By Ihor Dusaniwsky, Head of Predictive Analytics at S3 Partners, a leading financial data marketplace and workflow platform that specializes in long and short-position data and analytics.

Looking through binoculars can give you a clear picture of the specific object you are looking at but does not necessarily give you an idea of what the landscape truly looks like. While there have been short squeezes and significant short covering in some names and sectors, the reality is that overall short interest in the market has increased since the major indexes hit their recent lows on June 16th.

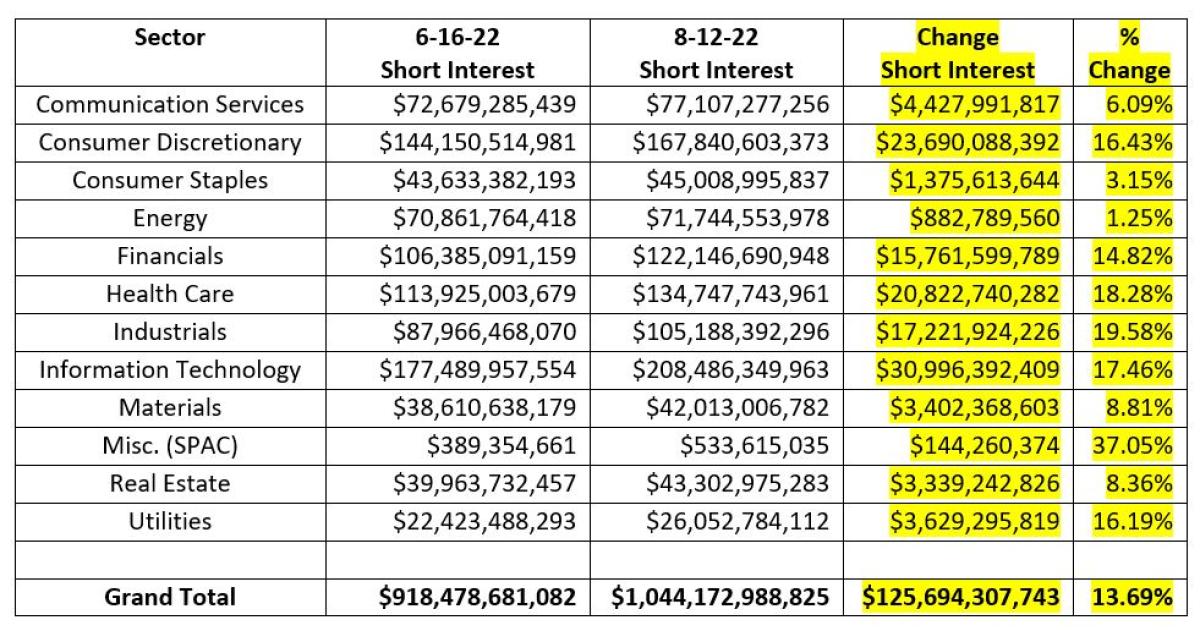

Looking at the domestic market, which includes U.S. and Canadian listed names (most of the largest Canadian names are dual listed), short interest has increased by $126 billion, or 18.6%, since June 16th. The largest increase in short exposure in dollar terms occurred in the Information Technology, Consumer Discretionary, and Health Care sectors while the smallest increases occurred in the Energy and Materials sectors.

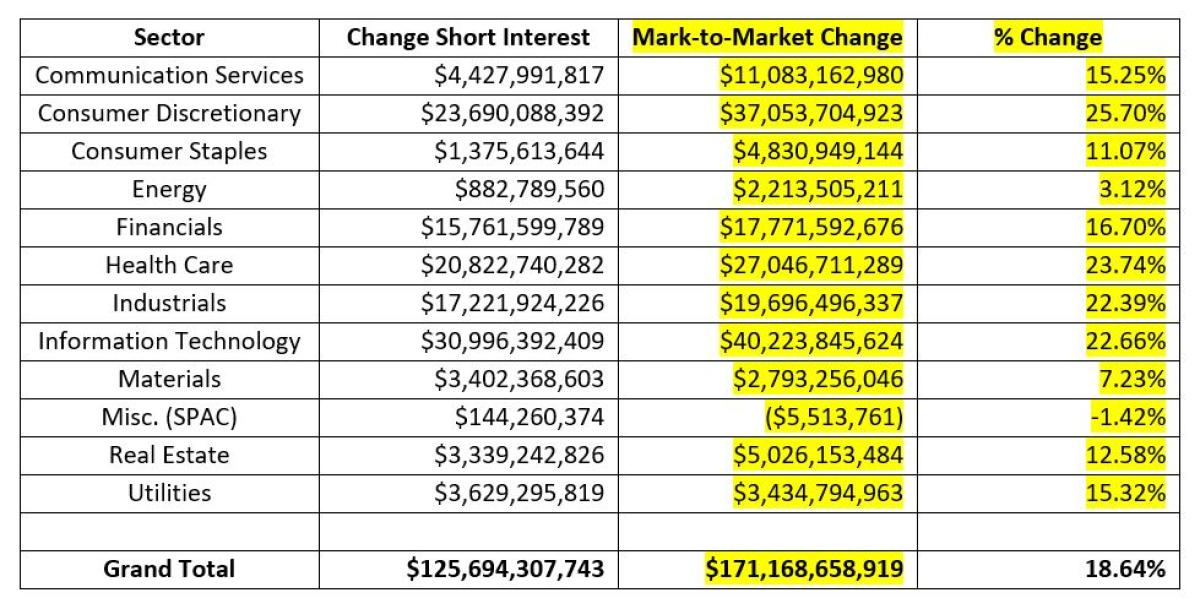

Change in short interest is made up of the mark-to-market change in the value of the shorted stocks coupled with new short selling or short covering. Looking at short interest, or the dollar value of shorted shares gives us the actual dollars at risk in the short side of the market which is not possible when looking at SI % Float. Risk management and limits are dollar-based (a 1,000 share or $300k Berkshire Hathaway B short is a riskier position to a portfolio than a 1,000 share or $10k Carnival Corporation short), profit & loss calculations are dollar-based (no one says they crushed a trading day and made 100 shares) and margin and leverage calculations are dollar-based (shares may not change but if stock prices change, leverage ratios will fluctuate, and margin calls can occur).

The market rallied significantly after June 16th with the larger cap S&P 500 up +16.73%, the more tech-based Nasdaq up +22.55%, and the broader Russell 3000 up 17.60%. These market-wide gains increased the mark-to-market value of the shares shorted by $171.2 billion, or +18.64%. The sectors with the largest increase of short interest in dollar terms were the Information Technology, Consumer Discretionary, and Health Care sectors while the smallest increases were in the Energy and Materials sectors.

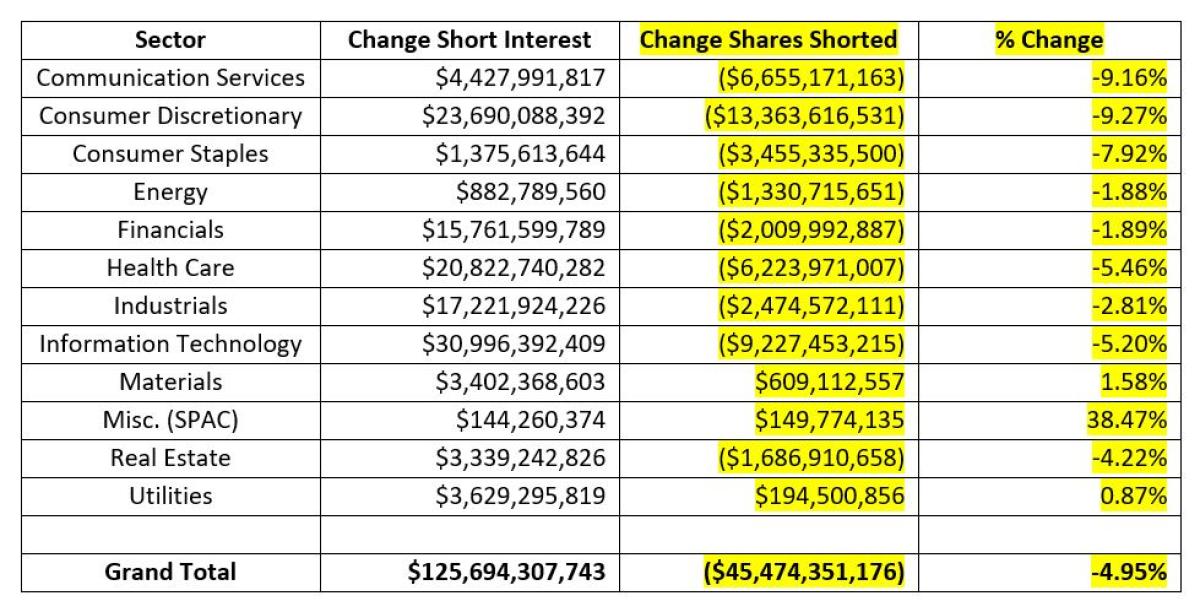

As the value of shorted shares increase or decrease due to changes in their underlying stock prices, short sellers will short more shares, buy-to-cover or stand pat depending on the amount of short side risk they want to take. Overall, short sellers were actively buying-to-cover as the value of their shares increased – indicating that although they were amiable to an increase in their short exposure, the rally pushed their exposure up too far and needed to be trimmed.

Short sellers ended up covering $45.5 billion of their short positions, reducing their short exposure by -4.95%. The largest amount of short covering in dollar terms occurred in the Consumer Discretionary, Information Technology, and Consumer Services sectors while the only two sectors with increased short selling were the Materials and Utilities sectors (the Misc. SPAC sector is not an official sector).

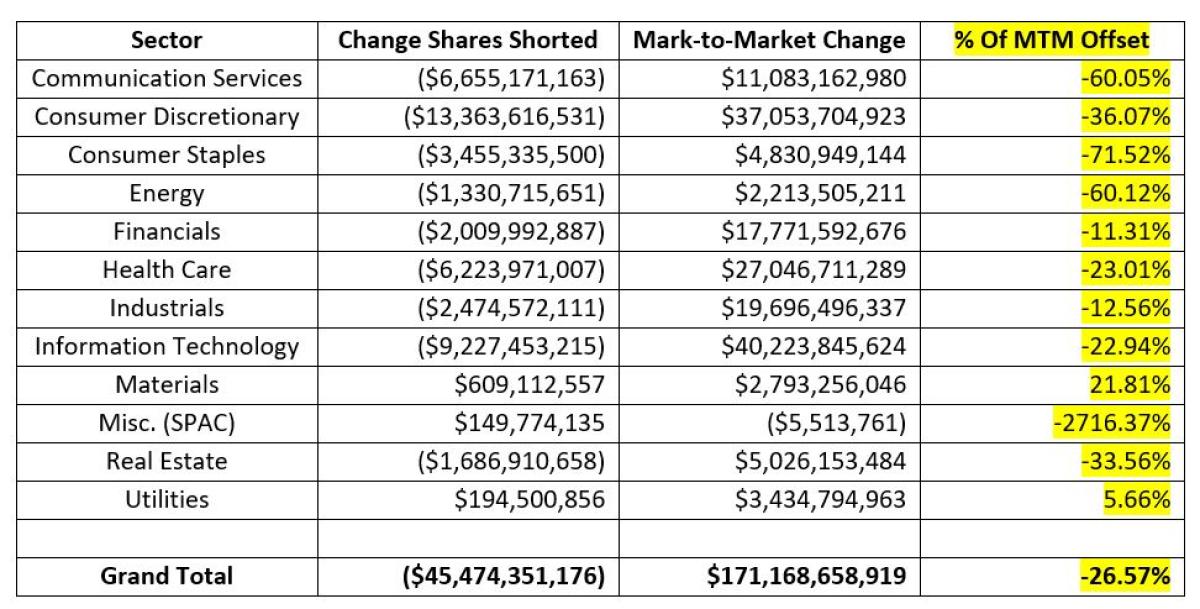

Short sellers offset over a quarter of the mark-to-market increase of the value of shares shorted. The largest “offsets” occurred in the Consumer Staples, Energy and Communication Services sectors while we saw increased short-selling in the Materials and Utilities sectors.

While there has been short covering in the domestic market during rallies, the short-side may not have been reducing their overall short-side exposure to the market. It may indicate that institutions looked at the upward market movements as a “bear rally” and were expecting a pullback in share prices across the broad market if the recession continues or worsens and the Fed is forced to raise rates higher or quicker than expected. It can also indicate that institutions are building up their long books in anticipation of a future rally and the increased short interest is just the associated short hedge growing along with the long side.

After missing out on a rally, institutions may start to increase their market exposure in order to make up for returns they already missed. An increased short interest across all sectors could be nothing more than short hedges to offset beta to increase alpha in a portfolio.

Yes, short covering occasionally helps to drive up the market. It does not necessarily mean the institutional side is deleveraging. They may merely be adjusting the tenor of their short book to better hedge a long book that is growing to make up for lost alpha.

Looking at short-selling trends over time provides insight into overall market sentiment as well as the strength of bearish conviction in individual equities. Our Blacklight SaaS platform and Black APP provide an up-to-date view of short selling and short covering on an equity, sector, index, or country-wide basis allowing investors\traders to better manage their existing long and short positions.

Here's an excellent article on how Apple is now the #1 short - surpassing Tesla.

About the Author:

Ihor Dusaniwsky is the Head of Predictive Analytics at S3. One of the first employees at the firm, Ihor joined S3 in 2003 after spending many years as a senior stock loan trader. He uses his extensive knowledge and relationships in domestic and international stock loan markets to provide insight and market color to S3’s clients. Ihor publishes research on the short side of the market and develops internal systems and algorithms which help S3’s clients manage their portfolios and gain insight into worldwide short selling activity and financing trends.

Prior to joining S3 Partners, Ihor was the Senior Equity Finance Trader at Commerzbank Capital Markets and Global Head of Agency Lending at Morgan Stanley. Prior to his role in securities finance, Ihor was the Global Head of FX Controllers and the Equity & Derivatives Controller at Morgan Stanley. During his tenure at Morgan Stanley, Ihor worked in the New York, Tokyo, Hong Kong and London offices. Ihor received a B.A. in Finance, Magna Cum Laude, from New York University and majored in Industrial and Labor Relations at Cornell University.