By Chris Zhang, CAIA, senior manager of a technology driven securities company based in Shanghai.

China onshore capital markets were one of the linchpins of China’s relations with the outside world. The belief that they would continue to open up helped to maintain links with Western financiers hoping to strike it rich. Even as relations between America and China soured during the Trump years, a craving for onshore securities took hold of many of the world’s biggest financial groups. As a trade war dampened global sentiment, regulators in Beijing began expediting long-promised reforms, eventually allowing foreign financial groups to wholly own their onshore businesses. In 2018 MSCI added Chinese shares to its flagship emerging-markets index. Other index inclusions followed, creating a flood of foreign capital into onshore Chinese securities. Between the start of 2017 and a peak at the end of 2021, foreign financial exposure to yuan-denominated assets more than tripled to RMB 10.8 trillion (approx. $ 1.62 trillion). This article will help you understand one of the major players in the Chinese capital market, China private offering fund.

1. Overview of China stock market

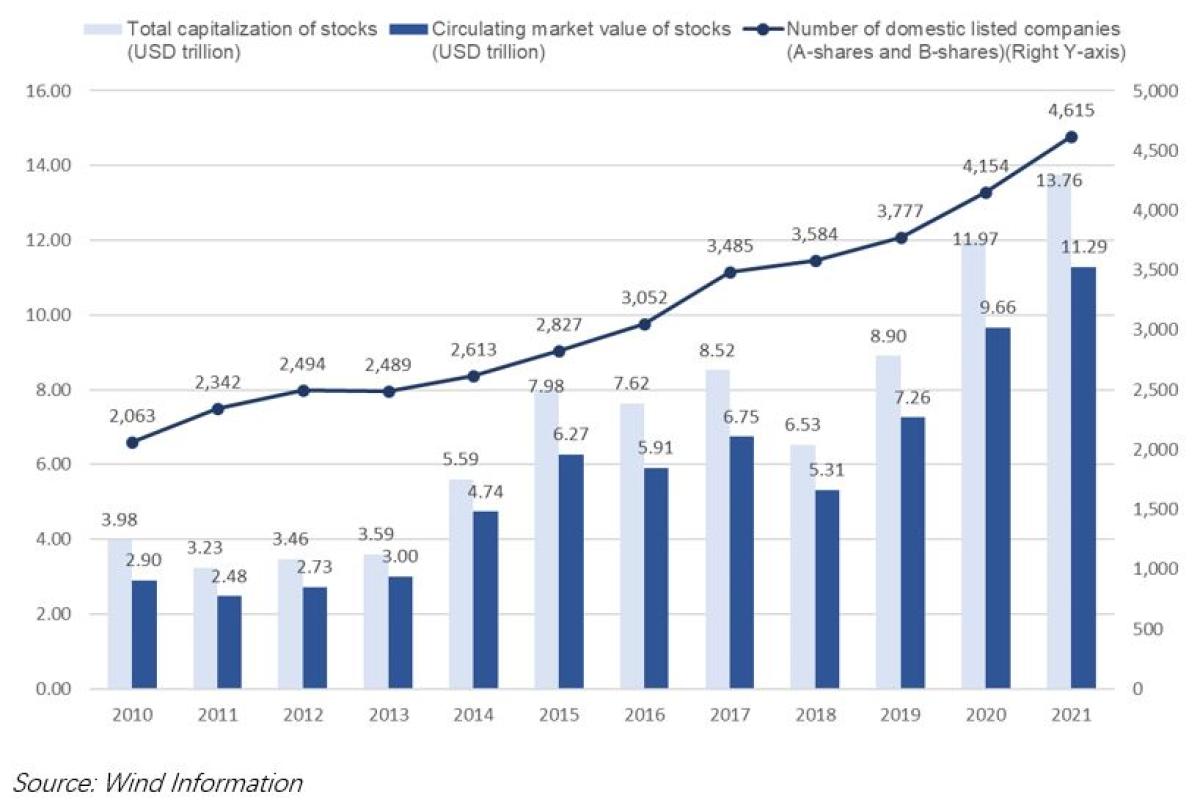

The number of listed companies in China has steadily increased since 2010 (see Figure 1). The number of A-share listed companies and B-share listed companies picked up from 2,063 in 2010 to 4,615 in 2021, with a CAGR of 7.59%. The market capitalization of stocks also maintained stable growth. As the end of 2021, the total market value of domestic stocks in China stood at RMB 91.61 trillion (approx. $ 13.76 trillion), with a CAGR of 11.92%. The total circulating market value was RMB 75.16 trillion (approx. $ 11.29trillion), with a CAGR of 13.15%.

Figure 1: Domestic Stock Listings in China from 2010 to 2021

In 2021, the A-share stock markets in Shanghai and Shenzhen maintained an overall upward trend despite a correction in the first quarter due to the pandemic. The SSE Composite Index, the SZSE Component Index and the GEM index closed at 3,639.78 points, 14,857.35 points and 3,322.67 at year end, representing year-on-year increases of 4.8%, 2.67 % and 12%, respectively. Among them, the CSI 1000 index performed the most outstanding, with annual rise of 20.52%, closely followed by the CSI 500 with annual rise of 15.58%. While the SSE 50 index and CSI 300 index, which are mainly large-cap stocks, went down (see Figure 2).

Figure 2: Performance of Major Market Indices in 2021

2. Brief and Regulations System of China Private Offering Funds

2.1 Brief on China Private Offering Funds

In China, private offering investment funds (hereinafter referred to as private offering funds), refers to the funds being established at territory of the People's Republic of China, raising capital in a non-public manner from accredited investors. The investment scope of private offering funds includes public stocks, private equity, bonds, futures, options, fund shares and other investment targets as agreed in the funds' agreement. Private offering funds are mainly classified into private offering funds in securities investment, private equity & venture capital funds and funds of funds. In China, private offering funds in securities investment are funds that invest primarily in securities publicly traded on stock exchanges or the interbank market, which are very similar to hedge funds.

2.2 Major Regulatory Authorities of Private Offering Funds

Private offering funds in China are subject to the administrative supervision and regulations outlines by the China Securities Regulatory Commission (CSRC), as well the membership-based self-discipline management of the Asset Management Association of China (AMAC).

The CSRC is a ministerial-level government body directly under the Chinese State Council. It supervises and regulates the Chinese securities market in accordance with applicable laws and regulations under the authorization of the State Council. While the CSRC does not examine or approve the registration of private offering funds, it does supervise the compliance of private offering fund operations on an ongoing basis.

The AMAC is a social organization registered with the Ministry of Civil Affairs of China as approved by the State Council in accordance with the Securities Investment Fund Law of the People’s Republic of China and the Administrative Regulations on the Registration of Social Organizations. The Securities Investment Fund Law and the Interim Measures for the Supervision and Administration of Private Funds stipulate that fund managers must apply and register with the AMAC. Private offering funds must apply to the AMAC for record-filing. The AMAC is responsible for the examination and approval of the registration of fund managers and products. However, it neither constitutes the recognition of investment ability or continuous compliance of the fund managers, nor serves as a guarantee for the safety of the fund’s asset.

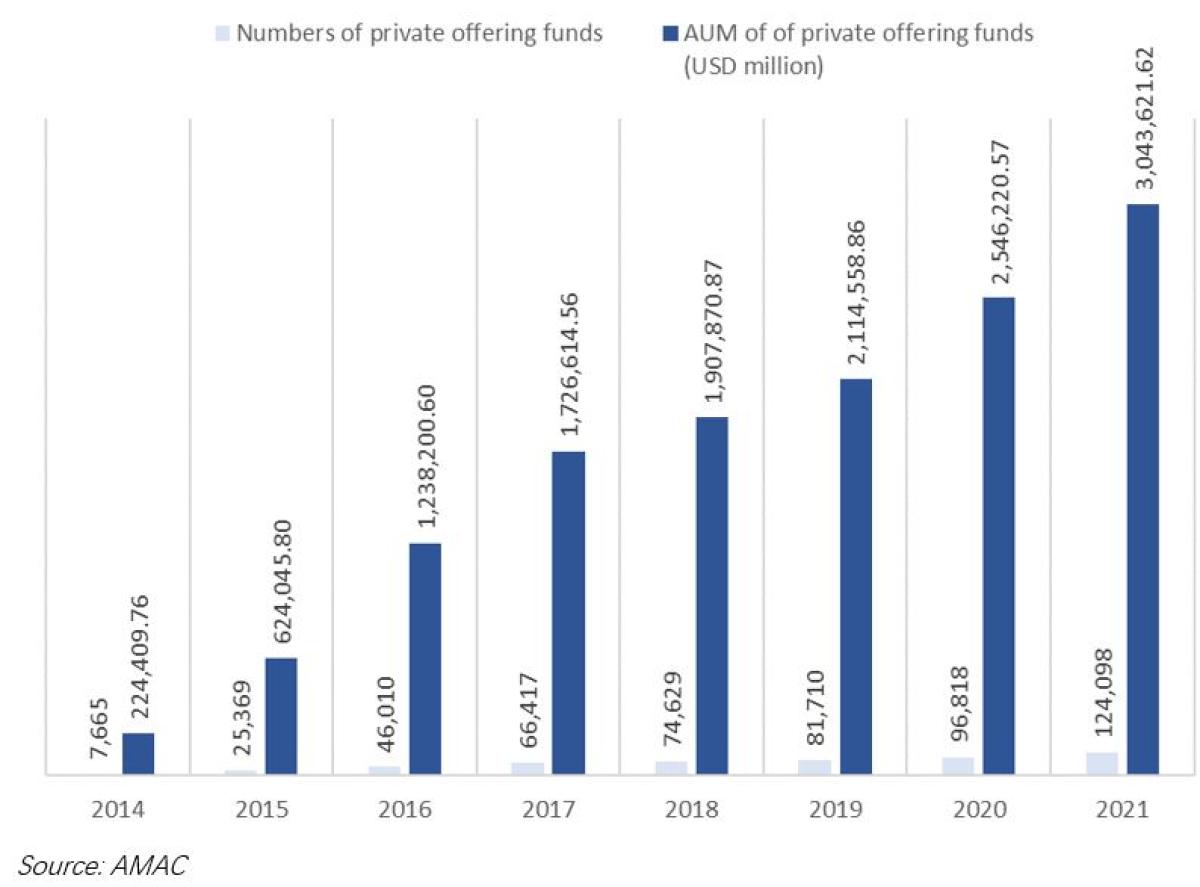

Since accredited investors are mostly institutional investors or high net worth individuals, who are strictly subject to the qualified investor management system and have a strong risk tolerance,the private offering funds sector in China has experienced rapid development in recent years (see Figure 3).

Figure 3: Development of Private Offering Funds in China in Recent Years

3. Overview of China Private Offering Funds in 2021

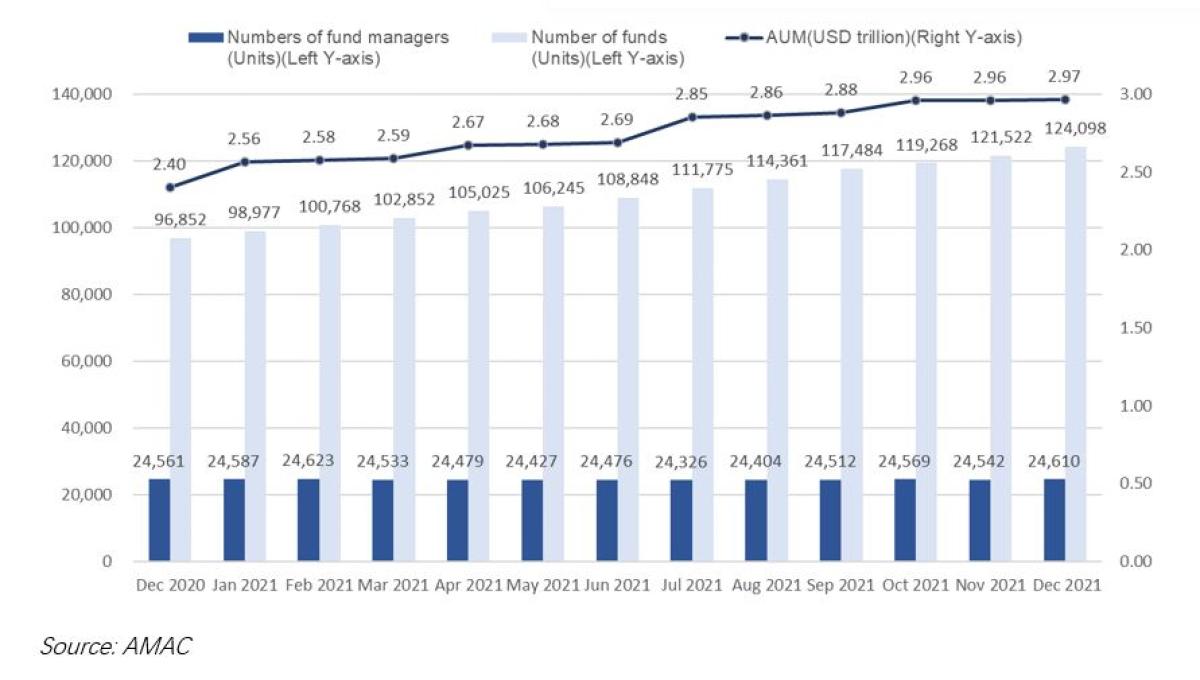

By the end of 2021, there were 24,610 existing private offering fund managers registered with the AMAC, an increase of 49 from end of 2020.There were 124,098 existing private offering funds registered with the AMAC, increased by 27,246 from end of 2020; asset under management was RMB 19.76 trillion (approx. $ 2.96 trillion), increase RMB 3.79 trillion (approx. $ 560 billion) from end of 2020 (see Figure 4).

Figure 4: Change of Private Offering Fund Managers in 2021

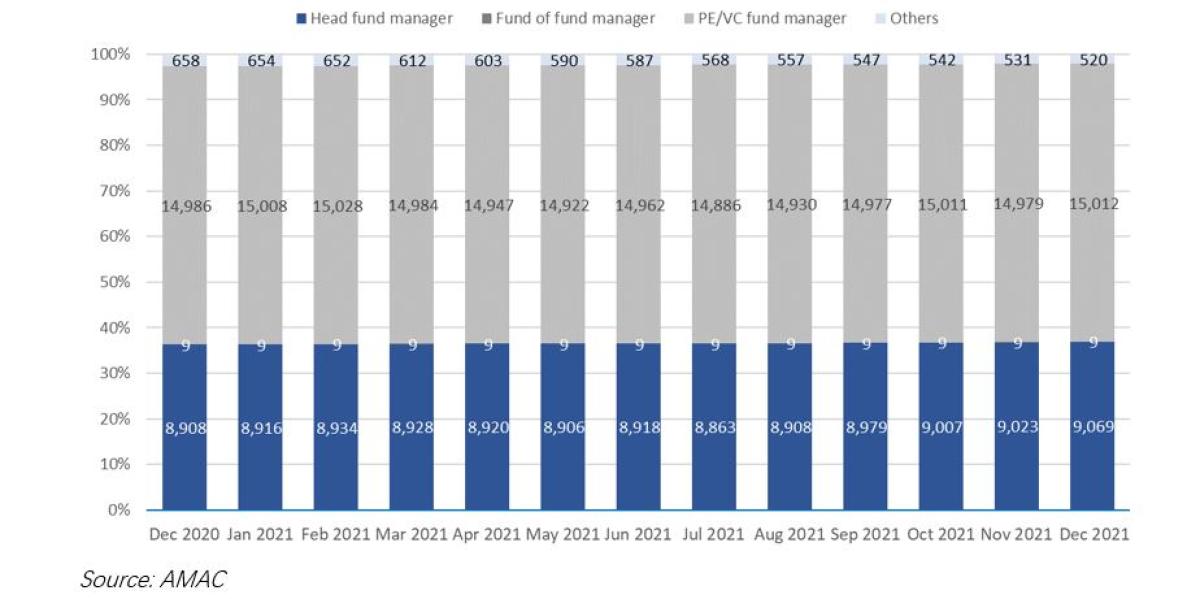

Among the 24,610 private offering fund managers, there were 9,069 existing registered hedge funds managers, 15,012 existing registered fund managers in private equity and venture capital, 9 existing registered funds of funds managers (see Figure 5).

Figure 5: Change of Private Offering Fund Managers in 2021

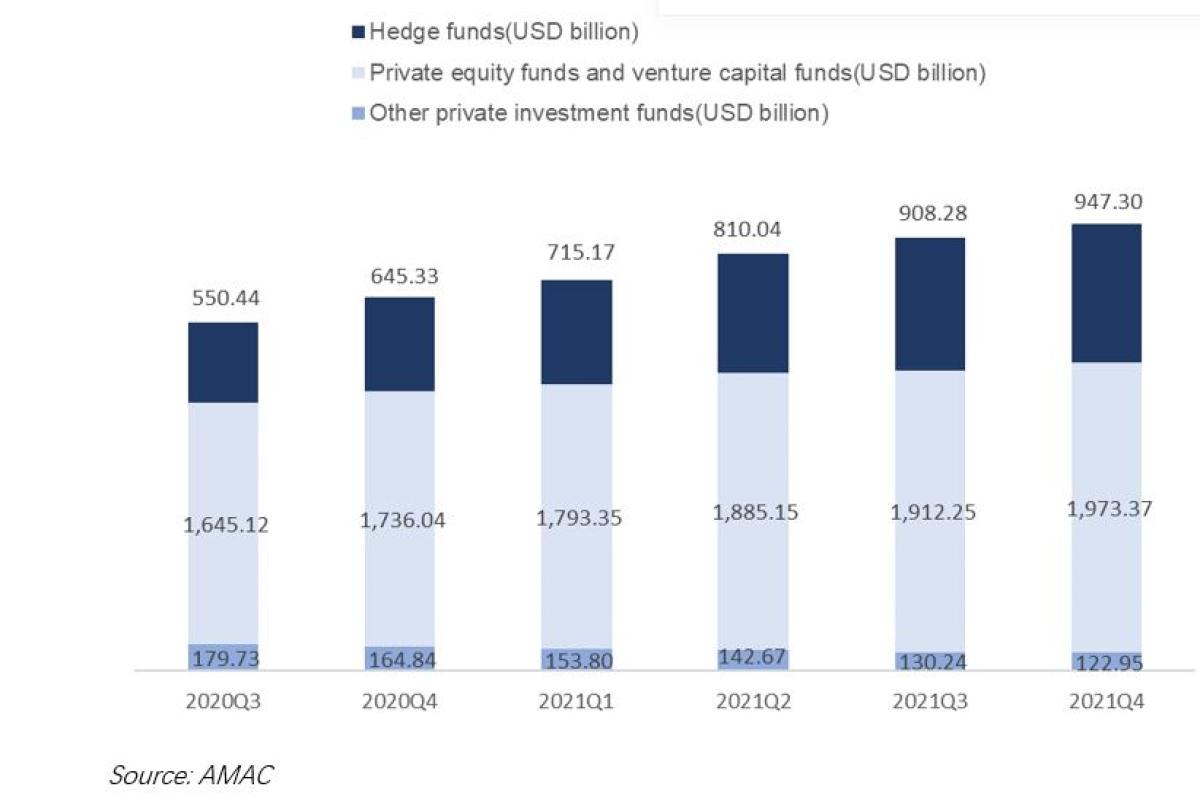

By the end of 2021, private equity investment funds and venture capital funds account for a large proportion of China’s private offering fund market. Hedge funds are also showing strong momentum and developing rapidly, with their share in the private offering funds market steadily on the rise (see Figure 6).

Figure 6: Change of AUM by Mangers’ Type

4. Overview of 2021 China Hedge Funds

4.1 Development of China Hedge Funds

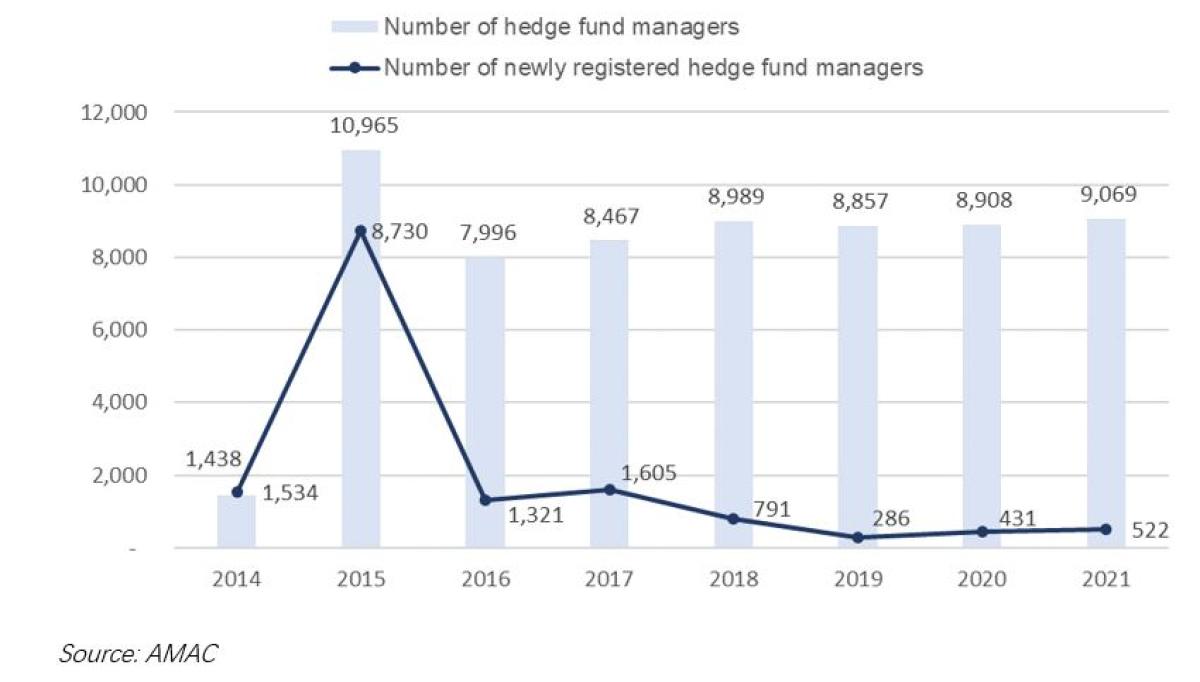

Since 2014, China’s hedge funds market is advancing rapidly and steadily. The number of hedge fund managers in China stabilized at around 8,900 over the past four years, with approximately 400 new managers registered each year. The funds and capital raised by hedge fund managers in China have continued to grow, especially in the past two years during which the market size increased by over 70% (see Figure 7).

Figure 7: Change of Hedge Fund Managers in China

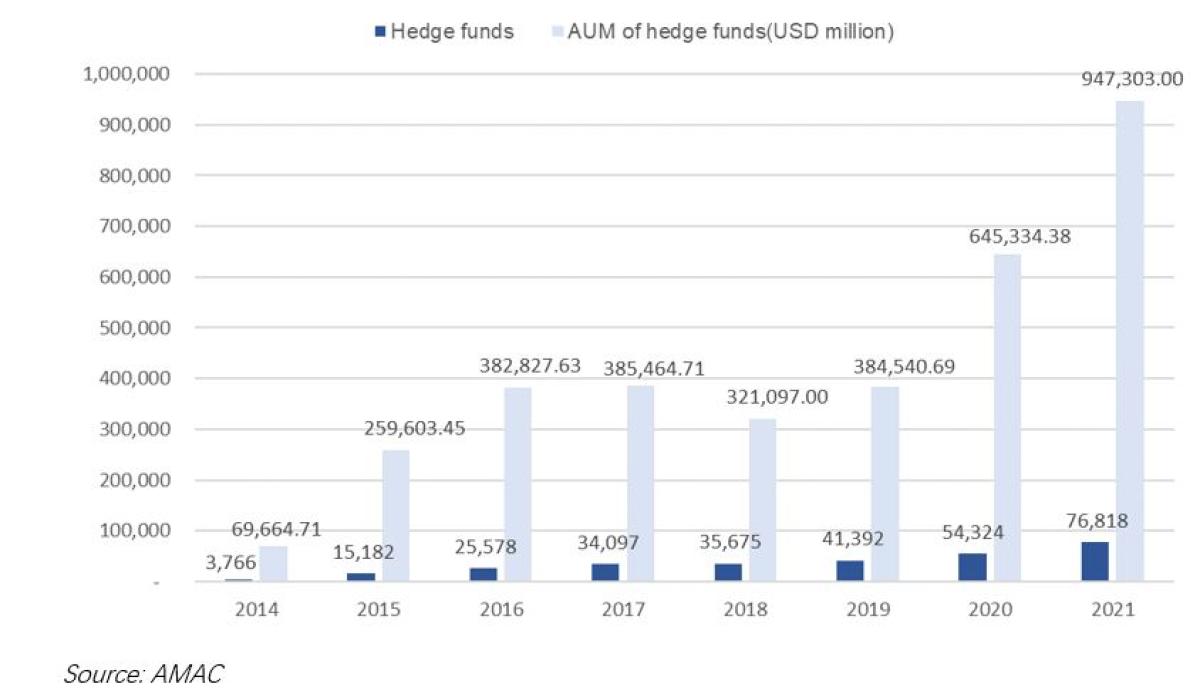

As of end 2021, there were over 70,000 hedge funds in China amounting to over RMB 6 trillion (approx. $ 900 billion) (see Figure 8).

Figure 8: Development of Hedge Funds

4.2 Trading Venue

Unlike private equity funds and venture capital funds, which focus on the primary market, the targets of securities investment funds are based in the secondary market. According to the Securities Investment Fund Law of the People‘s Republic of China promulgated in 2015, hedge funds are supposed to be engaged in securities investment transactions in China’s different exchanges. This includes trading of publicly-offered stocks of limited liability companies, bonds, funds, and other securities and their derivatives as prescribed by the CSRC. The scope of investment can be divided into stock trading, bond trading and futures trading. All transactions must be in compliance with the requirements of different exchanges (see Table 1).

4.3 Major Strategies and Performance in 2021

In China hedge funds can be classified into the following investment strategies: stock-discretionary (equities long), fixed-income, multi-strategy, Fund of Fund, market neutral, macro strategy, managed future, event-driven, and quantitative strategy.

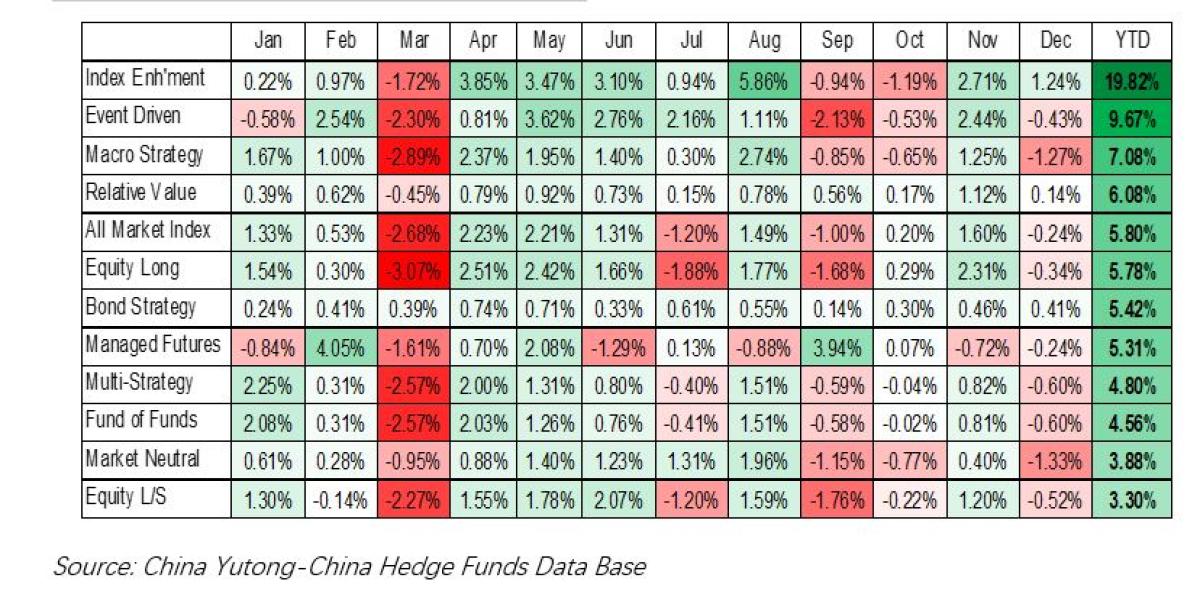

In terms of return, the performance varied in different months in 2021. Overall, the index enhancement strategy performed the best, with an annual return of 19.82%, followed by the event -driven strategy with 9.67% and the macro strategy with 7.08% (see Table 2).

Table 2: Returns by Strategies in 2021

5. Overview of China Quantitative Hedge Funds

Since the emergence of quantitative hedge funds in the Chinese market in 2015, the industry as a whole has seen a significant boost. The main improvement is reflected in: 1. the AUM and the trading volume of quantitative hedge funds has increased; 2. the number of quantitative hedge fund managers has increased and the concentration of the industry has increased; 3. the quantitative strategies have been updated and iterated and the profitability and risk control ability has been enhanced.

According to CITIC Securities' estimation, in 2021, there were 645 quantitative hedge fund managers raising capital for their funds, accounting for 7.79% of the whole industry. The AUM of quantitative hedge funds is nearly RMB 1.61 trillion (approx. $ 241.74 billion).

Figure 9: Discretionary vs. Quantitative Hedge Funds

According to estimation, quantitative trading daily volume in China stock market averages around RMB 200 billion (approx. $ 30.03 billion), accounting for about 20% of the overall trading volume. In 2021, the number of quantitative hedge funds with AUM over RMB 10 billion (approx. $ 1.50 billion) jumped to 30. Their combined AUM was estimated to be about RMB 480 billion (approx. $ 72.72 billion), accounting for about 33.57% of the overall market. Compared with 2020, the degree of concentration increased.

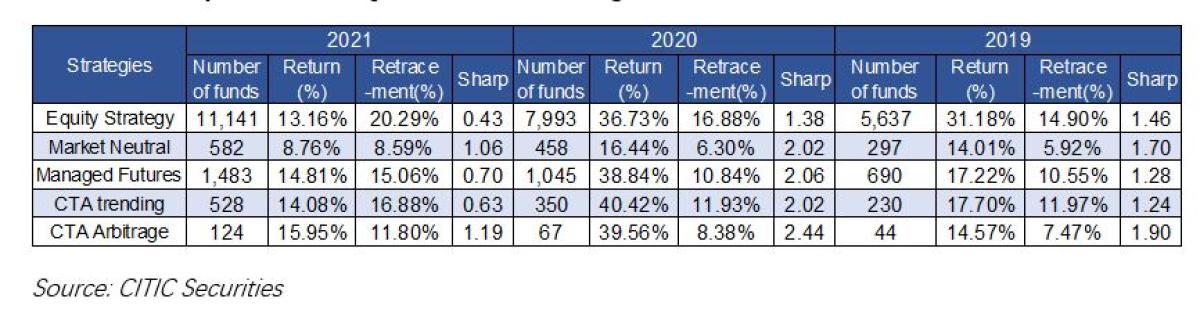

Quantitative hedge funds have developed a variety of strategies such as market neutral, index enhancement, CTA, quantitative stock picking, equities long-short, etc. and all have achieved notable performance in 2021(see Table 3).

Table 3: Comparation of Quantitative Strategies from 2019 to 2021

6. Summary and Outlook

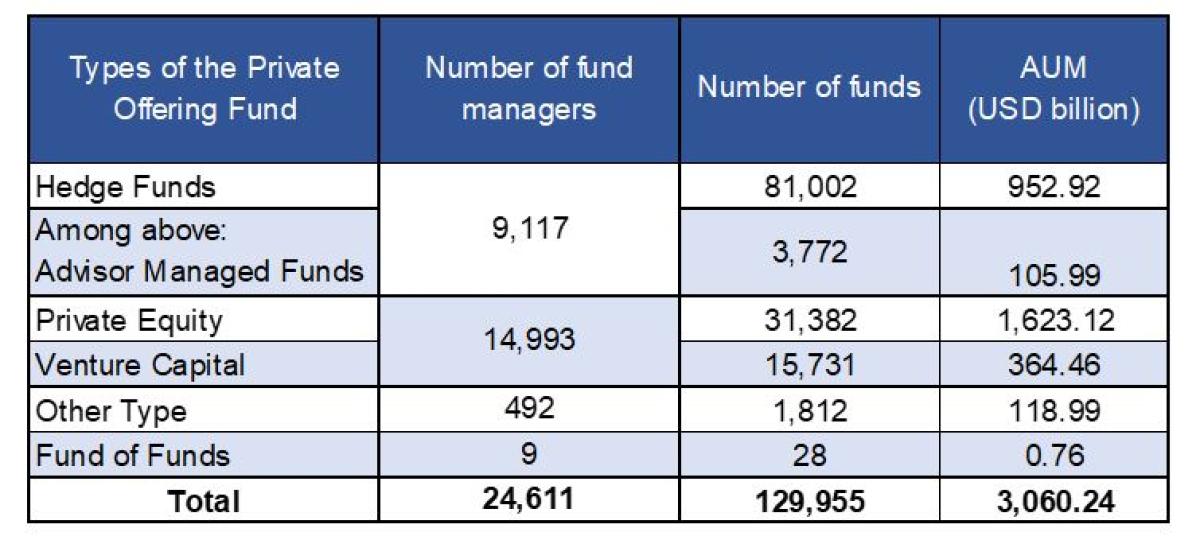

As of the end of March 2022, there were 24,611 existing private offering fund managers and 129,955 existing private offering funds registered with the AMAC. asset under management is RMB 20.38 trillion (approx. $ 3.06 trillion).

Many investors see 2022 as a bellwether year for the direction of policy. The optimistic outlook is that this gloomy period of ideology, policy missteps and slow growth is part of the preparation for the party congress in the autumn. We will continue to watch the performance of hedge funds in China.

About the Author:

Chris Zhang, CAIA is the senior manager of a technology driven securities company based in Shanghai. Chris has an MBA degree from Rutgers business school. After graduation, he worked as an auditor in an accounting firm based in US, auditing multiple onshore and offshore hedge funds from 2007-2010.

Since returning to China in 2010, Chris has been working for several different companies in financial service industry. During his working experience in China capital market, Chris is skilled in asset management and investment banking. For the past three years, he has been witnessing the development of the Chinese private offering funds industry and keeping writing reports on the industry. Currently for China Fortune Securities Co., Ltd, focusing on business development with high frequency trading firms and quantitative hedge funds.