By Christopher M. Schelling, CAIA®, Director of Alternatives, Venturi Private Wealth.

An investor’s defense of a maligned metric.

Dear IRR,

It seems like every time I see the letters ‘IRR’ in an investment article or financial news site, the story is about how terrible you are. Internal rates of return are misleading, inaccurate, and untrustworthy. You are not directly comparable to a compound rate of rate of return, and you don’t represent what investors actually earn.

I may be guilty of some of the same criticism as well. I’ve often said you can’t rely on just one performance metric alone in private markets, because you don’t get the whole picture from IRR. But I think at this point the disparagement has gone too far, and for any role I’ve had in that, I’m sorry.

You see, misperception isn’t the same thing as being misled; communication is a two-way street. Maybe investors haven’t done a great job understanding you. Perhaps we ought to do a better job listening. We need to see things from your perspective. I think if we do that, maybe we’ll realize you’re not so bad after all.

I don’t often draft letters to financial metrics, but I feel compelled to address IRR directly given hyperbolic rhetoric surrounding the issue of late. IRR certainly isn’t perfect, but it’s far from the completely worthless figure it’s been portrayed as of late.

Imagine you are trying to measure returns on a single private equity transaction. Let’s say someone invested $100 into a private company, and exactly four years to the day later, received $200 back when the company was bought by a new owner. That’s a pretty typical scenario for any given deal — two times your money in four years’ time.

Calculating IRR is difficult by hand, but Excel makes it easy, yielding an IRR on the transaction above of 18.91 percent — a solid return. But if we listened to all the haters, that’s just a meaningless number. Thankfully, on such a simple example, we can also calculate the compound rate of return, or geometric mean. If you invested $100 into a mutual fund, and four years later had a balance of $200, you’d get the following geometric rate of return: ($200 / $100) raised to the power (1/4), minus 1 equals … 18.92 percent!

(The geometric rate of return is 0.01 percent higher is because IRR uses a day-count methodology, and over 4 years, there is one leap year. So, if you used the power (365/1461) for the compounding period, you would get exactly 18.91 percent annualized geometrically as well.)

The numbers are identical, so maybe IRR does measure what you earn after all?

But I can already hear the critics howl: “That’s not what a real private equity portfolio looks like!” They will say there are cash flows in and out, and over time, that’s what causes the calculation to deviate from what investors actually earn.

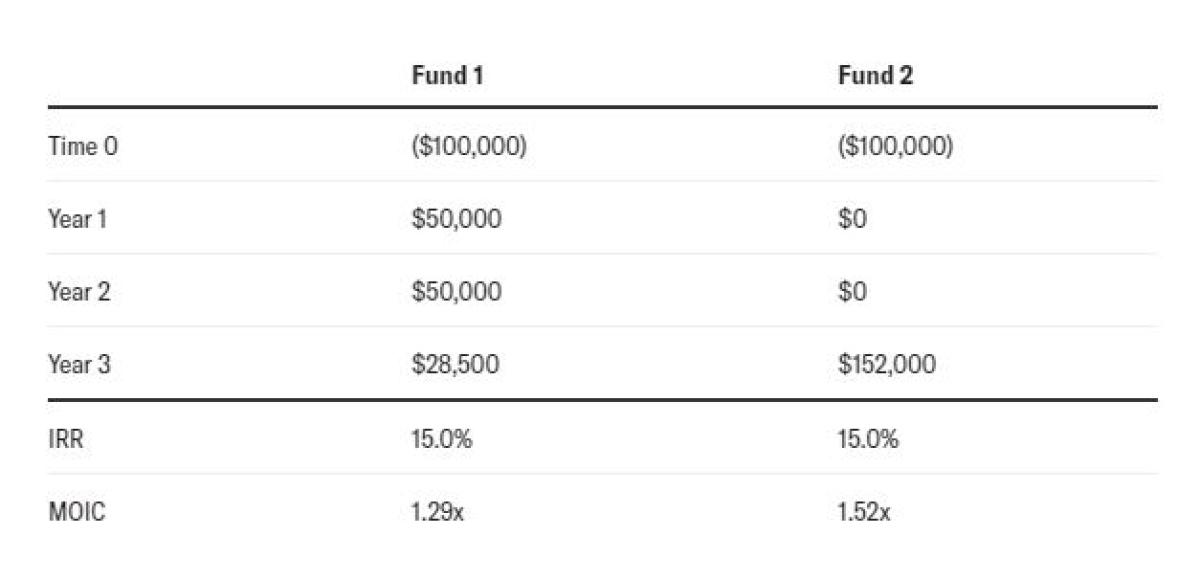

Let’s imagine two different funds. One invests $100,000 at inception and receives payments back over a three-year life. In Fund 1, you get half of your capital back in the first year, another half the next year, and small final gain in year three. In the second fund, there are no distributions in the first two years, and a lump sum return of $152,000 in the third year.

Both portfolios produce an IRR of 15 percent, but very different multiples of invested capital (MOIC). You make 1.52 times your invested capital in the second case, but only a measly 1.29 times in the first one.

Aha! See, this proves that IRR is misleading, just as we all suspected! Or does it?

There is a real difference in risk in the two scenarios above. In the first fund, half of your invested capital is already back by the end of the first year, so your risk is significantly lower. And if your capital is compounding for a shorter period, of course the cumulative return may be less, but your rate of return is the same.

Wait a minute. This all looks very familiar, like a story I’ve seen before. Bonds! These examples resemble two different maturity bonds.

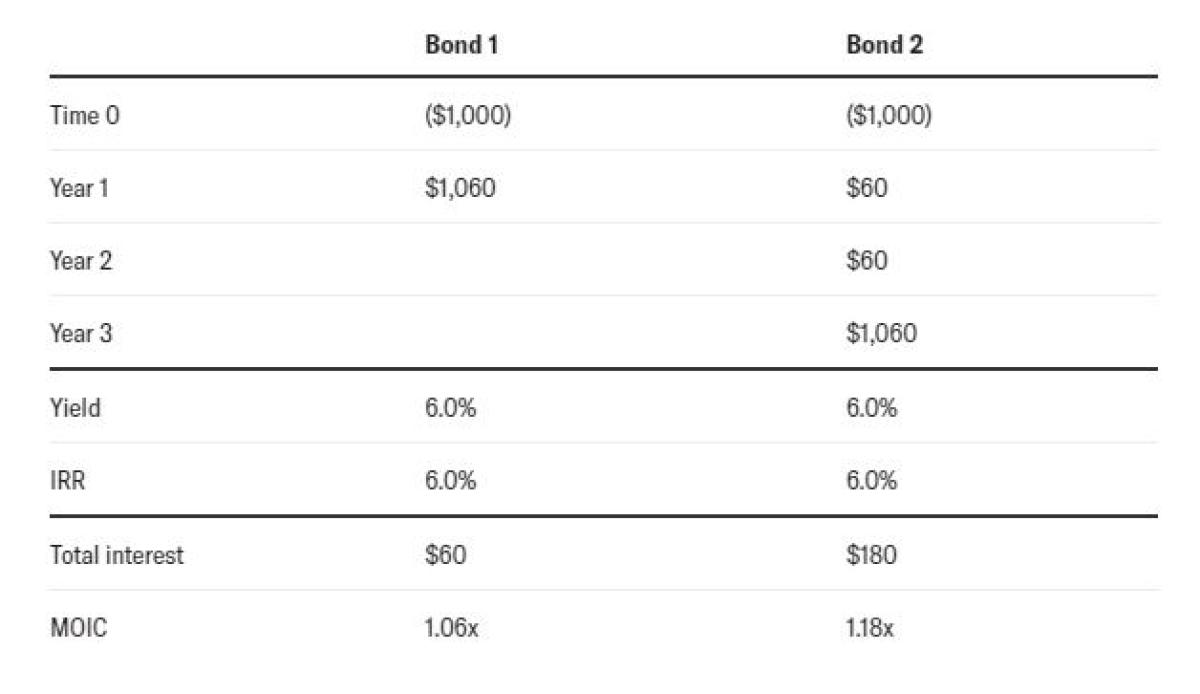

A shorter maturity bond with the same yield is going to pay less in total interest than a longer bond will, even though the interest rate may be the same. If, for comparison’s sake, we had a one-year, simple interest bond with a 6 percent yield and a three-year bond with the same yield, we’d have the scenario below.

For the first bond, you get interest plus your principal back at the end of year one. For the three-year bond, you would receive $60 interest payments over years one and two, and then the final principal plus interest check in the third year.

The 6 percent yields are the same for both bonds, and IRRs are identical as well, despite the fact that one lender receives $18 in total interest payments and the other receives just $6 for their capital.

That’s simply how it works. Investments of shorter duration will yield lower total cash on cash returns, but that fact does not invalidate their rate of return. Going back to our fund example above, the capital at risk in fund 1 is significantly lower than in fund 2. In fact, I would calculate a dollar-weighted principal duration of 1.5 years in fund 1, versus three years for the second vehicle. In private markets, duration isn’t just the date you get your last dollar out; it’s also opportunity cost.

When you get your money back faster, you have less risk, and in exchange you have the option to reinvest the capital in other investments. Sometimes rates are lower and sometimes they are higher, but in general reinvestment risk isn’t an actual risk; it’s an option. That’s why yield curves are typically upward sloping. Locking your capital up longer is riskier, and you should require a higher annualized yield to do so, like 7 percent or 8 percent for the three-year bond.

Similarly, it seems to me investors should not look at these two funds as equivalent. The typical view is that Fund 2 is superior because the IRRs are equal and the higher MOIC means a higher total return. A contrarian argument would be that fund 1 is far less risky because you get all your principal back much sooner. If anything, maybe fund 2 is a crummy deal because its IRR isn’t higher for the longer duration risk you are taking, just like bond 2.

Both these examples are simplistic. Funds don’t call capital all at once, and these scenarios still don’t look like a true private equity portfolio. Not enough cash flows in and out, and interim IRRs are even less accurate.

You’re being too easy on the dastardly old IRR, critics will tell me.

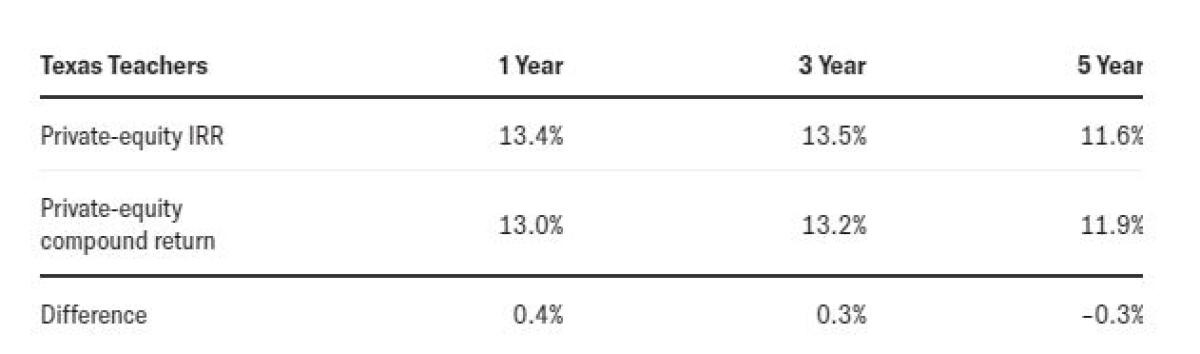

Let’s turn to a real-world comparison of IRR versus compound rate of return on a large, mature private equity portfolio. The Texas Teachers Retirement System has approximately $21.5 billion in net asset value and twenty-plus year track record in the asset class — they don’t get much larger or more mature than that.

Thankfully, Texas Teachers calculates and reports private equity returns in both IRR and geometric terms. Over the last five years, the portfolio has yielded 11.6 percent in IRR terms, versus an 11.9 percent compound rate of return, according to a July 2020 board report. These returns are pretty impressive over all periods reported, but more importantly, the variance between the two methodologies is typically just a few basis points.

It certainly looks like IRR is indeed pretty much what you earn, and not some wildly inaccurate and bogus metric. Maybe it can be misinterpreted, particular early on in the life of a fund during what is referred to as the J-curve. Over short periods, IRR and compound returns can diverge significantly. And large early cash flows can create a very high IRR, but that doesn’t mean it’s false. Short-duration strategies with quick return of principal do earn high rates of return, and since they are lower risk, they will have a lower cash on cash return.

But over longer periods, and on mature portfolios, IRR begins to track compound returns more closely. And most businesses use a similar process for capital project budgeting. IRR actually is pretty much what you earn. Maybe that’s why most of the best private equity investors I know — GPs and LPs alike — are still heavily IRR focused.

To finish my ode to the statistical figure…

Overall, IRR, I think you are fine. Like all of us, you have your flaws. While critics may have attacked and demonized you, I’ll keep using you — appropriately and with other relevant metrics, of course. I know you’re not stupid, IRR. You’re just math.

Your (limited) partner,

—Chris Schelling

About the Author:

Chris Schelling is the Director of Alternatives for Venturi Private Wealth. Chris is focused on sourcing, performing due diligence, and building portfolios of alternative investments for clients. As an institutional investor, Chris has invested roughly $5 billion and met with over 3,500 managers across hedge funds, real assets, private credit, and private equity in his career.

Chris is currently a contributing columnist for Institutional Investor and has authored over 60 articles on investing. He is also the author of Better than Alpha: Three Steps to Capturing Excess Returns in a Changing World. Better than Alpha provides the perspective, insights, and tools you need to retrain your focus away from searching for alpha and toward actions that produce superior investment outcomes through a simple three-step framework for making better investment decisions: Behavior (smart thinking), Process (smart habits), Organization (smart governance).

Previously, Chris was a managing director at Windmuehle Funds, a boutique investment firm, leading sourcing and structuring for niche alternative investments. Prior to this, Chris was the Director of Private Equity at the $30 billion Texas Municipal Retirement System. And before this, Chris was the Deputy Chief Investment Officer and Director of Absolute Return at the $15 billion Kentucky Retirement Systems. Chris has over 20 years of experience in the investment industry, nearly all focused on alternatives.

Chris was named one of Money Management Intelligence’s 2012 Rising Stars of Public Funds, a Rising Star of Hedge Funds by Institutional Investor in 2014, received the Institutional Investor Intelligence Award for Absolute Return Strategies in 2016, and was named a Top 30 Private Equity Investor by Trusted Insight in 2018. Chris holds a bachelor’s degree in Psychology from the University of Illinois. He received an MBA from the University of Illinois-Chicago and a master’s degree in financial markets from the Illinois Institute of Technology as well. He holds the Chartered Alternative Investment Analyst (CAIA®) designation.