By Riz Hussain, Leveraged Finance Investment Strategist at Lord, Abbett & Co. LLC.

Here’s why convertibles may represent an attractive approach for investors who have previously focused on traditional bonds.

The ongoing debates around the probability of a U.S. recession, the depth and duration of any slowdown to come, and what outcomes might already be “priced in” across assets have all been headwinds to risk markets. Meanwhile, a market-unfriendly U.S. inflation report on June 10 further added rationale for a more hawkish U.S. Federal Reserve (Fed).

Investor conviction remains low, and all the factors mentioned above have manifested themselves in choppy price action across credit and equities over the past several weeks—just as we head into the summer, a season of historically lower liquidity in the markets.

As a ‘hybrid’ asset class, the convertible bond market serves as a meeting place for addressing the range of these investor concerns across the corporate capital structure. In this Market View, we revisit the case for the convertible bond asset class, in the context of current market conditions.

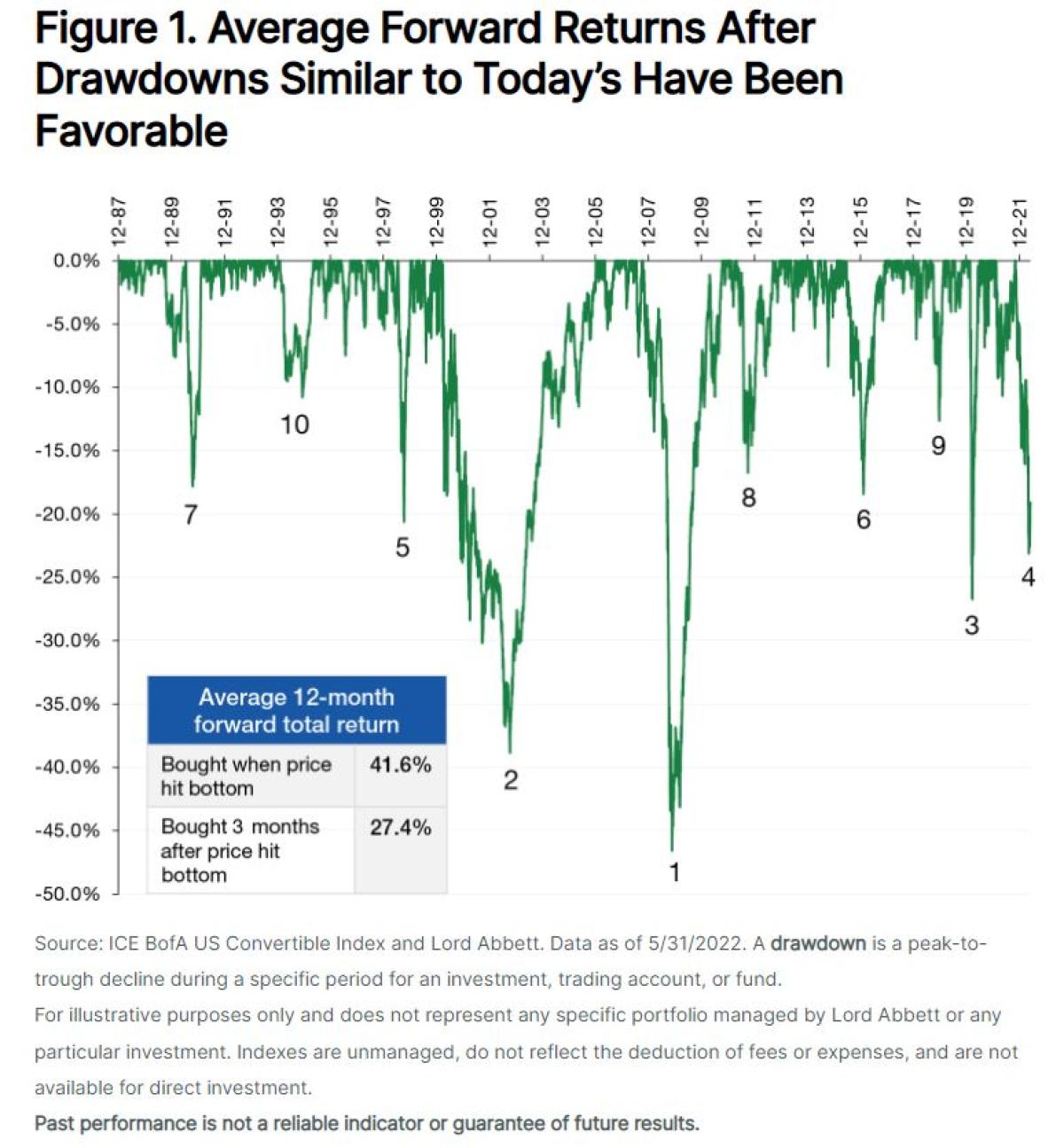

The Current Drawdown Ranks Among the Largest of the Last 35 years…

Risk assets of all stripes have been under pressure for much of the year as the Fed looks to rein in inflation by tightening financial conditions. In Figure 1, we put the current drawdown in the convertible bond market through the end of May into longer-term perspective. Specifically, the current move lower that started in late 2021 has resulted in the fourth-largest drawdown over the studied period dating back to 1987. Without taking a high-conviction view on the timing, shape, and pace of any rebound to come, we can simply note that the average 12-month forward returns after similar episodes of large drawdowns have been quite favorable, even if an investor was late to catch the initial turn higher. While the year-to-date return of the convertible index is roughly in line with the broad S&P 500® Index, the asset class has more exposure to small and mid-cap growth companies, and so historically has been more correlated with the Russell Midcap® Growth index. The Bloomberg U.S. Convertibles Index has provided the downside protection versus its underlying equity exposure, as it typically has, with a return of −16.9% versus the -28.9% decline of the closely related Russell Midcap® Growth Index.

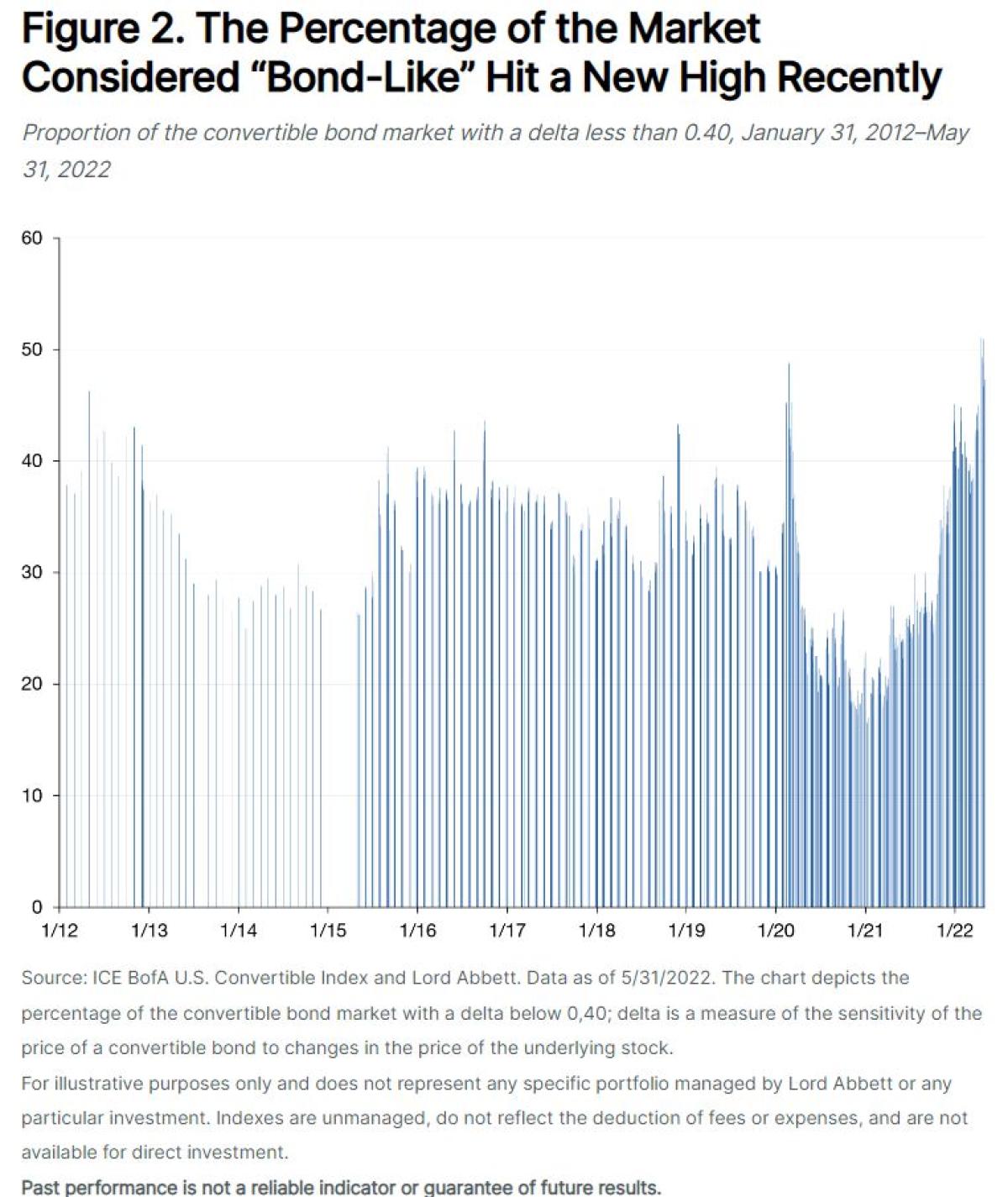

…and May Have Shaped Today’s “Bond-Like” Asset Class

One of the main defensive draws of the convertible bond market historically has been the rising “bond-like” nature of the security that results from declining sensitivity to the underlying equity—should the stock price move further away from the conversion price of the bond. This varying sensitivity of a convertible bond’s price to the underlying equity is known as the bond’s delta. While convertible securities with a high delta are considered “equity-sensitive,” market participants generally consider a convertible bond with a delta below 0.40 to be “bond-like” and thought of as more of a “yield instrument.” In Figure 2, we note that the percentage of the ICE BofA U.S. Convertible Bond Index that fits this characterization recently topped 50%, superseding the breadth of this “yield-instrument” classification seen during the worst of the March 2020 dislocation.

This resulting nature of the convertible bond market today makes comparisons to the traditional credit markets much more applicable, in our view. We believe the bond-like character of the opportunity today can appeal to traditional credit investors who may be searching for any positive convexity to come, beyond what could be derived from traditional credit instruments. In traditional credit, a further rise in benchmark yields would provide a headwind to prospective total returns, even should credit conditions ease and result in spread tightening. And related to our discussion around forward returns post large drawdowns, our prior work referenced above has shown that forward returns are positively correlated with lower starting points of broad market delta that result from a market decline. Further, today the asset class has less equity sensitivity going forward given the current delta, a reality that may appeal to those investors concerned about the potential for a further pullback in equities from here.

Comparing Convertibles to Traditional Credit

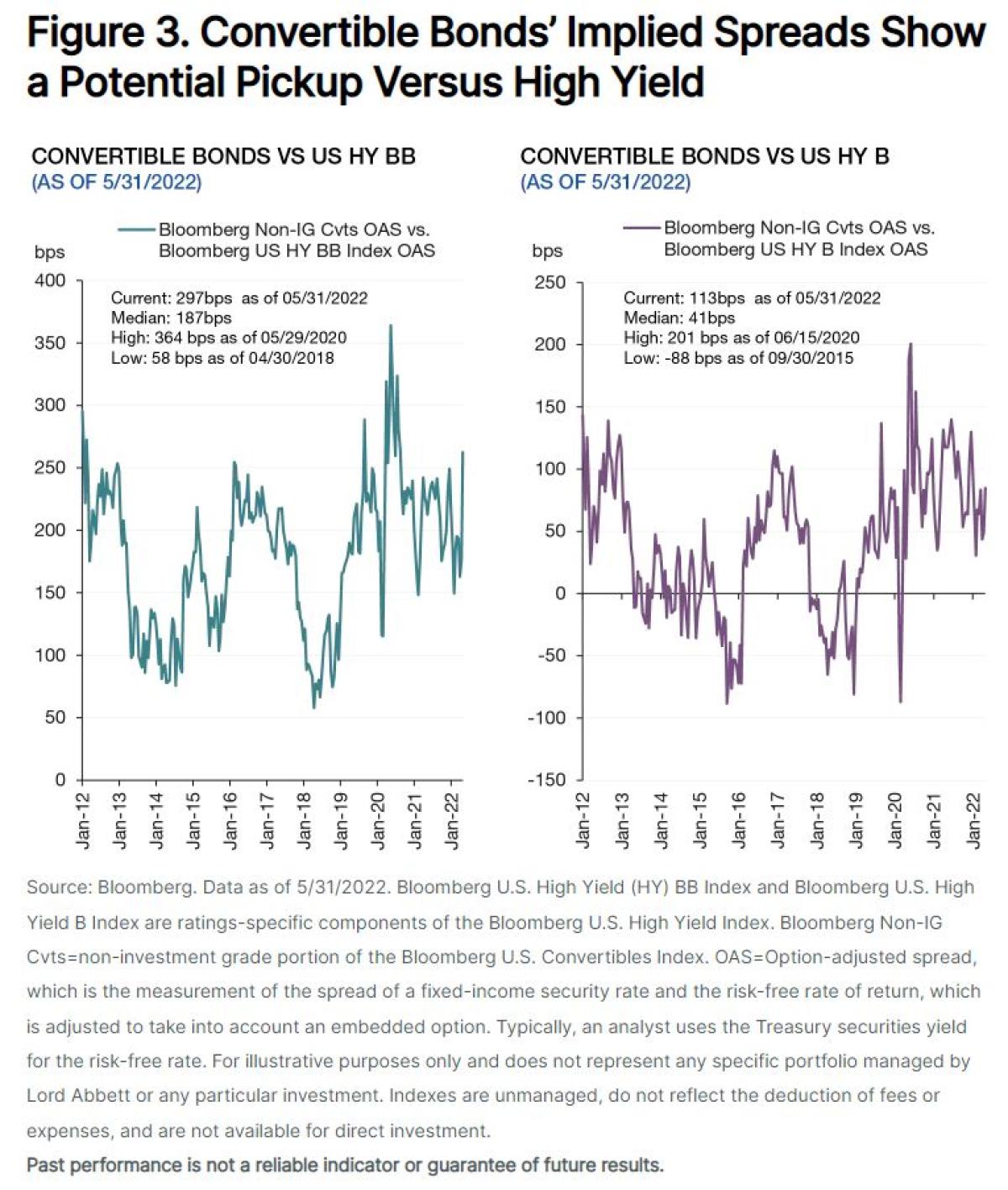

At their core, convertible bonds can simply be considered a package of a corporate bond with a call option on the underlying equity of the issuer. However, with the move lower in the broader equity market, the value of the call option (which may have fallen ‘out of the money’) in many convertible bonds has fallen as a proportion of the overall value of the theoretical price of the bond. We can calculate an implied credit spread of the bond based on certain volatility assumptions for the call option, as well as the maturity and current price of the convertible bond. Courtesy of Barclays, in Figure 3, we show the implied option-adjusted spread of the convertible bond market versus both the ’B’- and ‘BB’-rated segments of the U.S. high yield market.

While certainly not showing the same spread gain out of high yield we saw in early 2020, the pickup remains attractive, in our view. We have additional comfort in knowing that the default rate in the convertible bond market has generally been at or below that of the U.S. high yield market. Over the period from Q4 2017 through Q1 2022, the trailing 12-month (TTM) default rate in the convertible bond market has averaged 2.45%, versus 3.79% for the U.S. high yield market, based on ICE BofA index data. And we further note that this TTM default rate in convertible bonds has been lower than that of high yield in nearly 80% of those rolling periods. Finally, we note that convertible bonds can complement an allocation to traditional credit given the asset’s skew toward growth and innovation over value and cyclicals prevalent in the U.S. high yield market, for example.

Key Takeaways

If the hotter-than-expected May inflation report is any indication, investors may adopt a more defensive posture as we await the outcome of the Fed’s campaign to tame inflation by tightening financial conditions without inducing recession. In the meantime, we believe Lord Abbett’s strength in fundamental research across the capital structure, including deep resources in leveraged credit research, could potentially benefit investors given the bond-like nature of the convertible bond market today. On the flip side, periods when macro growth is scarce have historically seen growth-oriented equity strategies outperform value. That environment could also present a positive backdrop for the underlying equities of many of the innovative convertible bond issuers we have seen over the past several years. Either way, Lord Abbett’s convertible bonds team has a long history of successful active management through a variety of market and economic conditions and will bring that experience to bear in today’s challenging environment.

About the Author:

Riz Hussain helps drive the development and communication of information regarding the firm’s investment capabilities, strategies and market outlook to clients and prospects across the international market. Mr. Hussain also participates in product development and actively monitors industry activity to ensure Lord Abbett continues to offer competitive solutions in the marketplace to meet investor needs. Mr. Hussain joined Lord Abbett in 2019. His previous experience includes serving as Leveraged Finance Strategist at Barclay's and various roles at Morgan Stanley including U.S. Credit Trading Desk Analyst and U.S. Credit Strategist. He has worked in the financial services industry since 1994. He earned a BS in mechanical engineering from Cornell University and an MBA from Columbia Business School at Columbia University.