By George Aliferis, CAIA, CEO of Orama a video and audio marketing agency specializing in fintech and the content creator behind InvestOrama, a content platform that explores the future of investing across alternative assets, Defi, and technology - but without the hype.

A pragmatic view on REITs in portfolio construction, for income, capital appreciation or a step on or off the property ladder

On the surface, REITs present characteristics that make them convenient tools for achieving various investment objectives:

-

They will consistently distribute income (they have to)

-

Real Estate is a different asset class, thus offers diversification benefits if you mainly invest in bonds and stocks

-

A different risk profile: Property doesn’t usually go to zero. Even if a meteorite strikes your house, you should get an insurance payout (I think!)

But we’ve previously seen some of the challenges associated with REITs, as they are not direct property investments:

-

They are equity, not property(!), with various implications, from price action to market cap weighting

-

The choice is limited, and the labelling can be confusing: it’s not easy to find the right vehicle

-

They can be correlated with other sectors, in particular tech, because Telecom Towers and Data Centers are two of the largest REIT Sectors by market cap)

Let’s start by considering REITs for what they were initially invented: income, before going into portfolio construction.

Income from REITs vs Dividends & Coupons

A few years ago, I tried to explain to my Dad that you don’t need to have only income-producing assets in retirement. Leaving tax considerations aside, the result is the same if you have a total return index where dividends are reinvested, compared to a price return index where dividends are paid out.

But I was not looking at it from a lifestyle perspective. It changes everything.

If you are a “private investor” that’s not interested in the act of investing. For example, because you are retired and have better things to do. You want to spend the income you receive from your investments, and you want it to be frequent and reliable.

The purpose of REITs is to: “allow individual investors to invest in large-scale, income-producing real estate”.

The law requires that REITs pay dividends at least once annually; however, many REITs pay quarterly or monthly. It’s a regular and reliable income.

Looking at long-term averages, Broad REIT indices yield around 3-4%1, compared to 1-3% for equity indices.

These can vary, but broadly speaking, REITs have a yield advantage over equities. Yet, with the current 10Y Treasury yield at around 3.8%, income alone can’t justify a high allocation to REITs much riskier than bonds. However, anecdotal evidence (my Dad) suggests that monthly income (just like renting a flat but without the hassle) can be a factor. REITs have a frequency advantage over bond coupons paid annually or semi-annually.

Income explains the lasting appeal for REITs for rent-seekers. However, it’s not a compelling case for a purely rational investor.

If REITs are like a mix of bonds and equity, is there more to it than can justify their addition to a bond and equity portfolio?

Global REITS as non-diversifiers

If you invest in broadly diversified indices, you are already exposed to REITs.

It’s interesting to note that all the S&P 500 Real Estate companies are REITS. In theory, there could be listed Real Estate companies that decide not to distribute their profits and reinvest them.

-

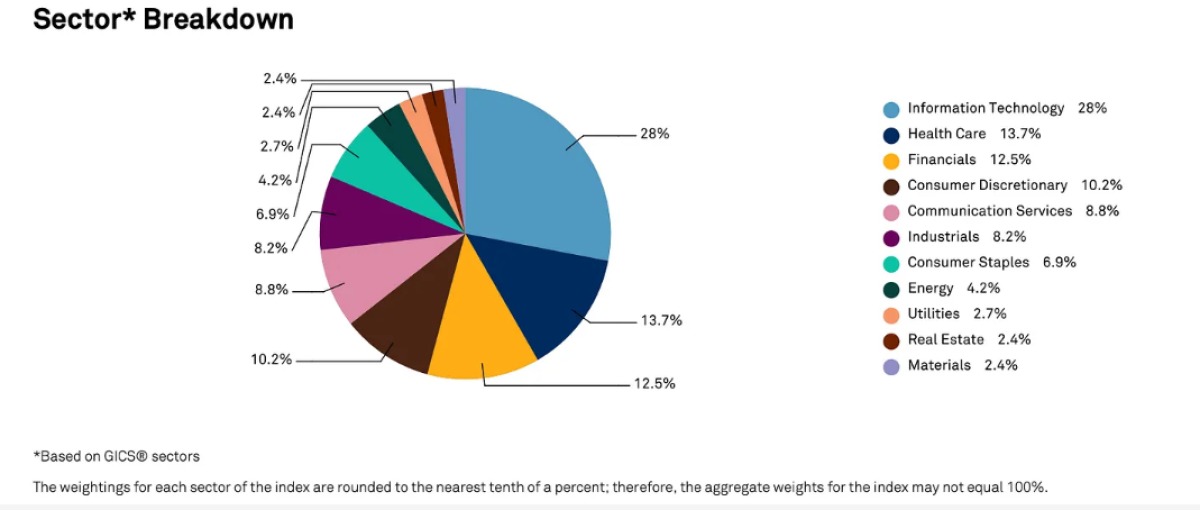

The sector breakdown for the S&P 500 Index indicates an allocation of 2.4% to Real Estate

-

For the FTSE Global All Cap, it’s 3.2%

So the question is, should you overweight to the sector?

Our friend and podcast guest Nicolas Rabener made a case against it in a detailed analysis.

You should read it in full, but here are his conclusions. The emphasis is mine:

This analysis does not make a particular strong case against allocating to real estate stocks, but the results are also not supportive either.

Despite REITs featuring only moderately positive correlations to stocks, the diversification benefits were marginal over the last 30 years. Stated differently, real estate stocks are just not unique enough and introduce additional, unnecessary complexity for asset allocation models.

Furthermore, the real estate asset class is largely a bond proxy and has benefited significantly from declining interest rates over the last 30 years. Given that bonds yields have reached zero or negative levels in many countries, this likely makes the outlook for real estate less appealing.

My previous article also made a case against allocating to broad REITs. Finominal’s quantitative perspective confirms that inadequacy from a data-driven perspective.

I was looking for a metaphor and thought mixing REITs into a portfolio would be like mixing different brands of cement: you get cement! But a quick search showed that actually, it can create a stronger cement mix if you combine the suitable cements.

So could you pick the right REIT to build a more robust portfolio? Let’s see if a more discerning approach, not based on broad REIT indices, can still justify their presence in one’s portfolio.

Adding Sector REITs or Individual REITs to the mix

It’s easy to match the S&P 500 and REIT sectors from the EPRA Nareit US.

Note Real Estate is, in fact, REIT exposure - not precisely the same thing!

For example:

-

Information Technology & Communication Services (“Tech”) - Data Centers & Cell Towers REITs

-

Health Care - Health Care REITs

This is an intuitive approach, as Causation implies Correlation. If Health Care is booming, they will hire more people, need more space, and rents and property prices will increase. This is not a direct link, but the equity performance will impact the speciality REIT sector.

This is also why Phil Bak mentioned the strong correlation between “Tech Stocks” and “Tech REITs” in our podcast conversation.

If you want to use ‘Real Estate” to diversify away from Tech stocks, avoid Data Centers & Cell Towers REITs. If you want to diversify away from stocks in general, avoid REITs that are linked to the dominant stock sectors: Tech and Health Care.

Phil also mentioned: “The correlations between the different REIT sub-sectors are very low, meaning that they trade differently than themselves. They're different economies within the REIT world.”

Picking sectors less exposed to economic activities should yield better results in terms of diversification from a bond & equity portfolio. And this intuitively draws towards Residential REITs.

So if Residential REITs make sense in your portfolio, the question that ensues is: how much should you allocate?

From a private investor perspective, that allocation depends on numerous factors, but one stands out: how much Real Estate exposure do you already have via property investments (including your residence)?

REITS to step on or off the property ladder

Let’s assume there is a Residential REIT that is well correlated to the price of your local property wherever you live- and you can buy it or short it!

The last part of the assumption, “short it”, is not realistic for a private investor. The rest of the sentence is highly hypothetical. Please bear with me!

Getting OFF the property ladder

On the podcast, Phil mentioned that, theoretically, many individuals are over-allocated to real Estate through our residence. Now, homes are much more than a financial asset and are typically excluded when assessing a Private Wealth client’s assets.

But you can sell your home - just not while you live in it!

For this exercise, let’s add a residence worth 500K to a 500K 60/40 portfolio. We now have a 1M portfolio with the following composition:

-

50% Real Estate (your home - illiquid and indivisible but still an asset)

-

30% equities

-

20% bonds

Here are some reasons you may want to reduce your Real Estate exposure:

-

From a financial perspective, you believe a 50% Real Estate allocation is excessive

-

You want more income and notice bond yields are higher than property

-

You think equities have better growth prospects than property

-

You’re planning to sell to downsize or rent, and you are concerned that property prices might fall

It makes sense to short the REIT to achieve those goals (remember you still live in the property).

Let’s say you are in case 4 and will purchase a new property worth half the current one. You decide to reduce your total exposure to 25% and maintain 60/40 for the rest.

You borrow 250K of the REIT and sell it. With the proceeds you invest 150K in equity and 100 in bonds, you now have:

-

25% Real Estate (and still live in your home)

-

45% equities

-

30% bonds

If property prices go up by 10%. You’ll sell the current property for 550, buy the new one for 275, and give back the REIT worth 275.

If property prices go down by 10%. You’ll sell the current property for 450, buy the new one 225, and give back the REIT worth 225.

You are now “perfectly” hedged (with many assumptions) against a decline in property prices.

This was unrealistic but fun!

Getting ON the property ladder

This is a slightly more realistic approach as it involves buying the REIT.

Imagine you’re planning to purchase a first property, and it’s a long-term goal. Your current assets increase yearly as you save, and they may also fluctuate in value.

The risk is well-known for many who struggle to get on the property ladder: property prices may rise faster than your savings, as it has done in the past. The first step of the ladder is getting unattainably high and keeps climbing.

If you’re in cash, then any property price increase will bring you further away from your goal. If you invest in risky assets, they may fall while property prices are steady or rise.

Note: We remove mortgages from the equation to simplify.

If, however, your savings were systematically invested in a REIT that followed property prices, you needn’t worry about their rise. The pool of assets dedicated to the purchase would grow at the same rate as the property value. All you have to do is save enough to achieve the purchase price, but it’s no longer a moving target.

So which REIT and how much of it

For private investors, REITs should be considered in relation to their existing portfolio, residential status, and direct property investments.

When it comes to the property ladder question, a lot depends on our assumption:

There is a Residential REIT that is well correlated to the price of your local property.

I mentioned previously how a quick search for UK residential REITs resulted in two tickers: HOME and RESI, with promising names but deceiving characteristics.

This is not straightforward. REITs are not ideal instruments. But there aren’t any better ones to transition from liquid assets to a property purchase, so they are worth considering.

I’ll finish with a personal anecdote.

In 2019, my family expanded. We felt our current residence was becoming too tight for all of us, so we were looking to move to a bigger house (see above - property ladder). We found one, but the conversations dragged (for technical reasons that I won’t explain). Our assets were in stocks and bonds, which would be transformed into cash to buy the new property.

In March 2020, the first lockdown was followed by a massive drop in asset prices.

My first thought was: “Be fearful when others are greedy, be greedy when they are fearful”.

My second thought was: “Hold on. These assets are dropping below the deposit threshold to buy a house”.

Then there were many thoughts after that. The one that prevailed is an image of a dystopian future, locked down in a tiny property with a little voice saying: “We could be sitting comfortably in a big property if Daddy hadn’t gambled on the stock market.”

And so I sold instead of buying stocks.

And then the property purchase fell through.

There are many things we could have done better to avoid this outcome. Could a strategic REIT allocation have helped? Potentially, but more fundamentally it taught me to have a holistic view of assets that includes life events and liabilities.

There's a new ETF that clones BREIT for a fraction of the cost - and has liquidity.

About the Author:

George Aliferis, CAIA is the CEO of Orama a video and audio marketing agency specializing in fintech, and the content creator behind InvestOrama, a content platform that explores the future of investing across alternative assets, Defi, and technology - but without the hype. Previously, George worked as a front-office professional for over a decade across derivatives, ETFs, and alternative investment products in Paris, Singapore, and London. He holds a Master's Degree from HEC Paris.