By Charles Skorina, Managing Partner at Charles A. Skorina & Company.

"We've long felt that the only value of stock forecasters is to make fortune tellers look good." — Warren Buffett

Howard Marks sent out a memo last week – The Illusion of Knowledge – in which he ponders the value of economic forecasts. He concludes that they aren’t worth much to anyone but the forecasters.

As recruiters evaluating senior investment talent we wrestle with a comparable conundrum, how can we make informed judgements about candidates and their success in the future when our knowledge and intuition is based on the past?

Don’t get us wrong, we meet exceptional clients and candidates almost every day – smart successful families, board members, and professional investors at the top of their game.

But interviewing chief investment officers and up-and-comers is a bit like camping with Garrison Keillor at Lake Wobegon, “where all the women are strong, all the men are good-looking, and all the children are above average.” We have yet to meet a candidate who hasn’t produced top quartile results.

Almost everyone is convinced they can pick superior managers and investments while the other guy rolls snake eyes. Active management is for heroes, indexing for geezers.

In our interviews for institutional and family office clients we often hear the comment that public markets are nearly impossible to beat, yet in the next breath they tell us their endowment or foundation team has consistently beaten public market benchmarks using active managers.

While we are impressed by their conviction, we wonder about their claims.

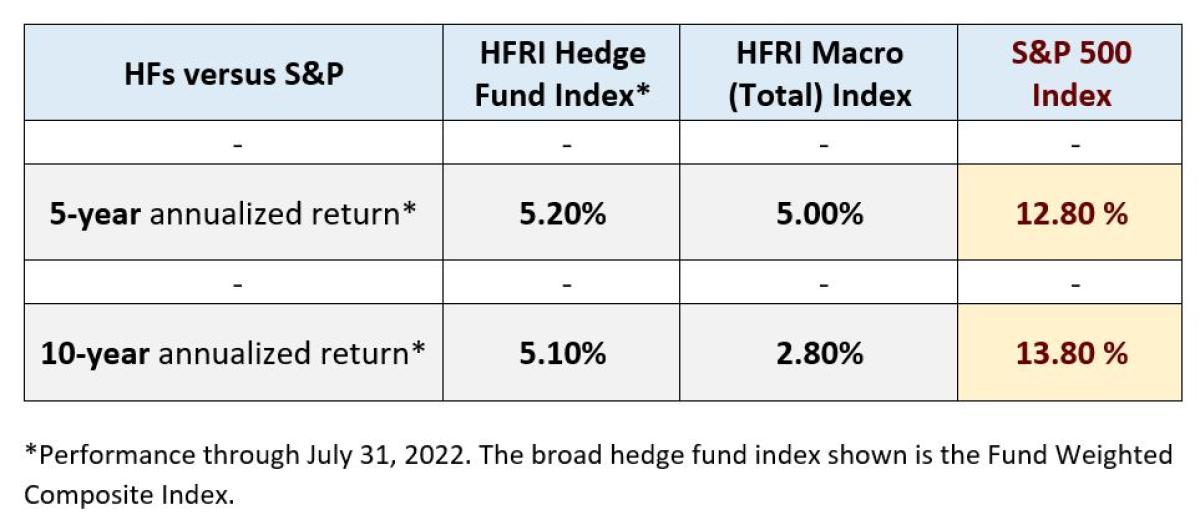

We’re in good company. Mr. Marks has also questioned the track records of active managers, at least those who place bets on macro trends. So, he sourced a few Hedge Fund Research (HFR) performance metrics for guidance. This is what he found.

And remember, these are arguably some of the smartest guys and dolls on the Street.

You can’t beat Art History

The chart above focuses solely on hedge fund performance. Large endowments on the other hand, with AUM over one billion dollars, hold on average well over one hundred active managers across the investment spectrum, with some managing close to three-hundred funds (asset managers, commingled funds, and partnership interests, NACUBO Study 2019).

Are there really that many exceptional top quartile managers? Enough to fill the portfolios of hundreds of family offices, public and corporate pensions, endowments, foundations, hospital systems, associations, and charities? About $49 Trillion worth of AUM in north American according to the Boston Consulting Groups’ Global Asset Management Report 2021.

Maybe it’s true, that great investment staffs can pick great managers year in and year out.

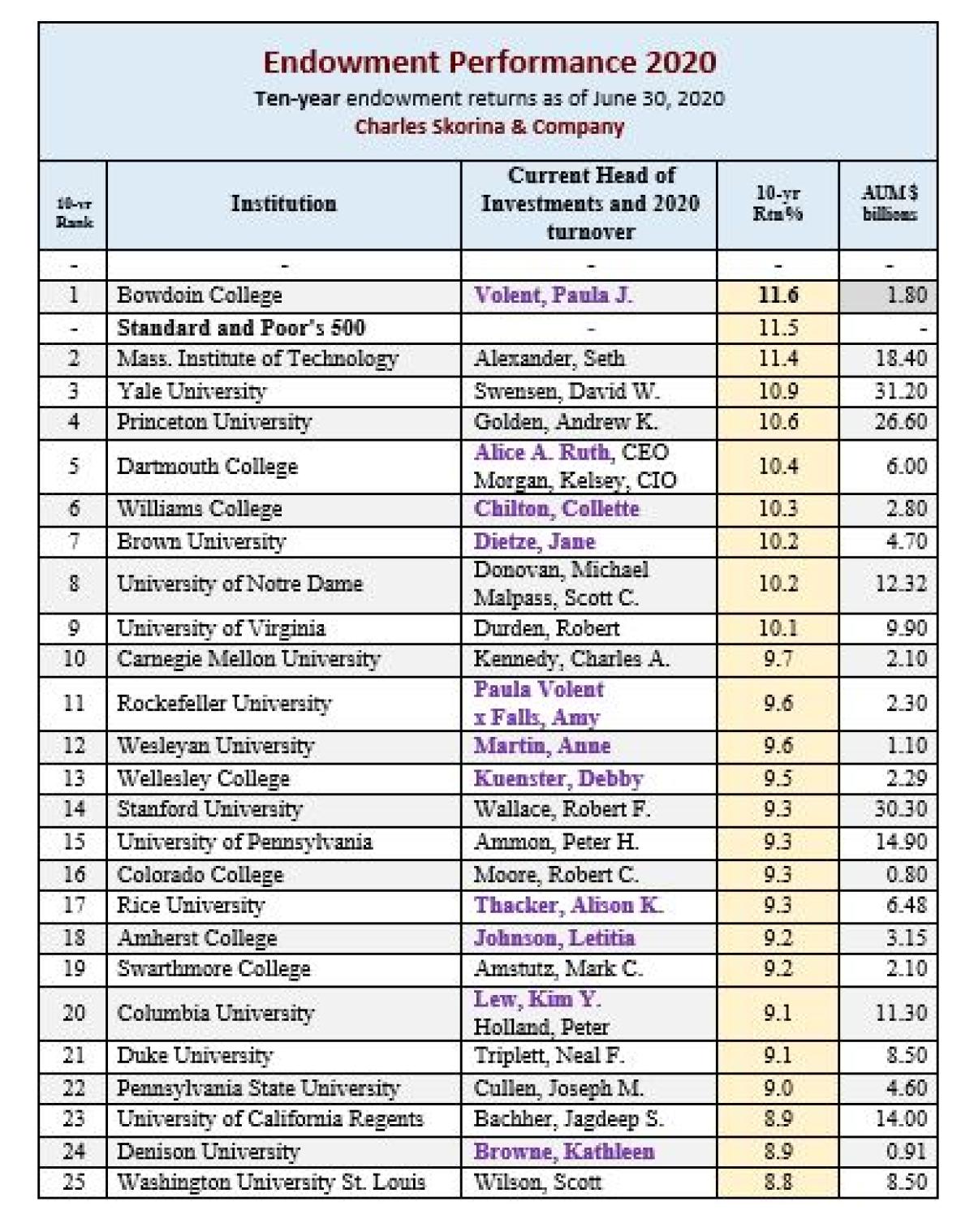

But in our last ten-year performance study ending June 30, 2020, only one endowment chief investment officer, Ms. Paula Volent, now the CIO at Rockefeller University in NYC, beat the S&P 500 over ten years. Just one, and she started out as an art historian and conservation specialist! A rare win for culture.

Active Management Pays the Bills

As we wrote in our last newsletter, “the asset management business is diverse, powerful, and exceptionally profitable,” and most of that money is made in active management.

Profit margins for the mutual fund industry alone are estimated at 30% and more. And yet, as S&P noted in their year-end 2021 score card, 79.6% of domestic equity funds lagged the S&P Composite 1500.

"Over a ten-year period as of July 1, 2022, only 26% of funds [large cap] have beaten the S&P BSE 100 Total Return Index."

So, if the investment seers can’t pick winning investments, how can CIOs pick winning managers, and how can recruiters identify top CIOs?

Our Not-So-Secret Sauce

Ultimately, we fall back on what we know, our process. This is both data-driven – can we identify skill and persistence in a candidate’s performance? And backed by intuition and experience – does the candidate’s resume catch our eye? Is there something special in their background? Schools? Jobs? Successes or failures?

Recruiting is as much an art as a science and every search consultant has their own style and technique. When we meet a prospect, we use a simple three-column grid as our guide with character, compatibility, and content as headings.

Character embodies the qualities that define the individual, and Compatibility – that elusive emotional IQ that Daniel Goldman writes about – builds trust, but Content is knowledge accumulated over a lifetime and we look forward to learning something new in every interview, an investment thesis, an upcoming manager, topical news, an off-the-cuff remark.

Unfortunately, it is surprising difficult for many senior institutional investors to put what they know into words. Maybe it’s just caution or maybe it’s groupthink, but we are often disappointed.

It’s hard to break from the herd and dangerous to talk about it. Media trolls lurk under every rock ready to strike at any nonconformist comment. Career risk is too great to be different and the reward for being like everyone else is a comfortable year-end bonus.

Insights from a Pro

A while back we asked Joe Dowling, global head of Blackstone Alternative Asset Management (BAAM) and former Brown University chief investment officer, what makes a great investor. Here is his reply.

They have the ability to step away from the crowd

They have the ability to step away from the crowd and have a variant perception and then act with conviction. They have different experiences that add up to cumulative investment knowledge. They develop a diverse lens to evaluate markets, managers, and opportunities.

They see patterns

CIOs meet with a lot of managers. Successful investors need to develop pattern recognition. A CIO probably needs to have met and evaluated at least four-hundred managers before they begin to really know what they are doing.

They have intellectual curiosity

They have intellectual curiosity and a strong work ethic. Nobody works harder than Paula Volent and Jane Dietze – they grind it out. And the work is intellectually interesting to them. They are not tourists.

They are relentless networkers

They are dynamic and social. Fund managers like them so there is a fly-wheel effect. Their networks expand and, as a result, they are fed more and more opportunities.

They have humility

They have made a ton of mistakes but view them as learning experiences. They know and appreciate how difficult the business is. This filters through to the managers.

They can handle the politics

They know how to engage, manage, and benefit from their investment committees. This allows them to rebalance into dislocations, pioneer new models like, for example, staking managers or investing in crypto before the herd took notice.

Final Thoughts: Character and Fate

The Greek philosopher Heraclites wrote “a man’s character is his fate.” We can observe, inquire, consider but can we ever really know the person behind the mask?

There are no sure bets when hiring investment talent, so many variables. The life they have lived, the organization they are joining, temperament, behavior, fit.

And as Paul Wachter, former investment chair of the University of California Regents said a few years ago, “what you can’t tell in an interview is how good of an investor someone is. If you look at their track record in their previous position, you’re seeing the product of an entire team or institution.”

In the end, we work with what we've got. We can still make the call.

About the Author:

CHARLES A. SKORINA works with leaders of Endowments, Foundations, and Institutional Asset Managers to recruit Board Members, Executives Officers, Chief Investment Officers, and Fund Managers.

Mr. Skorina also publishes THE SKORINA LETTER, a widely-read professional publication providing news, research and analysis on institutional asset managers and tax-exempt funds.

Prior to founding CASCo, Mr. Skorina worked for JP MorganChase in New York City and Chicago and for Ernst & Young in Washington, D.C.

Mr. Skorina graduated from Culver Academies, attended Michigan State University and The Middlebury Institute of International Studies at Monterey where he graduated with a BA, and earned a MBA in Finance from the University of Chicago. He served in the US Army as a Russian Linguist stationed in Japan. Charles A. Skorina & Co. is based in Tucson, Arizona.