By TresVista, a global enterprise offering a diversified portfolio of services that enables its clients to achieve resource optimization through leveraging an offshore capacity model.

Executive Summary

As the global focus shifted from post-pandemic exhilaration to caution following macroeconomic tightening, conflict and inflation scares, the Private Equity (PE) industry followed suit, with fund managers factoring in a potential recession following closely on the heels of the recovery from the pandemic. H1 2022 witnessed a shift in investor sentiment as bearish sentiment began to overshadow H2 2021's market euphoria, a prominent silver lining being more realistic valuations in general. The fund managers we surveyed were more conservative overall in H1 2022, with those dominant macro events (including the public market drawdown) observed so far in 2022 as the primary drivers for this sentiment.

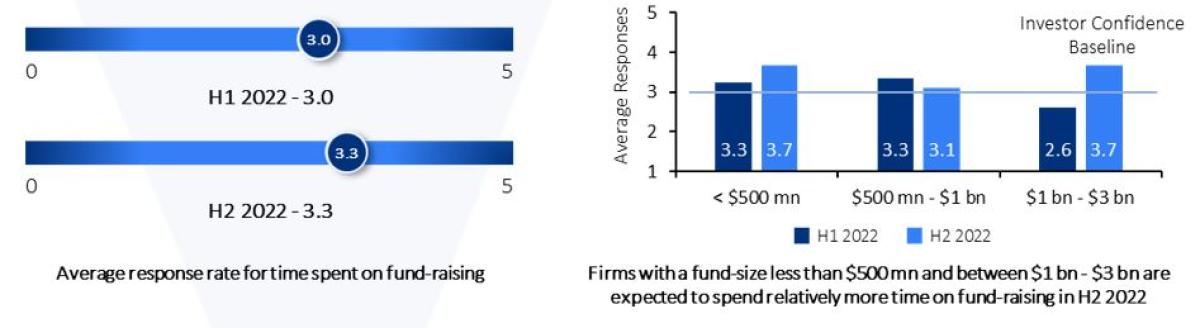

During H1 2022, these investors prioritized portfolio management activities as businesses navigated challenging headwinds. Investor sentiment toward holding periods and distressed asset quality was largely similar to H2 2021, which portrayed neutral sentiment toward holding periods and more positive sentiment regarding distressed asset quality. In terms of deal flow, H1 2022 was slightly weaker than H2 2021, when comparing the volume and quality of inbound/outbound opportunities; however, U.S. Middle Market PEs anticipate an increased focus on deal origination in H2 2022, as they are expecting pipelines to improve gradually. On fundraising, securing Limited Partners' (LP) allocations has been tough for emerging funds in H1 2022, according to a few respondents - especially as the LPs allocated their full annual amounts to re-ups in Q1 2022. In addition to rising interest rates, H1 2022's extensive valuation cuts incited a hold on the formerly heated IPO and SPAC routes.

Our respondents foresee an overall bearish environment for H2 2022, as investor sentiment is expected to continue to decline but at a more arrested momentum compared to H1 2022.

Index Methodology

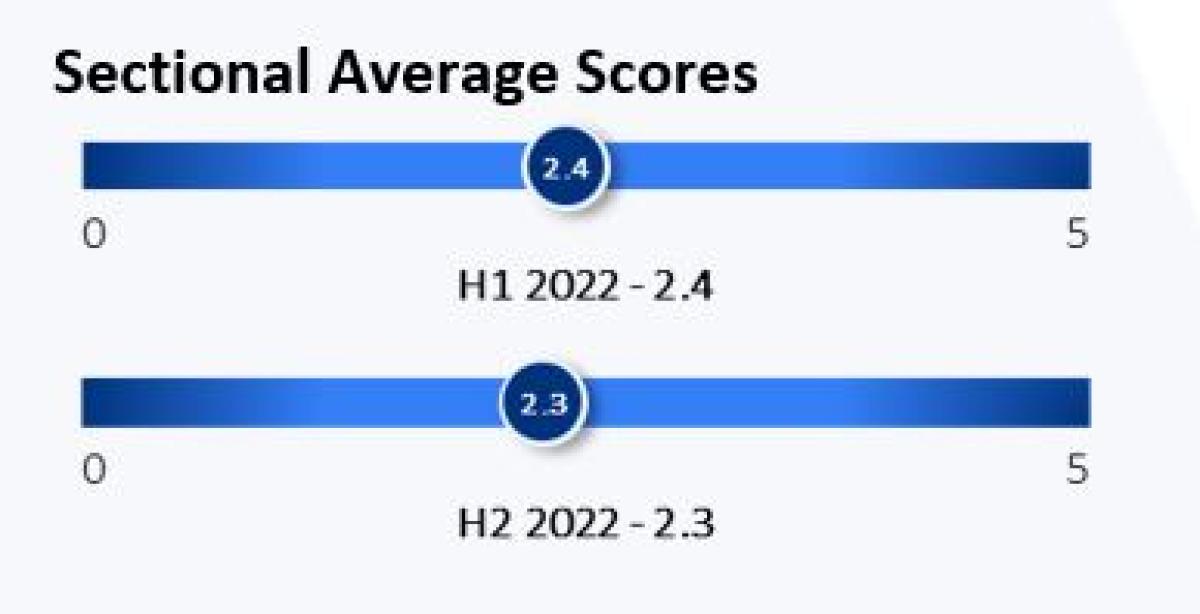

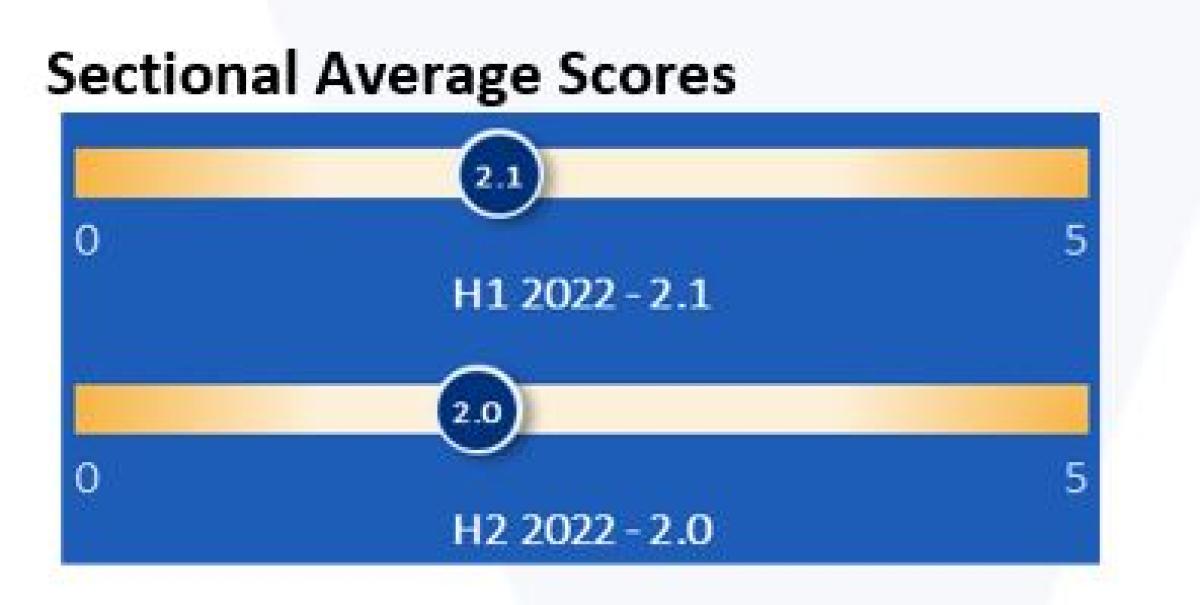

The TresVista Investor Confidence Index aims to capture the changing investor sentiments in the U.S. Middle Market PE industry. We spoke to PE professionals to measure changes in activity levels in key business functions and overall investor sentiments for U.S. Middle Market PEs over the last six months (H1 2022 vs. H2 2021) and their outlook for these over the next six months (H2 2022 vs. H1 2022).

The responses to the questions under these sections are captured using a 5-point Likert Scale and are assigned numerical values from 1-5. The score of the preceding period serves as the Investor Confidence Baseline Score for the current period. An aggregate score of 3 (Investor Confidence Baseline Score) implies no change in investor sentiment for the period under consideration compared with the preceding period. An aggregate score above 3 means a boost or positive change in confidence. Similarly, a score of less than 3 implies a decline or negative shift in confidence. The sectional questions are coalesced in proportion to their weights and correlation to arrive at an index value for the respective section. The final index value calculated reflects all the sections' weighted average value and indicates the overall shift in investor confidence compared to the preceding period.

Qualitative questions were used to delve further into the index value, gain deeper insights behind the score's rationale, and highlight the larger trends driving the current investor sentiments.

Key Takeaways

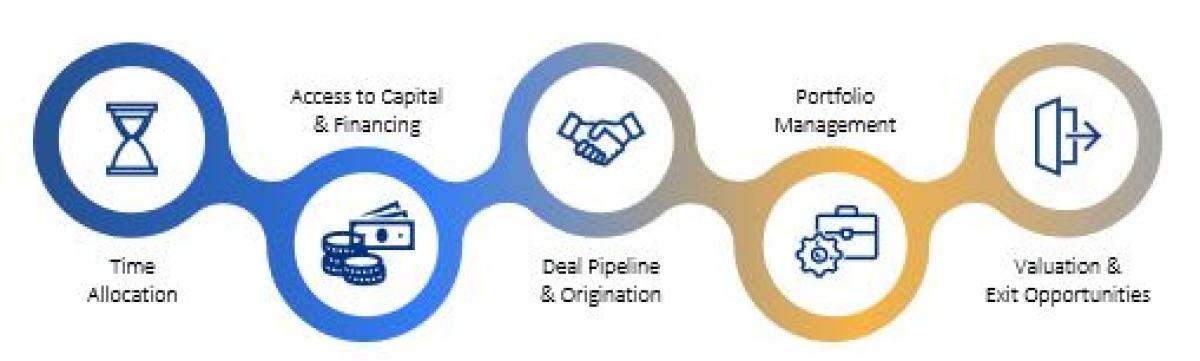

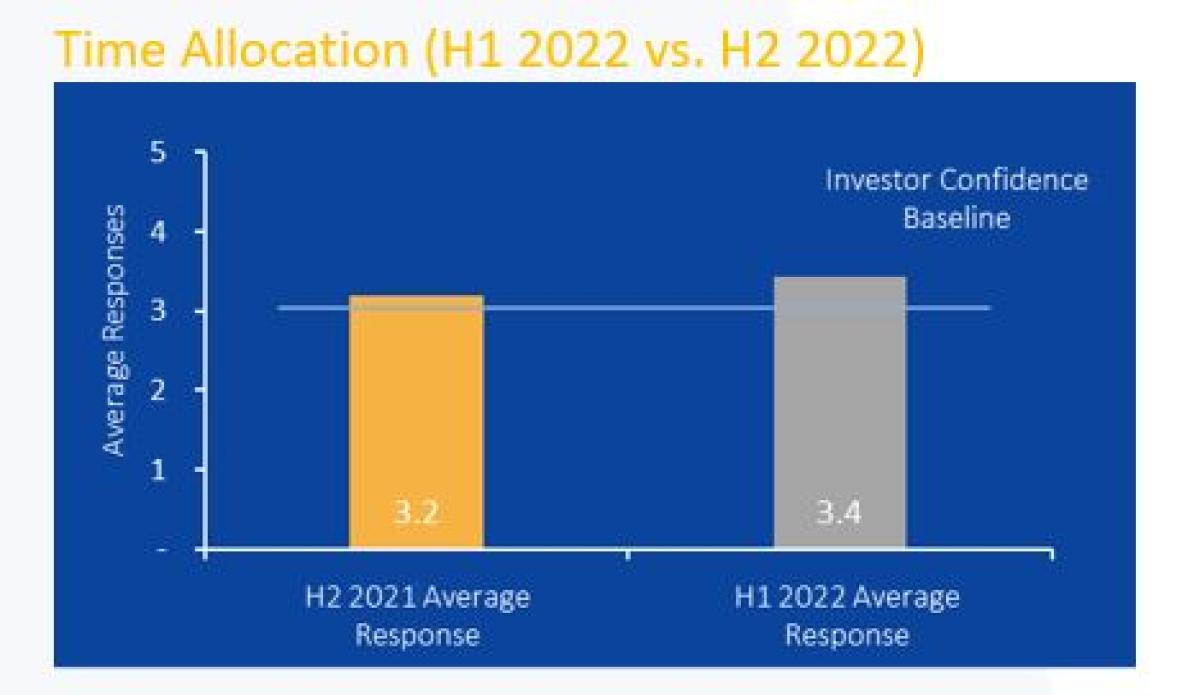

Time Allocation

U.S. Middle Market PEs largely continued to allocate similar time toward fundraising, deal origination, and new deal diligence activities in H1 2022, compared with H2 2021. Fund managers, however, spent more time on portfolio management activities, supporting their portfolio companies in the unfavorable macro environment in H1 2022 compared to H2 2021. The time allocated to all four activities is expected to rise marginally in H2 2022 as PEs further adapt to macro-level uncertainties.

Access to Capital and Financing

In H1 2022, LPs disbursed capital cautiously into newer funds, and as a result, the PEs felt constrained in their access to capital. Re-ups became the norm in the period, and are expected to feature prominently in the financing provided by LPs in H2 2022, as the bearish conditions continue to discourage LPs away from newly-formed funds - excepting perhaps thematic allocations.

Deal Pipeline and Origination

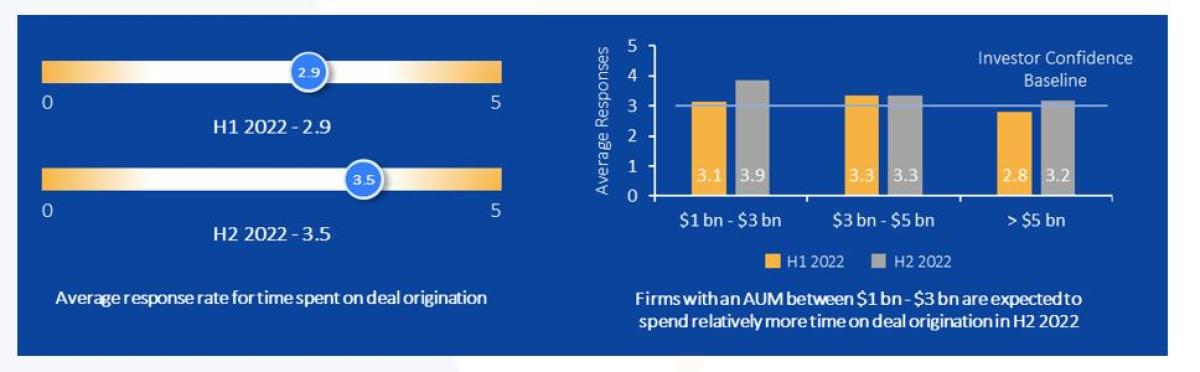

During H1 2022, deal origination and pipeline development demonstrated mixed tendencies. The overall deal flow (total and inbound opportunities) deteriorated in terms of the number of deals and quality. A slight increment was seen in deal close timelines due to the quality of deals. Average transaction size also saw a marginal increment. The U.S. Middle Market PE funds mostly competed for smaller deals and add-ons during H1 2022. Deal pipeline/origination aspects in H2 2022 could continue the trends observed during H1 2022.

Portfolio Management

The investor sentiment toward the holding period for portfolio investments and the quality of distressed and underperforming assets in H1 2022 remained similar to H2 2021, which witnessed neutral sentiment toward holding periods and positive sentiment toward distressed asset quality. As PEs absorb the market drawdown gradually, both holding periods and distressed asset quality could trend similarly in H2 2022, negatively impacting portfolio quality.

Valuation and Exit Opportunities

As public markets witnessed a significant correction in H1, PE valuation multiples were also affected. The gap between buyer-seller valuation outlook also rose as buyers cut valuations and sellers postponed transactions to obtain certainty about the macro environment. Further, IPOs/SPACs were no longer a compelling exit option for sellers. This gap is expected to widen at a slower rate in H2 2022 as compared to H1 2022 as the correction becomes more prevalent. The fund managers also expect valuations and exit opportunities to display a downward trend in H2 2022.

Time Allocation

Experiencing the significant public market correction globally, the U.S. Middle Market PEs spent almost similar time on deal origination, fundraising, and due diligence activities and focused more on portfolio management activities in H1 2022. There was a focus on deal quality due to a decline in expected valuations and rising interest rates. The time allocation for all four activities may increase slightly in H2 2022, which is expected to be primarily driven by prolonged macro-level concerns (rising interest rates, inflation) and a delay in the stabilization of public markets.

Time spent on fundraising activities during H1 2022 remained consistent with H2 2021. This was attributed to a decrease in capital allocation by LPs in Q2 2022. An overallocation in Q1 2022 may have led to a fundraising crunch during the rest of the period.

Investors' focus on deal origination fell slightly in H1 2022. According to a few participants, this was due to a decline in deal flows in the period for which delays to changes in tax laws in certain geographies was a prime inhibitor. Some investors also linked the decline in deal flows to their reaction to the market correction.

Read the entire report: TresVista Investor Confidence Index: U.S. Middle Market PE Half Yearly Report

Check out their webinar on secondaries:

Link: https://www.youtube.com/watch?v=vSqfn1pg-XY&list=PLGdZu5dpVzsEtW2c2AmDTTUGRnTrx7DZc&index=7

TresVista is a global enterprise offering a diversified portfolio of services that enables its clients to achieve resource optimization through leveraging an offshore capacity model. TresVista's services include investment diligence, industry research, valuation, fund administration, accounting, and data analytics. TresVista has 1,500 employees across offices in North America, Europe and Asia, providing high-caliber support and operating leverage to over 1,000 clients across geographies and asset classes, including asset managers, advisors, corporates, and entrepreneurs.

TresVista is 'Great Place to Work-Certified™'

To know more, please write to us at reachus@tresvista.com

Disclaimer: This document is provided for information purposes only. The information is believed to be reliable, but TresVista does not warrant its completeness or accuracy. It should not be used, relied upon, or treated as a substitute for any professional advice. Opinions, estimates, and assumptions constitute our judgment as of the date hereof and are subject to change without notice. TresVista may, at its absolute discretion and without any obligation to do so, update, amend or supplement this document. TresVista disclaims any and all liability arising from actions taken in response to this report. TresVista, its employees, and any persons associated with the preparation of this report are in no way responsible for any errors or omissions in the report resulting from any inaccuracy, misdescription or incompleteness of the content provided. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Additional information is available upon request. Images used in this document are for reference only and may not be reproduced, copied, transmitted or manipulated in any way.

© TresVista 2022