By Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director and Head of UniFi by CAIA™ at CAIA Association.

The analogy of building a house is not too far off from constructing a diversified portfolio. If asset allocation is like deciding the location of your new home, there’s many more steps to take before your portfolio is move-in ready. In Part I of this three-part series from Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director, Head of UniFi by CAIA™ at CAIA Association, he walked through some basic frameworks for advisors approaching portfolio construction with alternative investments. In Part II, he delved into what next steps define all that is available to clients after the investment philosophy has been determined through the investment policy statement and policy portfolio. The final installment, Part III, continues at the point when the policy portfolio has been constructed and the liquidity profile has been explored.

Once the policy portfolio has been constructed, and the liquidity profile has been explored, the investment opportunities should reveal themselves. The art of portfolio construction can now begin!

For an advisor there are five key considerations an advisor should make when building out an alternative investment allocation:

- The Role of the Strategy In the Portfolio

- Where the Strategy Resides

- Sub-Strategy Diversification

- J-Curve and Vintage Year Diversification

- Post-Commitment Strategies

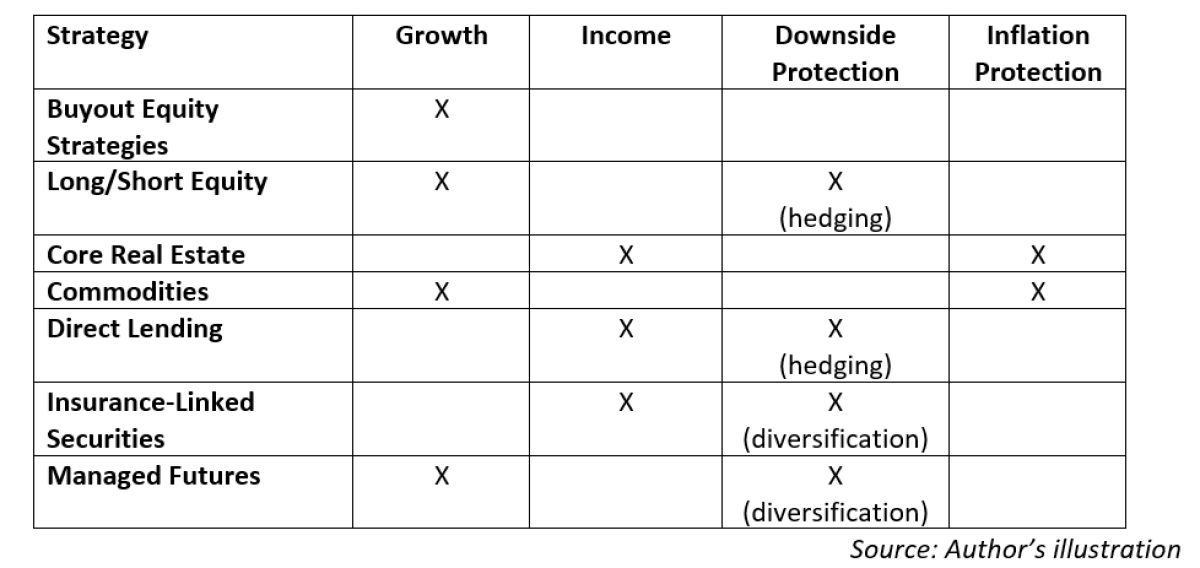

Consideration #1: Role in the Portfolio

The first, and most important, consideration an advisor should make is what role the investment strategy will play in the client’s portfolio. “Alternatives” are a convenient catch-all, but under the surface, some strategies act and behave differently. While some strategies will have overlapping characteristics, we can loosely categorize every single one into four primary roles:

- Growth: plays “offense” in the portfolio and meaningfully increase the portfolio’s value over time

- Income: generates an attractive current income stream

- Downside Protection: protects the portfolio during difficult markets, either through one of the following:

- Hedging - a true hedge offers positive returns in a bear market; potentially negative correlation and negative beta.

- Diversification - positive or differentiated performance through low to negative correlation to other assets

- Inflation Protection: protects the portfolio from rising or surprise inflation, either through price appreciation or inflation-linked cash flows

Each of these roles are not mutually exclusive – in fact, many strategies fit multiple roles in the portfolio, so it’s up to the advisor to select the most appropriate ones. Let’s show some examples in Table 1.

Table 1: Examples of Alternatives Role in the Portfolio

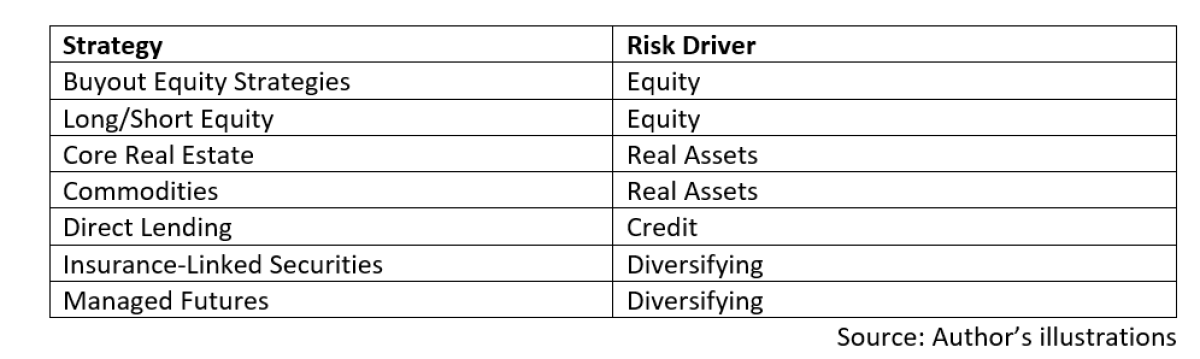

Consideration #2: Where Does It Go? Risk-Based Framework

The second consideration is where these alternative strategies reside within the broader portfolio. Referencing back to the earlier section, my view is that a risk-based exposure makes the most sense rather than creating a “bucket to fill.” As we just saw, that “bucket” is heterogeneous.

If we take a risk-based framework, we should instead look at the primary risk and return driver of each strategy. In other words, when examining each strategy, we should ask, “what is the leading risk that drives this return?”

Again, the categorizations will vary, but for simplicity, we can group things into four primary risk drivers for most strategies:

- Equity – strategies where the primary driver of return is equity risk premia

- Credit – strategies where the primary driver of return is credit risk premia

- Real Assets – strategies with assets that derive their value from their physical properties

- Diversifying Strategies – strategies with assets that don’t have direct exposure to the other three risk drivers, where the manager tactically borrows from the other three risk drivers, or where performance is driven primarily by the manager’s skill

Let’s look at some examples to illustrate this point. Like Consideration #1, some strategies will have overlapping exposures, but for simplicity, I’ve categorized them into their “primary” grouping in Table 2.

Table 2: Examples of Primary Risk Drivers in Alternative Investments

The result is this: the underlying risk driver may be the same, but the role it plays is different. Think of the “role” as the goal or outcome and the risk driver as the tools at the advisor’s disposal to achieve them.

Once the risk driver and the roles are known, utilizing a risk-based framework provides a bit more clarity for implementation. Equity strategies are combined with other equity assets; credit strategies are combined with other credit assets, and so on. Of course, this is an oversimplification – as we covered earlier, these strategies are complex, illiquid, and carry different considerations than trying to “factor-ize” them will capture, but it can be a helpful starting point, both for the advisor and for clients.

This combination is the sweet spot between the top-down and bottom-up decision-making processes – it recognizes similarities to other asset classes, like the top-down approach favors, but also acknowledges that not all strategies are created equal, like the bottom-up approach favors.

Consideration #3: Sub-Strategy Diversification

An important consideration in portfolio construction is sub-strategy diversification. In public, long-only traditional investments, there’s greater visibility into each strategy's components, allowing an advisor to build a diversified allocation within each asset class. In alternative investments, there is no real standardized equivalent to the Morningstar Stylebox, so advisors will be required to focus on diversifying by what they can observe. Some of these characteristics might include style, sector, geography, or capital structure. Let’s use a few examples

Private Equity

“Private equity” is a broad categorization for an industry with so many kinds of strategies. When allocating to private equity strategies, an advisor should consider the following:

- Stage: Private equity investments can be made at different stages of a company's life cycle, such as start-up, expansion, or mature stages.

- Industry: Some GPs are sector specialists (e.g., technology or health care) while others are multi-sector.

- Geography: Like public markets, investing in private equity opportunities in different regions or countries can also help diversify the portfolio.

- Style: Private equity investments can take various forms, such as venture capital, growth capital, or buyouts. Each of which carries very different risk-return profiles.

- Strategy: Each strategy can target value creation from different sources. For example, distressed managers target underperforming businesses and create value via turning around and stabilizing the business. Another strategy is industry roll-up/consolidation, in which a manager buys a business and uses that company to engage in M&A purchasing smaller companies, benefitting from efficiencies of scale, and growing operating leverage.

Private Debt

Private debt strategies are similar in their diversity in that there are many strategies within the broader complex. In addition to some of the characteristics of private equity, private debt investors should also include:

- Capital structure: Some debt strategies focus on senior secured loans, while others focus on subordinated/unsecured loans.

- Rate Structure: Some private loans offer fixed rates, while others offer floating rates. Additionally, some loans incorporate PIK yields and other sources of return, such as origination fees.

- Term/Maturity: Some debt strategies focus on shorter-term holding periods (2-3 years) while others may anticipate a loan lasting 5-7 years or in the case of real estate loans 15-25 years.

Real Estate

Given that real estate’s value is driven so much by physical characteristics, investors in real estate should consider the following:

- Style: Like private equity, real estate strategies tend to focus on certain stages and styles of properties, such as core, core plus, value-add, and opportunistic.

- Geography and Market Type: The opportunity for higher returns can also be driven by the type of markets in which real estate properties exist. Primary, secondary, and tertiary markets have varying degrees of affordability (and therefore rental income) and growth opportunities

- Property Type: the dynamics between property types vary greatly. The major types include office, retail, industrial, multi-family, and hotels. Not surprisingly the dynamics for hotels investments may differ greatly from an industrial property, or trophy office property (among others).

The unique characteristics of private alternative investment categories go beyond the three examples listed above. This exercise aims to illustrate that it’s not always enough to have exposure to an “asset class.” Thoughtfully combining strategies within the same category can lead to better outcomes. This is an exercise many advisors already pursue in traditional markets – total public equity exposure is often broken up into style, factor, size, and geographical exposures – the same should be done for alternative investments.

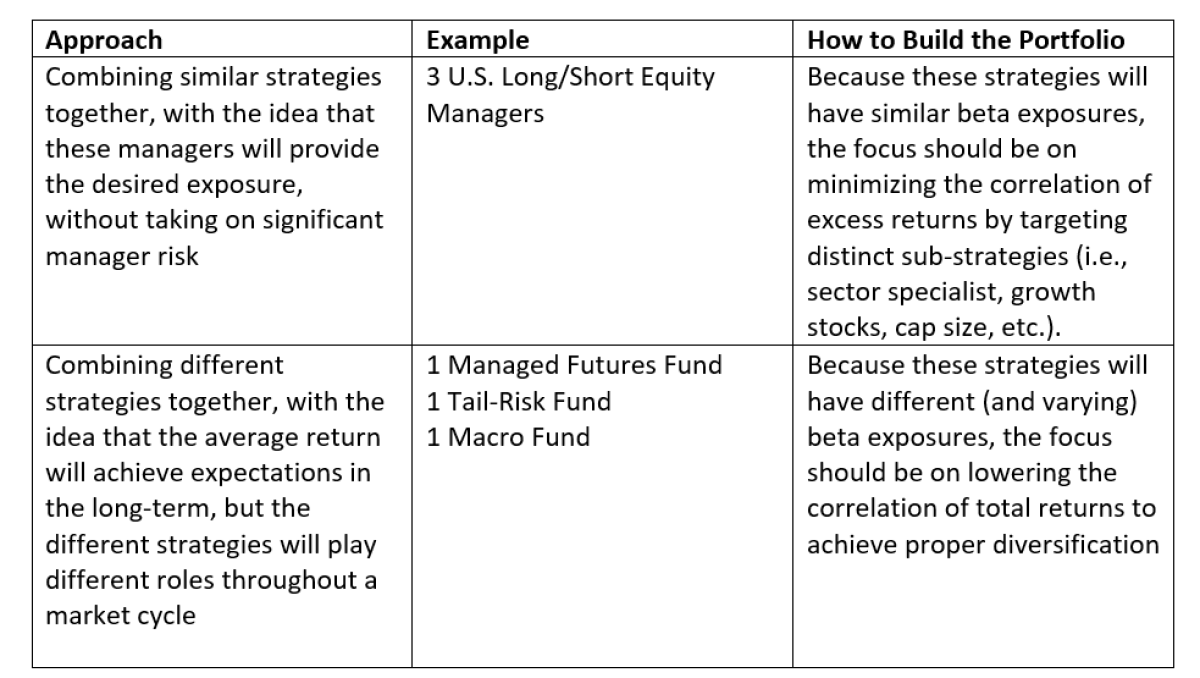

The challenge comes with more flexible and tactical strategies like many hedge funds and liquid alternative mutual funds pursue. For example, managed futures and macro managers may be labeled similarly but pursue their strategies very differently. The key to portfolio construction with these strategies is to combine different managers enough to avoid concentrating risks with one, while still benefiting from the skill the manager adds to the overall portfolio. This can be done doing either or both of the following, as shown in Table 4.

Table 4: Combining Flexible Strategies

Consideration #4: J-Curve and Vintage Year Diversification

When investing in private markets using drawdown fund structures, the vintage year of a private fund can be a very important factor that determines its future performance. For example, a fund with vintage year one or two years before an economic downturn may see lower returns, while one a year or two after may see higher returns.

Unlike public markets, it’s difficult to be tactical in private markets, so building a long-term portfolio that invests across vintage years will lead to performance that’s more representative of the broader asset classes. Predicting vintage years is a near impossible task. The best approach, if available to the client, is to consistently allocate each year. Going from 0% exposure to the target exposure will take time (perhaps years). There are strategies to back-fill and up the exposure more quickly, however overcommitting in year 1 is a risk to not be ignored. This is often referred to as ‘pin risk’.

While you can build a diversified vintage year program with new commitments, you can also allocate to historical vintage years using the secondary market. In fact, using secondary funds can be a quick way to create a diversified portfolio of vintage years.

Consideration #5: Cash Flow Management and Time Horizons

Even after you’ve determined your client’s asset allocation and have a plan for constructing a portfolio that meets their objectives, the advisor still must manage cash flow. Unlike open-end funds or ETFs, which can be purchased and redeemed daily, many alternative investment strategies use less liquid structures. Therefore, a meaningful and diversified allocation will take time to build and will be more challenging to unwind.

With drawdown fund structures, there is time lag between capital commitments and capital calls; an advisor should ensure they have a strong cash management program for their clients. It could be months between the time you commit capital to a fund and when that capital is first called. When a fund manager calls the capital, you may have as little 10 days to provide them with your commitment. This requires you to balance two tasks: make sure the money is accessible when called, but also figure out what to do with it until it’s called.

Once invested, some strategies may lock up capital for as much as 10-15 years, which means the advisor needs to ensure the total portfolio's liquidity profile meets the client's needs. For example, retirees needing regular distributions may not be able to invest a substantial portion into venture capital all at once. The portfolio’s distributions would only be able to come from other assets, creating an unwanted concentration in the asset class.

Beyond portfolio construction decisions, one way to manage cash flow for clients is to combine multiple fund vehicles. This approach would very explicitly mitigate a cash drag on the front end of the investment period and allow periodic redemptions and rebalancing on the back end. All of this while maintaining long-term exposure to a particular strategy or asset class.

Conclusion

Like building a house, portfolio construction starts with a solid foundation. From there, the design is up to the preferences of the buyer…in this case, your client.

Constructing a portfolio of alternative investments shouldn’t be taken lightly simply because the data isn’t as rampant as public markets. Each category of strategies carry overlapping characteristics and economic exposures, but each individual strategy pursues their objectives differently. By combining multiple managers within each category, advisors can layer on different exposures appropriately and mitigate manager-specific risks.

About the Author:

Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP is managing director and head of UniFi by CAIA™ at CAIA Association. He earned a BS with distinction in Finance and a Master of Finance from Penn State University. Contact him at afilbeck@caia.org.