Authored by Aaron Filbeck, CAIA, CFA, CFP®, CIPM, FDP, Managing Director, Global Content Strategy

Space (Our industry) is big, really big. You just won’t believe how vastly, hugely, mind-bogglingly big it is. I mean, you may think it’s a long way down the road to the chemist (an asset management firm with a trillion dollars in AUM is large), but that’s just peanuts to space (the broader industry).

In The Hitchhiker’s Guide to the Galaxy, Douglas Adams uses a bit of humor to describe the overwhelming vastness of space, comparing it to everyday experiences to help readers grasp its scale—before pulling the rug out from under them and showing just how much bigger it truly is. Similarly, the world of asset management, particularly alternative investments, presents a mind-boggling challenge of scale and complexity. Just as space can leave even the most seasoned explorers awestruck, the sheer complexity of the alternatives market can feel equally uncharted and boundless.

Due to its size, varying degrees of transparency and disclosure, lagging values, and constantly changing composition, it’s increasingly difficult to nail down just how big it is. And this is an even bigger problem in alternative investments that are private and unregulated with infrequent (optional?) reporting and disclosure. It’s a tall task.

With this in mind, we’ve centered this edition of Chronicles of an Allocator on the industry’s growth, offering a clearer view of its scale as well as a few things to look out for as we welcome 2025.

DON’T PANIC.

Every few years, we try to not only measure the industry’s size, but also provide some context into how it’s changed over time. Earlier in the year, with the launch of our seminal piece, Innovation Unleashed: The Rise of the Total Portfolio Approach, we calculated the industry’s size to be approximately $22 trillion in assets under management. As we close out 2024, and the industry’s 2023 marks are finally in (yeah, it takes a long time to get those figures), we have an update.

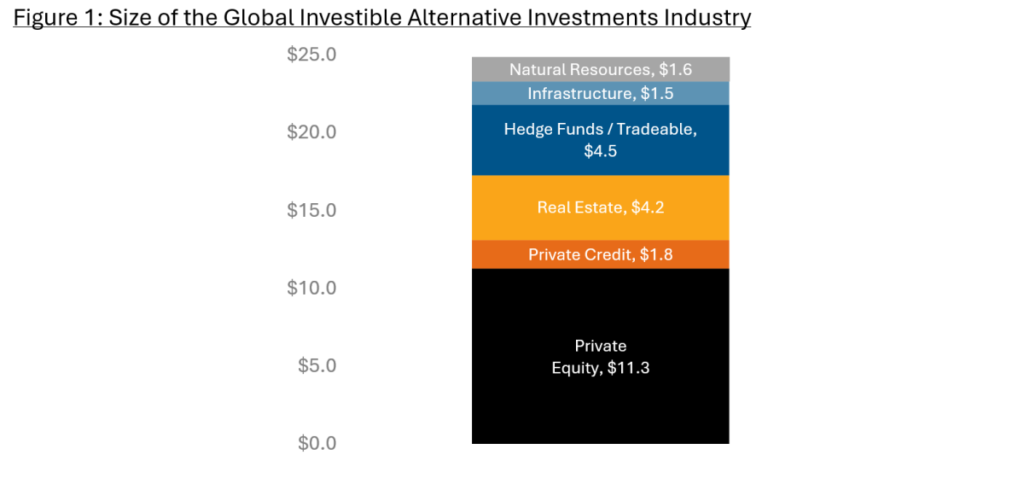

Today, alternative investments sit at $25 trillion in assets under management. The breakdown of this figure is shown in Figure 1.

Sources: CAIA Association, Preqin, Pitchbook, HFR, ANREV/INREV/NCREIF, Morningstar

Note: Final AUM figures may vary slightly due to rounding. Data comes from periods between 12/31/2023 – 6/30/2024 and includes drawdown funds, alternative mutual funds, UCITS, non-traded BDCs & REITs, interval funds, and tender offer funds

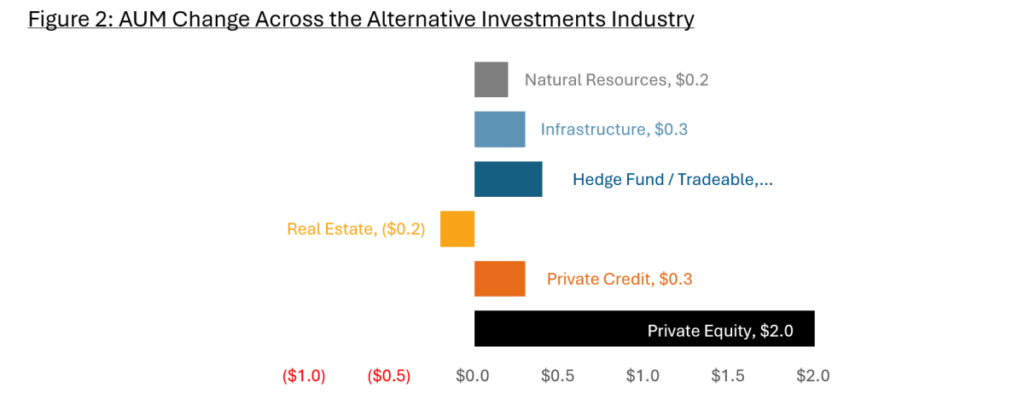

The usual caveats on the figures aside (read: there’s a lot of art involved in compiling and analyzing these measurements), one thing is clear: the alternative investment industry is continuing to grow!

Source: CAIA Association

Note: Figures display the change in AUM between figures calculated in Innovation Unleashed: The Rise of the Total Portfolio Approach (which may have changed from their publication date) and those in Figure 1. Approximately $400 billion of the total change is due to including registered products for the first time.

Private equity contributed to two-thirds of the growth ($2 trillion alone), but you can see that all corners of the alts industry have broadly participated. In fact, the only category to see a decline in AUM was real estate, which has gone through a challenging period of property value declines and low deal volume (though, according to Preqin’s H2 Investor Outlook, investors believe this will reverse).

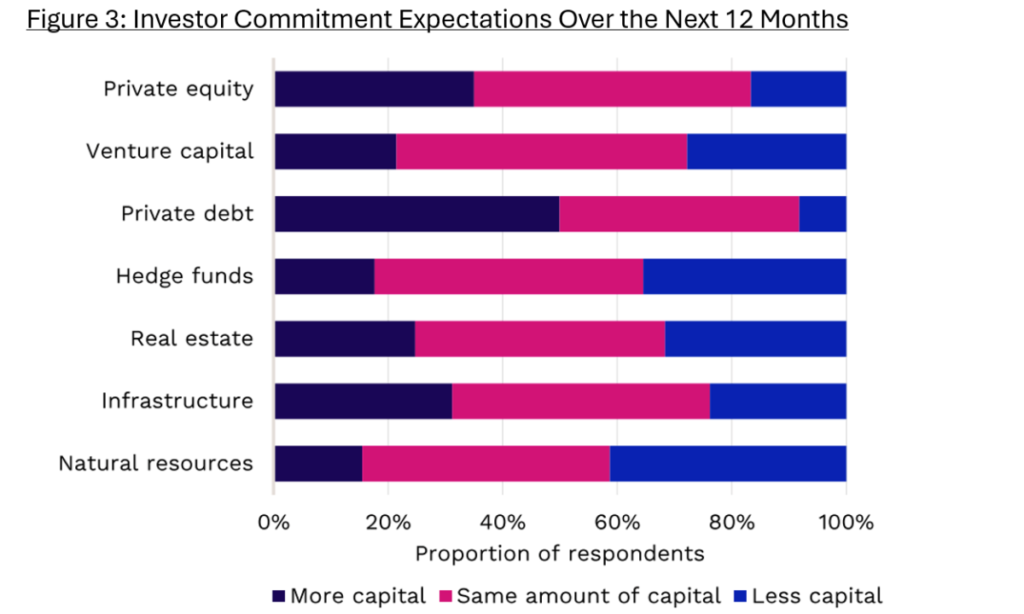

How does long-term historical AUM growth line up with investors expected commitments to asset classes over the next 12 months? According to Preqin, private credit and private equity remain the two primary places investors are making greater capital commitments, in lieu of hedge funds and natural resources.

Source: Preqin H2 Investor Outlook

Liquid Alternatives 2.0

Post-GFC, the hedge fund industry democratized access to hedge fund beta. In the 2010s, the private markets attempted the same thing. Therefore, it’s no surprise that the liquid alternatives market (i.e., registered products) is following a similar trajectory to their illiquid counterparts. For the first time, we explicitly incorporate evergreen and registered products in private markets strategies into our industry size calculations, as they’ve become more than a rounding error in the total AUM calculation. While we’ve been talking about these vehicles for some time, the flows are beginning to become material. Evergreen products account for $400 billion of the total increase in AUM and are primarily concentrated in private credit and real estate strategies.

In case you missed it, the writers at Pitchbook put out a fantastic report a few months back providing a comprehensive overview of the evergreen space. Preqin also covered this topic earlier in the year and even included LTIFs and LTAFs in their estimates, which are still very small relative to the overall industry and account for only $100 billion with less insight into the strategy breakdown. Semi-liquid products for the wealth channel are still very much a U.S. phenomenon but are gaining traction all over the world… even in ETFs?

Liquid alternatives are still an important component of the hedge fund strategy complex, but they have had a growth trajectory similar to those of their hedge fund counterparts. According to a Morningstar report, the two categories that have seen the most significant growth have been the Derivative Income and Options Trading categories, which grew 65% and 38% between 2023 and 2024. The rest have seen flat or negative growth, with Event-Driven and Systematic Trend seeing the most significant declines of -31% and -23%, respectively.

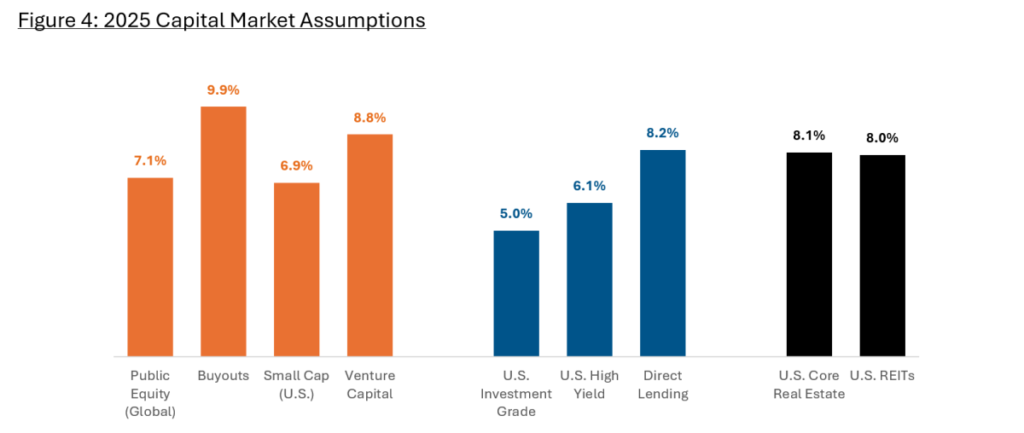

Capital Market Assumptions: How Can We Eat? Why Do We Eat? Where Shall We Have Lunch?

One of the tenants of embracing the Total Portfolio Approach is engendering a competition for capital among all asset classes and investment opportunities in the portfolio – in other words, no more buckets. Instead, every investment opportunity must compete for its place. A few years ago, competition may have looked very different when interest rates were unprecedented, and risk premia tilted in favor of risk-on assets. However, today’s return expectations are much tighter amongst assets that look like one another, as shown in Figure 4.

Source: Excerpt from the 2025 Long-Term Capital Market Assumptions Report, JPMorgan

For example, despite being earlier in the lifecycle, venture capital and small cap equity median return expectations are lower than those of buyouts and global large cap equities. Median private core real estate and REITs have similar return expectations as well. Finally, private credit seems to be a bright spot at face value, but it’s important to note that pockets of risks may be building if you don’t take the time to dig in (more on this later).

On the median level, return differentiation continues to be tough, though dispersion of returns in private markets would suggest an opportunity for incremental value-add (if you can identify and access those opportunities ex-ante).

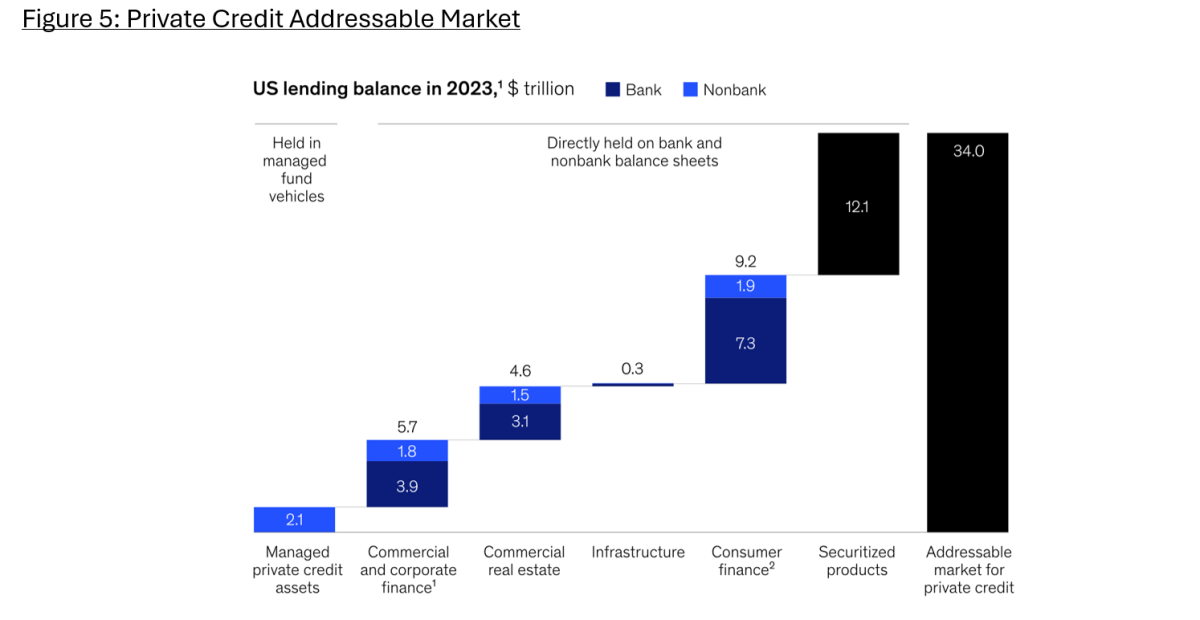

Spotlight on Private Credit: The Bulldozer Trying to Create a Bypass

Have you any idea how much damage you would suffer if we just let private credit roll straight over the entire economy? So far, none at all. After all, it’s a bypass for the last decade…and you’ve got to build a bypass!

According to McKinsey, the addressable market for private credit is roughly $34 trillion in the U.S., as shown in Figure 5. Combine this with the fact that banking systems outside of the United States are still the primary lender, meaning that the total addressable market for private credit managers is far bigger than the current AUM would suggest.

Source: McKinsey & Co.

According to the report, the industry will likely partner with other players in the ecosystem to take advantage of this massive opportunity, it’s just too large. In fact, the banks may once again enter the lending business as a partner (a co-investor?).

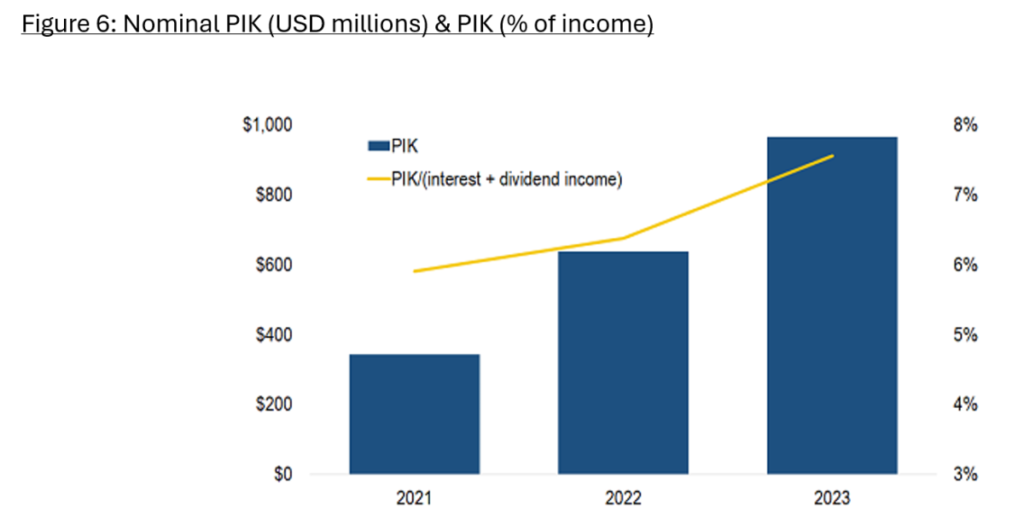

As this secular trend unfolds, it’s worth looking at the cyclical trends as well. After rates shot up in an uncharacteristically short period over the past two years, companies and investors still haven’t had time to digest the implications for credit risk. While the yield is attractive at face value to investors, they are a cost to companies. In a recent note from Pitchbook in October, the proportion of paid-in-kind to total income is on the rise, as shown in Figure 6.

Source: Pitchbook | LCD. October 2024.

Digital Assets: Like Vogon Poetry

Just as you should never listen to a Vogon recite poetry, on no account should you allow a crypto bro to talk crypto price action with you. (Note, if you need a laugh, check this video from the Morning Brew.)

With a second Trump administration confirmed in the U.S., attention and energy is moving back to the crypto space, supported by all-time highs and positive price action post-election. While the U.S. government is no longer a first mover regarding digital assets, it’s still the largest and most developed economy in the world.

Trump has made digital assets part of his policy platform, promising to do things such as encouraging all the remaining Bitcoin to be made in the U.S., creating a Bitcoin reserve, and deregulating the industry through sweeping changes at the SEC. He’s even acronym-ed his new efficiency department after the meme-coin named after the Shibu Inu. For those interested in following more, I would encourage you to read this blogpost from Duane Morris on the implications of the U.S. elections on the digital assets ecosystem.

What will be interesting to watch is what and how the U.S. embraces or differs from other regulatory regimes around the world. The Middle East (via the UAE) has been one of the leaders in terms of adopting and enabling supportive regulations, going back as far as the mid-2010s and furthering in 2022 with the creation of the Virtual Asset Regulatory Authority (VARA). According to a report from CoinGeek, the UAE received $30 billion in digital assets, making it MENA’s third-largest digital asset destination after Turkey and Saudi Arabia.

So Long, And Thanks for All the Fish

There are many things to be excited about in this industry. Innovation continues, growth is everywhere, and there’s plenty of stones to uncover for the intellectually curious. We’ve included a few resources for you below if you need some holiday reading beyond what we’ve laid out here.

Finally, as we close the calendar year, I wish you all a wonderful holiday season. Whatever you celebrate, I hope you have time to unwind, reflect, and spend time with loved ones. See you in the New Year!

Other Resources:

Technology That Could Define the Decade

If you’re interested in reading about some of the coolest innovations in technology that will impact markets, healthcare, energy, and transportation, you’ll really enjoy this short read from Morgan Stanley. 2030 is only five years away, and we’re dreaming pretty big. Themes discussed include artificial intelligence, autonomous vehicles, and … robots?

Capital Decanted: Artificial Intelligence

Quant shops, hedge funds, and algorithmic trading firms have embedded AI in their models for over a decade. But have we hit a tipping point where applications of these accelerated computing capabilities are ready to invade the more traditional asset management business? What are those use cases, and which are most promising? How should we think about a peaceful future co-existence of the human and the machine in managing portfolios? Martin Escobari and Dave Morehead joined a recent episode of Capital Decanted to unpack this provocative topic.

New research from David Chambers, Elroy Dimson, Antti Ilmanen, and Paul Rintamäki examine the growing body of work examining historical returns and their viability when trying to forecast future returns. If you’re looking for an academic nerd-out session (38 pages!), but also hoping for a few nuggets of wisdom on how to forecast better, this is a good read.

If you’re trying to think through the next steps of your own career around year-end, this piece walks through the different “levels” to investment management that separate the novices from the greats. Also, a perfect read for newcomers to the industry trying to hitchhike their way up the ladder.

The Less Efficient Market Hypothesis

Common wisdom would suggest that markets have become more efficient over time, as information becomes more readily available, technology improves, and investment costs come down. Not so, says Cliff Asness, PhD of AQR Capital Management. In this article from The Journal of Portfolio Management, Cliff outlines three reasons why markets have become less efficient over the past three decades, and what investors can do about it. Worth a read for investors trying to figure out how to position their portfolios, and themselves, as we enter a period where lack of information is less of a problem than sifting through too much of it.

Everything In Its Right Place, Including Every 2025 Private Markets Outlook

Ever wanted a centralized place to read every single 2025 private markets outlook in one place? Look no further than this LinkedIn post from Andrea Carnelli Dompe. The post features outlooks from all of the largest asset managers and GPs (and even has page references for the lazy ones).

Photo Credit | iStockphoto: da-kuk