By Will Thomson, Founder and Managing Partner of Massif Capital.

Real assets businesses are generally cyclical. In our view, this cyclicality lends itself to investing on both sides of the business cycle — and to the long/short approach we employ in our global real assets strategy.

While many real assets investment portfolios are long-only, I believe this approach limits a portfolio’s potential. It eliminates the opportunity to a) make money in real assets stocks when they decline and b) offset losses in a portfolio’s long positions.

Massif Capital’s long/short equity approach offers us opportunities to engage in different ways throughout the business cycle.

Why Our Strategy Includes Shorts

As a portfolio manager, my first job is to avoid losing money. My second job is to make money. Allocating a portion of portfolio assets to short positions aligns primarily with my first job — capital preservation. It’s a method of reducing risk. Specifically, our portfolio’s short book aims to: 1) neutralize some of the counterproductive factor exposure embedded in our long book and 2) contribute an annual single-digit return of roughly 5%-7% to the portfolio. This doesn’t suggest that we pick companies to short based on factors; we don’t.

Our cumulative short positions generate a net exposure that flexes between 0% and 50% depending on the opportunity set and market dynamics.

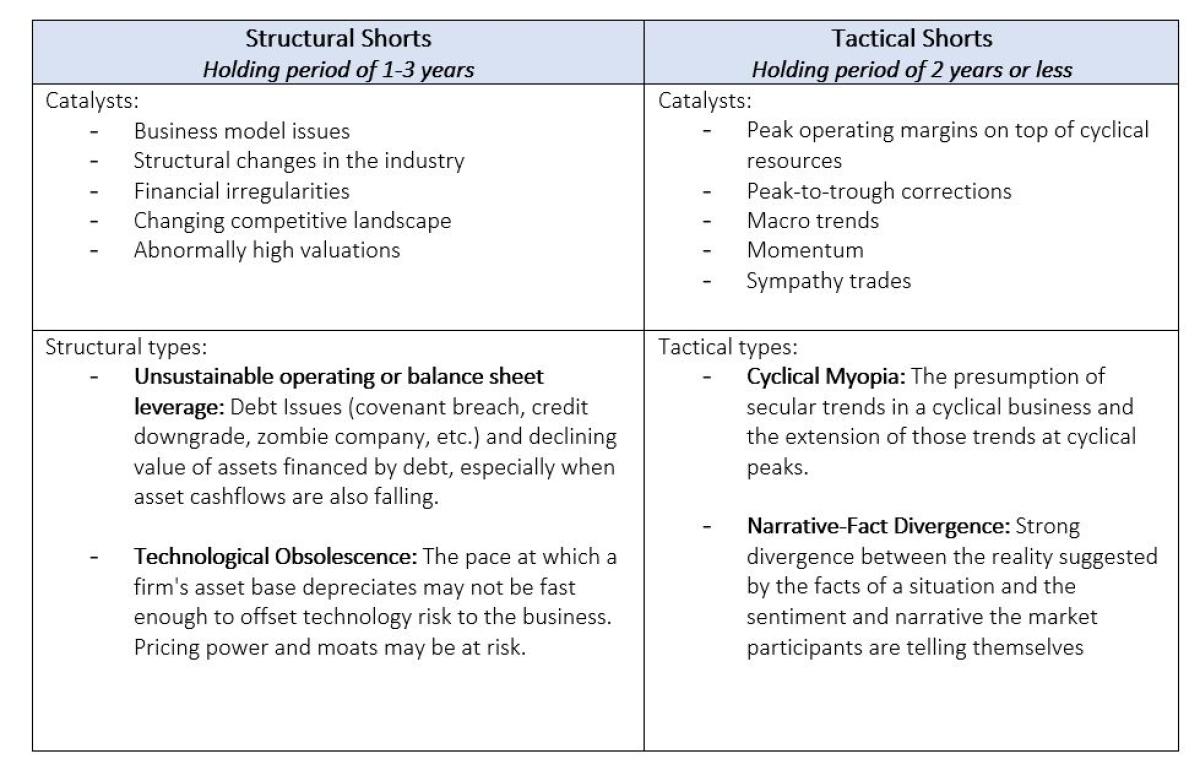

What We Look for in Shorts

Finding short candidates in real asset industries often is counterintuitive, as industry cyclicality can create transitory financial metrics. Broader economic tailwinds further complicate the process, often obfuscating poorly run businesses for many years.

With these complexities in mind, we construct our short book using a framework that helps us assess whether a particular company represents a structural short, defined as a stock impacted by negative catalysts in its business, or a tactical short, defined as a stock impacted by underlying shifts in market fundamentals. Categorizing short candidates within one of these two buckets subsequently enables us to determine target holding periods for each stock. While not every short can be neatly categorized within this framework, most demonstrate one or more of the following characteristics.

Where We’re Finding Opportunities to Short (& Where We’re Not)

During 2022, we found the opportunity set for shorts to be limited. More recently, we’ve identified some short candidates in battery metals, particularly those that complement our battery metal long positions. We categorize these as cyclical myopia-style shorts. We’re also exploring shorts in civil engineering and construction, which would be macro trend shorts or unsustainable operating/balance sheet leverage style shorts, depending on the company.

Additional opportunities may be narrative-fact divergence shorts. That said, the longer the downturn in the market, the fewer opportunities we expect to see in this category, as stocks in this grouping tend to re-price early in market corrections. Narrative-fact divergence shorts are also some of the trickiest shorts, as the market knows these companies purely through management’s stories about the business's future. Untethered from any fundamentals, the “spin” surrounding these companies can keep their stock prices afloat longer and at higher prices than might be expected. The purity of the narrative element underlying the security pricing means that narrative-fact divergence shorts also critically require careful risk management via hedges, as they are the most likely type of short to go against you in a punishing way. This complicates the short, as companies within this category rarely have a robust options market that enables cost-effective hedging. Additionally, narrative-fact divergence shorts usually are somewhat obvious, leading to significant short herding, which can result in an expensive cost of carry.

While also on our radar, technological obsolescence shorts are difficult to evaluate. In some regards, this category is the most dependent, counterintuitively, on a positive economic backdrop, as it is the corporate manifestation of Joseph Schumpeter's theory of creative destruction. For something to be obsolete, something must be better to supplant it. While creative destruction and progress are by no means confined to positive economic environments, they are often found in these environments.

How We’re Adjusting Our Short Allocation

Given our assessment in 2022 that the opportunity set for shorts was narrow, our short book has been on the smaller side. Therefore, as we came into the market’s drawdown, we left money on the table. Some shorts, such as the narrative-driven clean tech companies we believe were built on smoke and ideal for shorting in a falling market, fell so quickly that we mostly missed those opportunities. Other pockets of the market proved more resilient, falling slower than our ability to do due diligence. Regrettably, however, in the first half of the year, we missed out on many of the easiest short-side returns.

We’re currently fine-tuning our positioning, and with an investible universe of 2,500 companies across energy, materials, and heavy industries and the 45 sub-groups within these industries, we’re confident we will identify additional short candidates and increase our short allocation. The industries in which these companies operate will continue to be cyclical. They will be hot – or not – at different times. But with our long/short equity approach, we have the flexibility to move with the market and we intend to use this cyclicality to our advantage.

For more about why Massif Capital’s Will Thomson and Chip Russell believe a long/short vehicle is the optimal structure for real asset investing, we encourage you to check out this recorded webcast.

About the Author:

Mr. Thomson is the Founder and Managing Partner of Massif Capital, LLC. Mr. Thomson has experience in private equity and credit/political risk insurance, in addition to having served as a strategic and economic adviser to NATO/ISAF in Afghanistan. Before starting Massif Capital, Mr. Thomson worked in the New York office of Chaucer, a Lloyd’s of London insurance syndicate, serving as the co-portfolio manager for a $750 million portfolio of credit and political risk insurance policies. Mr. Thomson is a Graduate of Trinity College and holds a Masters in Government from Harvard University. Mr. Thomson is a member of Value Investors Club and has won or been a finalist in several investment contests including Sohn and the van Biema Associates Small Cap Challenge hosted by SumZero. He is consistently ranked as one of the top analysts on SumZero, a buyside community of 10,000+ members.