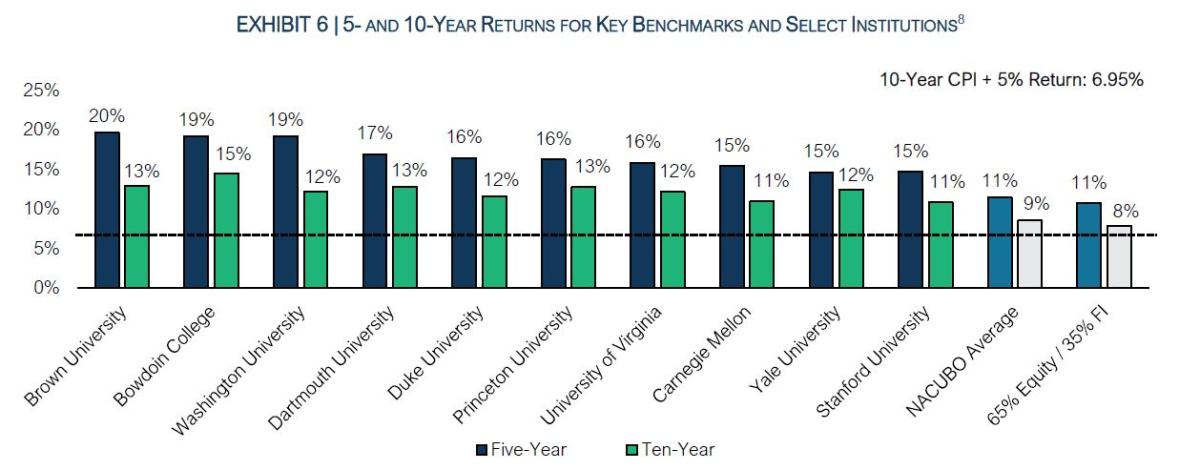

Although we expect muted returns from Fixed Income and lower returns from Public Equity going forward, outperforming indices can help to offset this likely reduction. Exhibit 6 shows that many of the institutions highlighted above have successfully outpaced the NACUBO average, a 65/35 Mix, and CPI + 5% over the past 5 and 10 years. It is noteworthy however, that while a select group of endowments has been quite successful, the overall population has generally struggled in the years following the 2007 to 2009 Global Financial Crisis (GFC), tracking the 65/35 Mix fairly closely.7 We would argue that all nonprofit investors should be actively confronting the likely reality of diminished returns from markets and asking how they can make up the difference.

So the question becomes: Are there lessons to be learned from the organizations above? In our accumulated experience, there are no silver-bullet solutions to be readily applied by all nonprofit investors. Rather, we believe there are a series of time-tested principles that, if employed thoughtfully and consistently, can lead to strong long-term results. At TIFF, these philosophies have worked well for us, and appear to be on display in the results of many of the outperformers that we have been referencing throughout.

1) Equities as the Cornerstone – Wharton professor Jeremy Siegel made a simple argument in his influential 1994 book, Stocks for the Long Run: Over long periods of time, investing in Equity markets has delivered strong absolute returns and better risk-adjusted returns than any other major asset class or investment category. This wide-ranging yet straightforward claim is backed by strong evidence, but seems to be easily forgotten by nonprofit investors.

In our view, Government Bonds, Credit, Commodities, and Real Assets can play a role in nonprofit portfolios. Many endowment investors, however, have weighted these asset classes too aggressively and often at the most inopportune times.

Materially tilting portfolios away from Equities in the short or medium term can be both sensible and beneficial. However, before doing so, an investment office should be realistic about its ability to make these cross-asset class assessments. Additionally, to the extent that this view may persist for an extended period of time, an investment office should be aware that generally, Public and Private Equities will outperform other asset classes over the long-term.

At TIFF, Public and Private Equities (inclusive of Venture Capital, which represents equity stakes in early-stage businesses), adjusted for the proper level of risk given the organization’s characteristics, are always the cornerstone of our portfolios. We make significant use of Hedge Funds and more modest and episodic use of the asset classes listed above. If we were to ever consider a more meaningful or permanent shift away from Equities, we would certainly heed the warnings above.

Last, our analysis shows that the 10 endowments that we have been referencing throughout not only use Equities as their cornerstone, but generally take on greater exposure to Public and Private Equities than the broader endowment community or the 65/35. We will elaborate in the next section on how we believe that this increased exposure has helped to contribute to stronger performance over time.

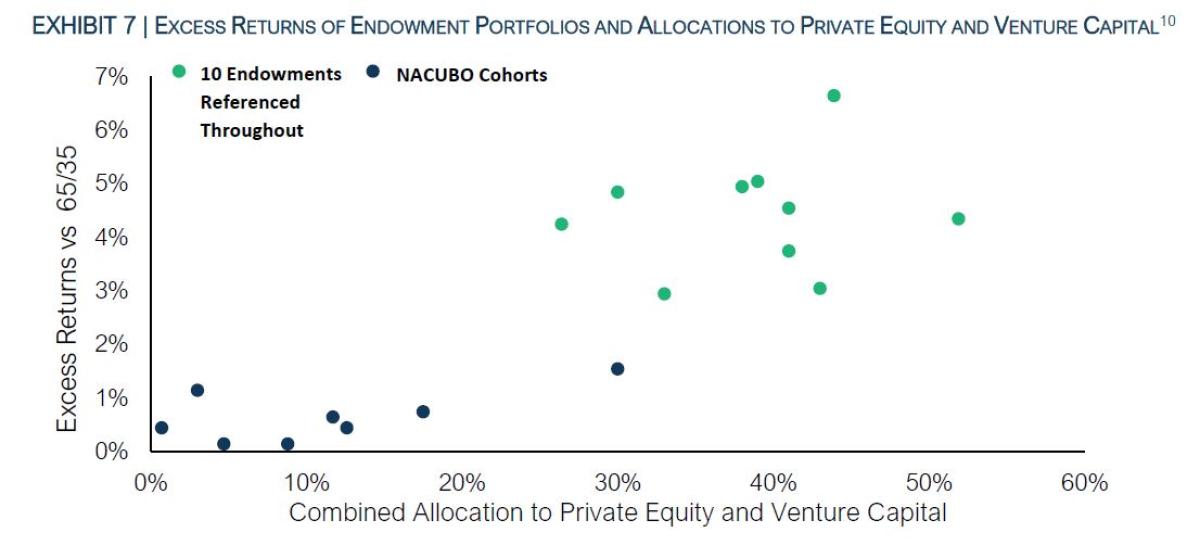

2) Intelligent Use of Alternatives – The annual NACUBO survey provides asset allocation information as well as returns for seven distinct college and university endowment size cohorts.9 The navy blue dots in Exhibit 7 below demonstrate that across these cohorts, the greater the allocation to Private Equity and Venture Capital, the greater the excess return over the past 10 years. Private Equity and Venture Capital have historically featured higher risk, but critically, also higher returns, than Public Equities. We believe this is the primary reason that a more significant allocation to these asset classes appears to be such a clear predictor of outperformance across the cohorts.

Additionally, the green dots in Exhibit 7, representing the endowments we have been referencing throughout this paper, show that these institutions have quite large allocations to these categories and significant outperformance. In our estimation, the outsized performance of these institutions overall can be attributed to their significant allocations to Private Equity and Venture Capital and also to their strong performance within these asset classes. Although it would not be appropriate to comment on the anecdotal reports of the strong private market programs of these college and university endowments, we do feel comfortable sharing some of the underlying drivers of our own outperformance. Below we detail three best practices that have served us well in managing our Private Equity and Venture Capital portfolios.

Smaller Deals and Smaller Managers – In both Private Equity and Venture Capital, our view is that smaller deals will yield better long-term returns. Generally speaking, in private markets smaller deals will feature less competition and a greater opportunity for the operating partners of strong managers to enhance outcomes for the businesses that they’re investing in. In Exhibit 8, we show performance data for Private Equity buyouts, compiled across the entire industry over multiple decades. In our view, the evidence is striking: As the deal quartiles decrease in size, the returns get better. While each investment opportunity is nuanced, in private markets we tend to focus our energy on smaller deals and smaller managers, in an attempt to harness this effect.

Venture Capital Requires Both Experience and Expertise – Venture Capital exhibits significant return dispersion (Exhibit 9), with strong managers delivering outstanding returns and weaker managers struggling. Investors without the relationships to access elite managers and the capability to due diligence them, may be better served in public markets, which can be accessed less expensively, with daily liquidity, and full transparency on holdings. We believe that our long history in seed and early-stage Venture Capital gives us a unique advantage in this market.

Co-Investments and Secondaries as Powerful Complements to Fund Investments – As the Private Equity industry has evolved, Co-Investments and Secondaries have matured as valuable complementary components of investors’ toolkits. Co-Investments may exhibit better long-term returns than fund investments,13 largely because of the significant fee savings. Investment offices with the staffing and expertise to perform the requisite diligence, can further magnify this advantage by participating in select Co-Investments from highly skilled managers with uniquely attractive economics. Secondaries, which can at times be purchased at meaningful discounts, tend to feature prompt return of capital and stronger internal rates of return (or “IRR,” one of the key performance measures used in Private Equity) relative to the broader industry.

At TIFF, for organizations with sufficient financial health, liquidity, and risk tolerance, we will often feature private market allocations exceeding 30%. Our private market programs typically allocate approximately 70% of market value to primary fund investments, with approximately 30% to Co-Investments and Secondaries.

3) Key Public Market Manager Characteristics – Selecting public market managers that consistently beat benchmarks is difficult, but not as difficult as some would have you believe. In our view, investors should focus on managers with a handful of simple characteristics that tend to lead to strong outperformance over time. Specifically, we have found that managers with less AUM (Assets Under Management), incentives aligned with their investors’, and specialized domain expertise are better positioned to deliver excess returns than managers without these characteristics. Below we expand on each of these ideas.

Managers with Smaller Capital Bases – Within Public Equity markets generally, we are of the belief that the smaller the firm is, the less attention it will receive from analysts and institutional investors, and the more likely it is to be materially mispriced by the market. A savvy portfolio manager can take advantage of these mispricings, but only if managing a portfolio that is sufficiently small to be able to size attractive positions significantly. It is important to note that, unlike in private markets, we are not arguing for a premium associated with smaller firms. Rather, our view is that material mispricings are more common for small firms relative to large ones and that a smaller manager is better able to take advantage than a larger manager. At the risk of oversimplifying the point: Small managers have flexibility to hold whatever securities they want in whatever size they want and can enter and exit with modest transaction costs. Conversely, in an extreme scenario, a large manager will be more confined to the largest and most liquid stocks in a given market.

While each market, manager, and trading style is different, at TIFF we have consistently observed that a small capital base is a good indicator of future success. There is empirical evidence to substantiate this approach. Exhibit 10 comes from a recent study14 that focused on the drivers of manager outperformance. It shows that small- and medium-sized managers outperform larger counterparts. This outcome has been replicated by academic researchers several times across different asset classes and time periods.15

Aligned Incentives – Warren Buffet’s partner at Berkshire Hathaway, Charlie Munger, has said, “Show me the incentives and I’ll show you the outcome.” Measuring and assessing incentive alignment is one of the more straightforward aspects of manager selection. Relative to other more nuanced variables, elements such as portfolio management compensation, personal money invested, and ownership of the firm are fairly easy to assess. Despite their simplicity, these foundations are important aspects in any manager evaluation that we undertake.

Exhibit 11, excerpted from the same study as Exhibit 10, shows that privately owned firms outperform managers owned in the public markets or those owned by a financial institution. Implicit in this analysis is the idea that privately owned managers are more aligned with investors than managers with other ownership structures and business goals.

Specialized Expertise – Regardless of fund size or manager alignment, performance is driven by an ability to identify and invest in mispriced assets. In our view, specialist investors with highly detailed knowledge of an industry, sector, country, or region are better able to develop and maintain that expertise than a generalist. For example, the Biotech industry evolves at an incredibly rapid pace and requires a detailed level of expertise to understand the science, trends, and firms impacting it. Similarly, the Chinese and Indian equity markets, with their enormous populations and unique cultures, and histories, operate very differently than other markets. In these areas, we believe that specialized knowledge is required to truly understand the dynamics driving firm-level outcomes.

Given that these three characteristics are pillars of our selection process, it should come as no surprise that our manager roster is comprised of many smaller, privately held, specialist firms. That is not to say that all our managers embody each of these characteristics. Rather, our view is that each of these characteristics, all else equal, is a strong predictor of future outperformance, and therefore are important ingredients in picking managers.

Having identified these characteristics and cited the empirical evidence that indicates associated outperformance, why aren’t all institutional investors allocating capital this way? The reality is that identifying and partnering with these types of managers is difficult in a few ways. These managers are not typically found in major cities, aren’t well known to the public, and are frequently new or quite small. Additionally, as these smaller managers experience success and increase their assets under management, many become unwilling to take capital from new investors. Even institutional investors that do have the resources, expertise, and patience to execute the needed due diligence, are sometimes simply unwilling or unable to invest less conventionally and would prefer the comfort of larger, better-known managers. While we do not begrudge any approach and are humble about our ability to forecast the future, the evidence seems to indicate that our philosophy has the odds on its side over the long term.

CONCLUSION

FY2021 endowment investment results were outsized – but consistent with the market environment that fueled them. While we do not expect a meaningful economic slowdown or crash in risk assets, the markets are likely to provide less of a performance tailwind going forward. That said, we do strongly believe that by focusing on the three key elements we have outlined – Equities as the Cornerstone, Intelligent Alternatives, and Key Manager Characteristics – we have provided a roadmap for nonprofits with the requisite resources to generate returns above what the global economy and broad indices are offering. Capturing these excess returns on behalf of our nonprofit members and allowing these honorable organizations to better accomplish their missions encapsulates our mission at TIFF.

Footnotes:

1. NACUBO stands for the National Association of College and University Business Officers. The organization produces annual comprehensive reports on endowment asset allocation and returns. FY2021’s result is the highest return since 1991, the start date of the data available to us.

2. Sources: NACUBO Fiscal 2021 report, Bloomberg, and each institution’s website. 65% MSCI ACWI / 35% Bloomberg Barclays Aggregate. The 10 individual endowments here will be referenced throughout the paper and were selected for inclusion based on having the strongest returns over the 10 years ending 6/30/2021. We sourced these returns from Pensions and Investments. We excluded any endowments for which we were not able to locate a publicly available asset allocation.

3. Sources: NACUBO Fiscal 2021 report and Bloomberg are sourced for Exhibits 2 and 3.

4. Private Equity and Venture Capital returns represent the Cambridge Associates indices and Hedge Fund returns are from Hedge Fund Research (HFR).

5. For each asset class we take the prior-year weight and multiply by the most relevant index’s current-year return. We don’t expect this calculation to tie exactly to the aggregate NACUBO figure, but we do expect it to be quite close, which it is (i.e., 30.6% vs. 30.3%). US Equities, Non-US Equities, Private Equity, Hedge Funds, Venture Capital, and FI, Real Assets, Other are represented by S&P 500, MSCI ACWI ex US, Cambridge Associates Private Equity, Hedge Fund Research (HFR) Fund Weighted Index, Cambridge Associates Venture Capital, and Barclays US Aggregate indices, respectively.

6. Source: Robert Shiller Data.

7. The aggregate performance challenges of nonprofits are well documented in the academic literature: “Do (Some) University Endowments Earn Alpha” (2013) by Barber and Wang; “A Better Approach to Systematic Outperformance? 58 Years of Endowment Performance (2020) by Hammond; “Endowment Performance” (2020) by Ennis.

8. 5- and 10-year returns are as of June 30, 2021. Returns are sourced from NACUBO Fiscal 2021 report, Pensions and Investments, or directly from Endowment website.

9. The size cohorts are: <$25 million; $25-$50 million; $50-$100 million; $100-250 million; $250-500 million; $500-1 billion; and >$1 billion.

10. Exhibit 7 reflects 10-year returns and asset allocation weights as of June 30, 2021, for the NACUBO size cohorts and the select colleges and universities that are referenced in Exhibits 1

and 6. Excess Returns are in comparison to 65% MSCI ACWI / 35% Bloomberg Barclays Aggregate. The NACUBO size cohorts are the same as referenced in footnote 9.

11. Source: "Private Equity Portfolio Companies: A First Look at Burgiss Holdings Data," by Brown, Harris, Hu, et al.

12. Source: Cambridge Associates venture capital index, as of June 30, 2021.

13. “Adverse Selection and the Performance of Private Equity Co-Investments” (2018) by Braun, Jenkinson, and Schemmerl.

14. “Investing with External Managers” (2020), Norges Bank, Investing with external managers (nbim.no).

15. For instance, “Does Fund Size Erode Mutual Fund Performance? The Role of Liquidity and Organization” (2004) by Chen, Hong, Huang, and Kubik.

Read the original article: TIFF.org/higher-education-endowment-results-reflections-and-outlook

Originally Published Spring 2022 ©TIFF Investment Management. All rights reserved. May not be reproduced or distributed without permission.

About the Author:

Matthew Hoehn joined TIFF in 2021 and is the Co-Head of Custom Asset Allocation. He serves as the lead portfolio manager for a number of TIFF members and is also responsible for TIFF’s framework that tailors Strategic Asset Allocation (SAA) to the unique characteristics of an organization. Before joining TIFF, Matt spent the prior four years as a senior investor at BlackRock, managing Endowment and Foundation OCIO portfolios. From 2003-2017, he was at Goldman Sachs Asset Management (GSAM), where he served as the named portfolio manager on a number of multi asset class investment strategies that spanned public and private markets. Matt is a member of TIFF’s investment committee.

Matt graduated, magna cum laude, from The College of New Jersey in 2002 with a double major in Economics and English. He also has a Master’s Degree in Economics from New York University. He has volunteered on a number of nonprofit boards and committees, most recently on the Executive Director’s Council at Cents Ability, an organization that aims to bring financial education to underprivileged high school students.

Matt lives in Glen Ridge, New Jersey with his wife and three daughters.

Disclosures

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance. There is no guarantee that any particular asset allocation or mix of strategies will meet your investment objectives.

The materials are being provided for informational purposes only and constitute neither an offer to sell nor a solicitation of an offer to buy securities. These materials also do not constitute an offer or advertisement of TIFF’s investment advisory services or investment, legal or tax advice. Opinions expressed herein are those of TIFF and are not a recommendation to buy or sell any securities.

The enclosed materials may contain forward-looking statements relating to future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” the negative of such terms or other comparable terminology. Although TIFF believes the expectations reflected in the forward-looking statements are reasonable, future results cannot be guaranteed.

The NACUBO survey data for a particular fiscal year is typically available two quarters after the fiscal year-end. The NACUBO returns shown in this presentation, which are based on a survey of 720 institutions, are net of management fees and expenses. The NACUBO All Institutions average is the average compounded nominal rates of return of the participating institutions’ endowments. Large Institutions are those with endowments in excess of $1 billion. Small Institutions are those with endowments of $25m-$50m. The investment approaches and performance goals of the NACUBO institutions vary widely and may vary significantly from TIFF’s approach. See Disclosures pages for additional information about NACUBO. University endowments typically include allocations to private investments. The performance goals of the institutions in the NACUBO survey may and typically do differ from the goals and targets of all nonprofit institutions.