By Boris Okuliar, Partner and Co-Head of Global Liquid Credit, Brian Abdelhadi, Partner and Portfolio Manager in the Ares Credit Group, and Elliot Hill, Vice President in the Ares Investor Relations Group.

We believe the European leveraged loan market is one of the most compelling yet underappreciated asset classes within the sphere of global credit. Over the past two decades, the asset class has evolved into a distinct opportunity set, while also building a performance track record that stands out among competing asset classes. For example, European leveraged loans have generated a higher average rolling five-year Sharpe ratio over the past ten years compared to U.S. loans, U.S. and European high yield bonds, emerging market corporates as well as U.S. and European equities1. Additionally, the asset class has produced 10 consecutive calendar years of positive total returns, delivering 4.6% on an annualized basis2. This leading risk-adjusted performance is positioned to continue if one considers the current market environment. The asset class consistently offers one of the highest yields across the public credit markets, while an exclusively institutional investor base should support a stable return profile given their longer-term investment horizon as well as the pricing power of CLO investors.

The credit performance of European leveraged loans has been a notable driver of the attractive risk-adjusted return profile. The asset class has achieved lower average defaults and higher recovery rates compared to other segments of the leveraged credit markets3. Furthermore, the rate of improvement across these metrics has also been superior3. This could be attributed to the underlying borrower base that increasingly consists of larger and more mature companies in addition to tenured private equity sponsors. Structural and compositional features of the asset class have also promoted the credit performance. For example, the asset class is almost entirely categorized as first lien, while the opportunity set is well diversified across countries and sectors, with notably large allocations to industries that are generally less cyclical in nature. Notably, European loans typically bring diversification across a broader portfolio given that there is a limited amount of overlap when compared to the companies that appear in European equity and high yield bond markets.

The rate structure of the asset class is another key factor when considering risk-adjusted performance. Negative underlying base rates impact the all-in yield of fixed rate bonds; however, this dynamic is negated in the loan market through Euribor floors. Moreover, fixed rate bonds are negatively impacted by upward moves in interest rates, while loans are insulated from this impact given their floating rate characteristics.

The significant increase in “cov-lite” loans has been a notable change to the asset class and is arguably a detrimental development from a lender’s standpoint. However, this dynamic provides an issuer with more flexibility to focus on navigating through difficult periods thereby potentially improving the investor’s default experience. Additionally, we believe the increasingly important integration of ESG factors by both borrowers and lenders could be a large driver of change within the asset class, but will ultimately make loans an attractive place for those investors who are focused on sustainable investments.

This paper demonstrates an attractive investment opportunity that we see in the European leveraged loan market, making the case that the asset class should be considered as a core holding in a well-diversified portfolio.

The evolution and compelling performance of European leveraged loans

- A large and increasingly liquid opportunity set

- Leading risk-adjusted returns

- Returns going forward are supported by attractive yields

- Institutional ownership promotes stability

The attractive risk-adjusted return profile is driven by:

(1) strong and improving credit performance

- Low default and high recovery rates

- Maturation of the borrower base

- Seniority in the capital structure

- A diverse opportunity set

- Defensive sector composition

(2) the rate structure of the asset class

- Protection from negative rates

- Well-positioned for rising rates

Shifting market dynamics that investors should be aware of

- The prevalence of covenant-lite loans

- Growing focus on Environmental Social and Governance (“ESG”) considerations

European Leveraged Loans: The Basics

European leveraged loans are a form of debt issued by companies that typically hold a publicly available credit rating below investment grade. They are floating rate instruments that pay a Euribor base rate, which resets periodically (usually every three months), plus a spread that provides investors with a satisfactory level of compensation for the additional credit risk that they are assuming, compared to a “risk-free” investment.

Leveraged loans are generally classified as secured 1st lien instruments, which means that a loan investor has first claim on the company’s assets and cashflows in the event that the company defaults on their debt repayments.

The evolution and compelling performance of European leveraged loans

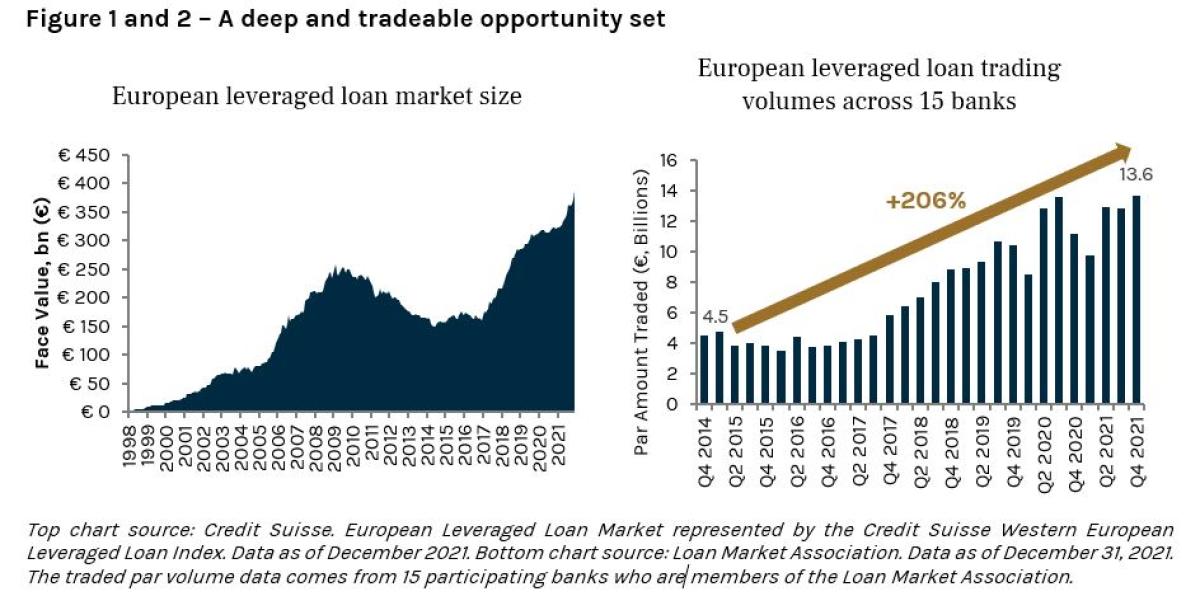

A large and increasingly liquid opportunity set:

With over €350 billion outstanding and around 500 individual issues, the European leveraged loan market has evolved into a distinct segment of the financial markets. The asset class has seen considerable growth having more than doubled in size over the past five years (Figure 1).

The combination of significant growth and a larger pool of issuers across which to invest has led to increased liquidity within the asset class. This dynamic is evidenced in Figure 2, which shows a 206% increase in quarterly trading volumes across 15 major sell-side banks since the fourth quarter of 2014. As a result, large-scale investment managers can potentially trade loans in the hundreds of millions of euros over the course of a few days.

Leading risk-adjusted returns:

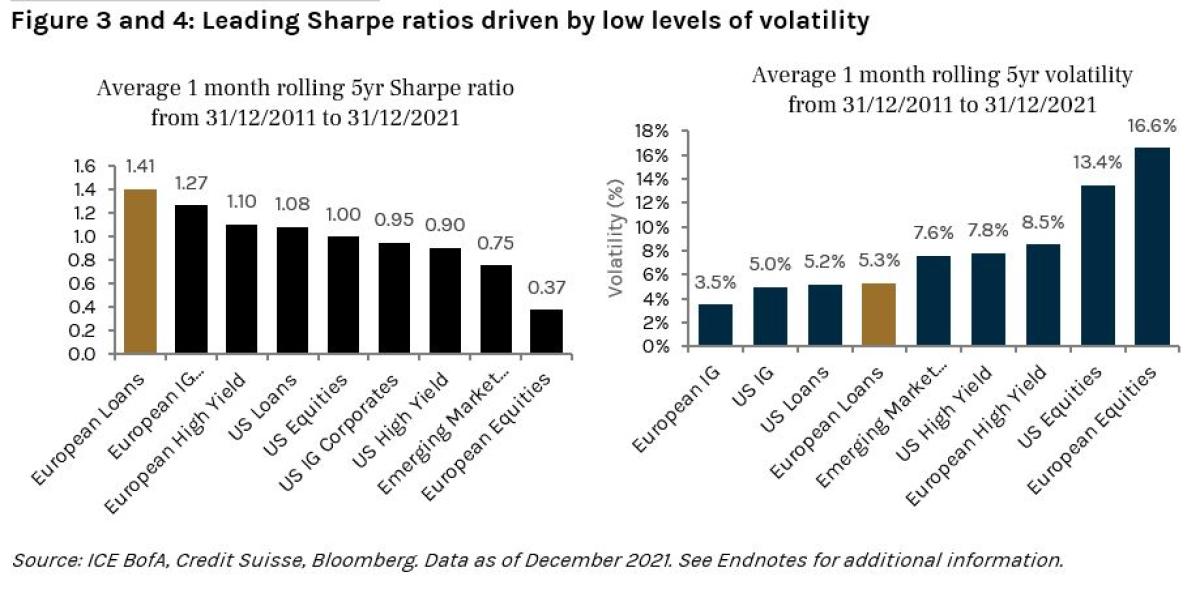

European leveraged loans have delivered superior risk-adjusted returns over the past 10 years when considering the average rolling Sharpe ratio over the same period compared to many other liquid global alternatives (Figure 3).

In our view, one of the key merits to the European leveraged loan asset class is its track record of low volatility. It is this lower level of volatility (standard deviation) that has driven the Sharpe ratios higher. As shown in Figure 4, European loans have produced materially lower levels of volatility compared to many other segments of the market, such as high yield bonds and equities.

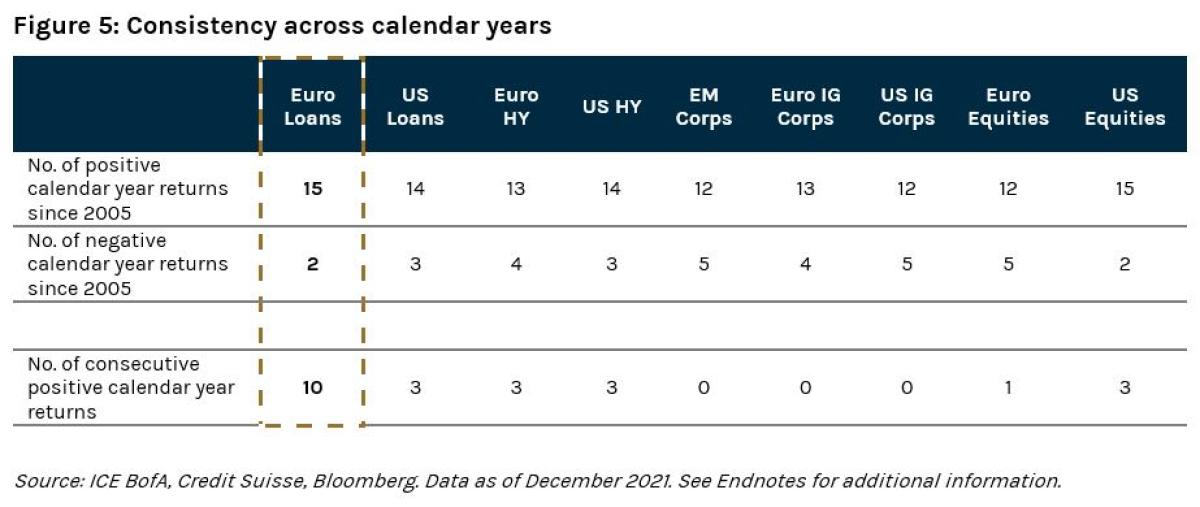

The Sharpe ratio is not the only way to see the stability and consistency of the European leveraged loan return profile. Over the past 17 years, European leveraged loans have delivered the highest number of positive years of total returns compared to other competing markets. Furthermore, as of December 2021, European leveraged Loans have produced the longest period of consecutive positive calendar year returns (figure 5).

Returns going forward are supported by attractive yields:

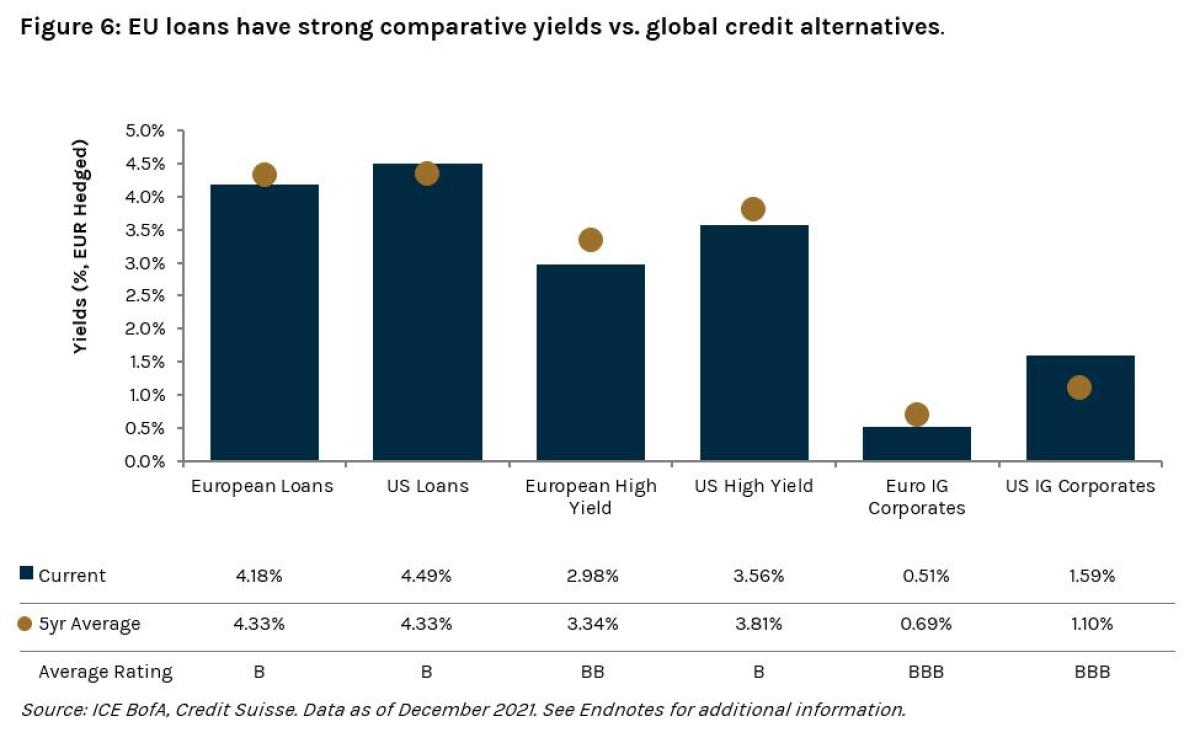

European loans have consistently provided a yield of ~4%+, which compares favorably to high yield in the U.S. and Europe and is more than eight times greater than the five-year average of European investment grade corporate bond yields.

We believe this measure of valuations suggests that the return experience across global leveraged credit markets should be favourable going forwards; however, if we couple this with the aforementioned characteristic of low volatility, European leveraged loans appear well placed to continue delivering attractive risk-adjusted returns.

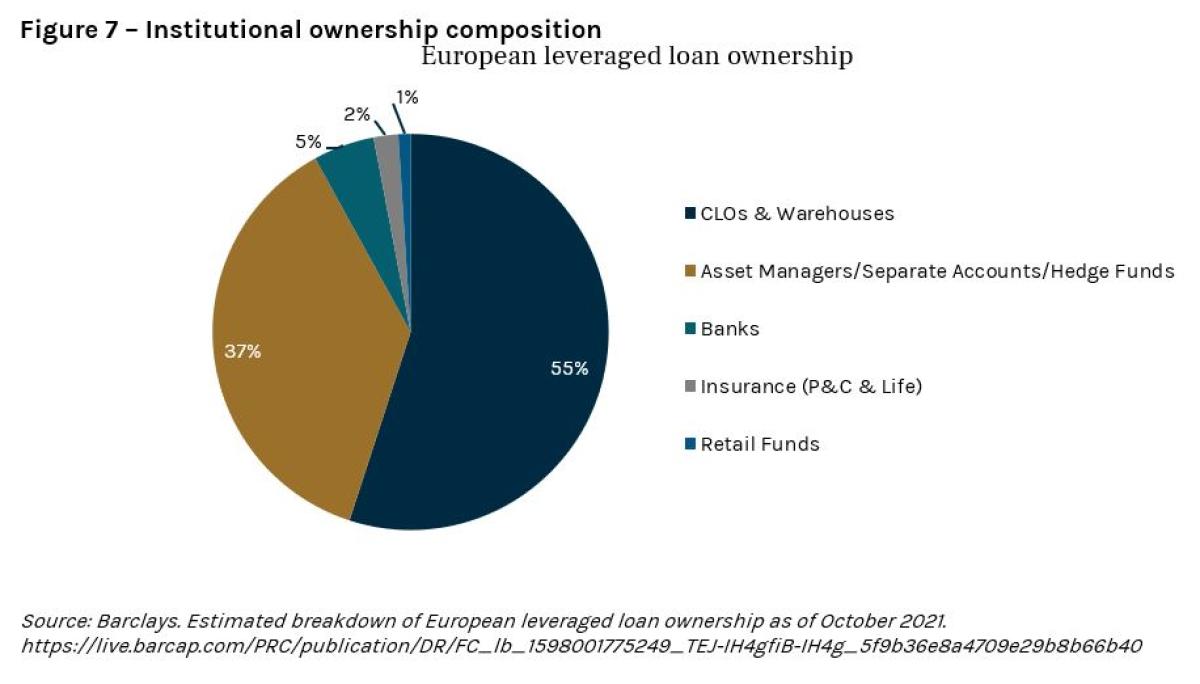

Institutional ownership promotes stability:

The growth of the asset class has been underpinned by strong demand from an exclusively institutional investor base. For instance, collateralized loan obligations (CLOs) are estimated to own over 50% of the market, while the next largest investor type comes in the form of separately managed accounts and funds for investors, such as insurance companies and pension funds(Figure 7). This ownership composition has meant that demand for the asset class has a relatively low sensitivity to prevailing market sentiment, which has helped to characterize a stable return profile. For example, institutional investors tend to have a long-term investment horizon, meaning the asset class tends not to suffer from short-term technical pressures associated with retail fund outflows. Moreover, the CLO investor base has a degree of pricing power given their significant proportion of ownership. As a result, there tends to be a floor on valuations within the new issue market that aligns with a CLO investor’s return targets.

The attractive risk-adjusted return profile is driven by:

(1) strong and improving credit performance

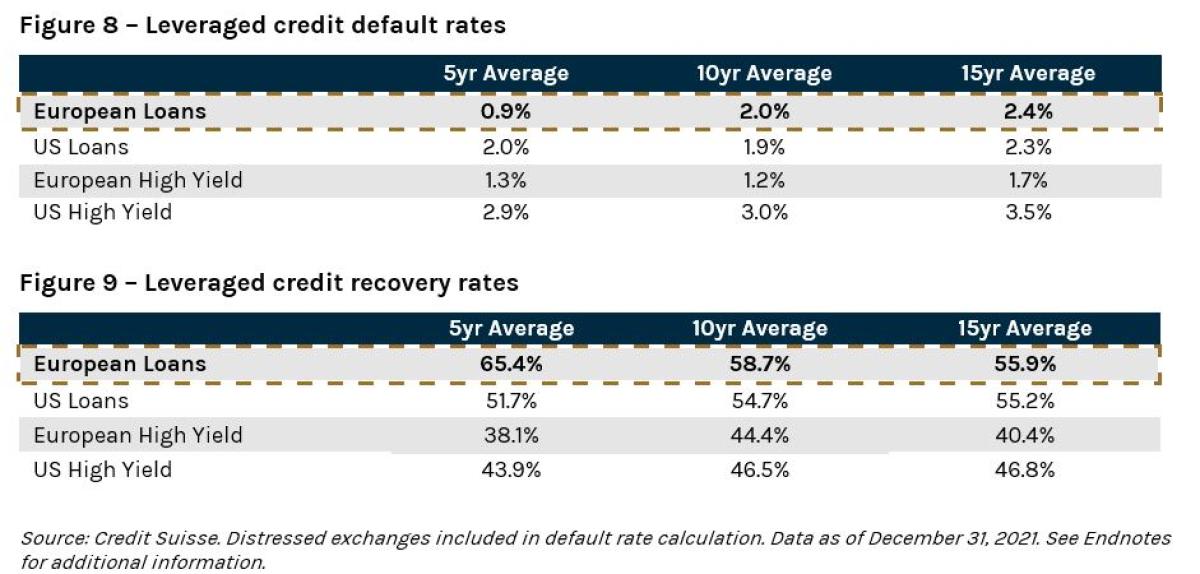

Low default and high recovery rates:

Default and recovery rates are key metrics to consider when assessing below-investment grade asset classes. A default is typically associated with significant downward price action, and investors ultimately getting back less than they originally lent to a given company. As such, limiting the default experience can have an important bearing on the volatility and risk-adjusted return profile of an asset class.

European leveraged loans have historically fared well relative to other segments of the leveraged credit markets when comparing default and recovery rates. Default rates are lower than the U.S./European high yield and U.S. loan markets over the past five years and are tracking in line with these markets over longer time periods (figure 8). The recovery rate experience has been even more impressive, with European loans at the top of the pile over a 5, 10 and 15-year lookback period (figure 9). We believe both metrics have contributed towards the favorable volatility and risk-adjusted return profile the asset class has exhibited on a consistent basis over time.

Maturation of the borrower base:

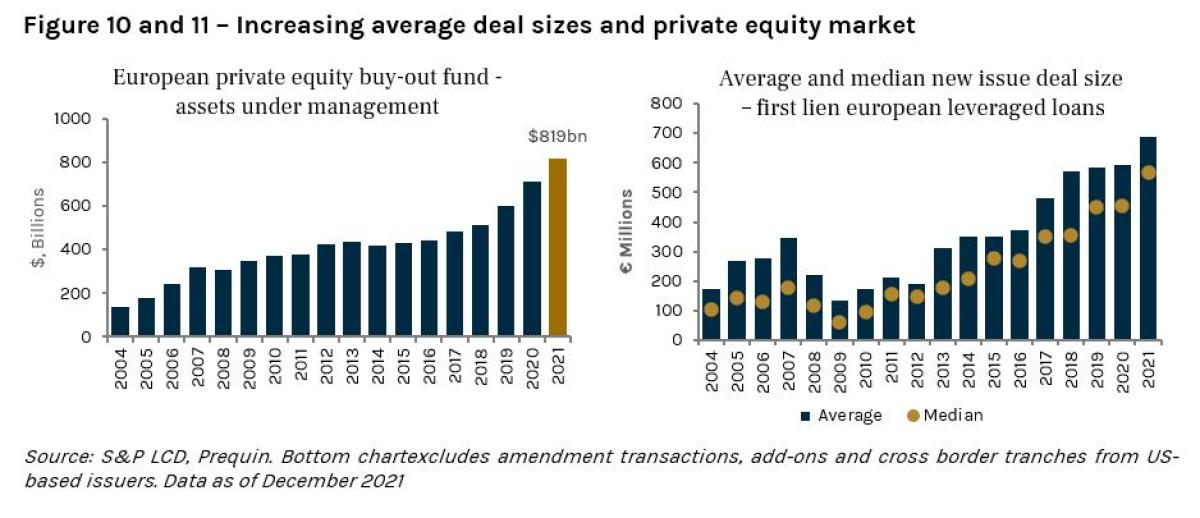

What is also notable about the default and recovery trends is the rate at which they have improved in the European leveraged loans space compared to other leveraged credit markets. In our view, this underlines the extent to which the European loan market has matured in recent years. For instance, around 70% of new Loan issuance over the past 10 years has been associated with private equity sponsored credits. As shown in Figure 10, the European private equity market has also grown and matured in recent years, with sponsors increasingly willing to provide the necessary support to their portfolio companies in difficult periods, thus avoiding a default scenario. Additionally, the market has become more diversified over time, with an increased number of mature companies that are larger, more established, and less likely to default when compared to smaller issuers that are increasingly turning to the direct lending markets to raise capital. Figure 11 below demonstrates this theme by conveying the rise in the average size of new issues that have come to the market. These deals have more than tripled over the past 10 years from approximately €200 million to €700 million.

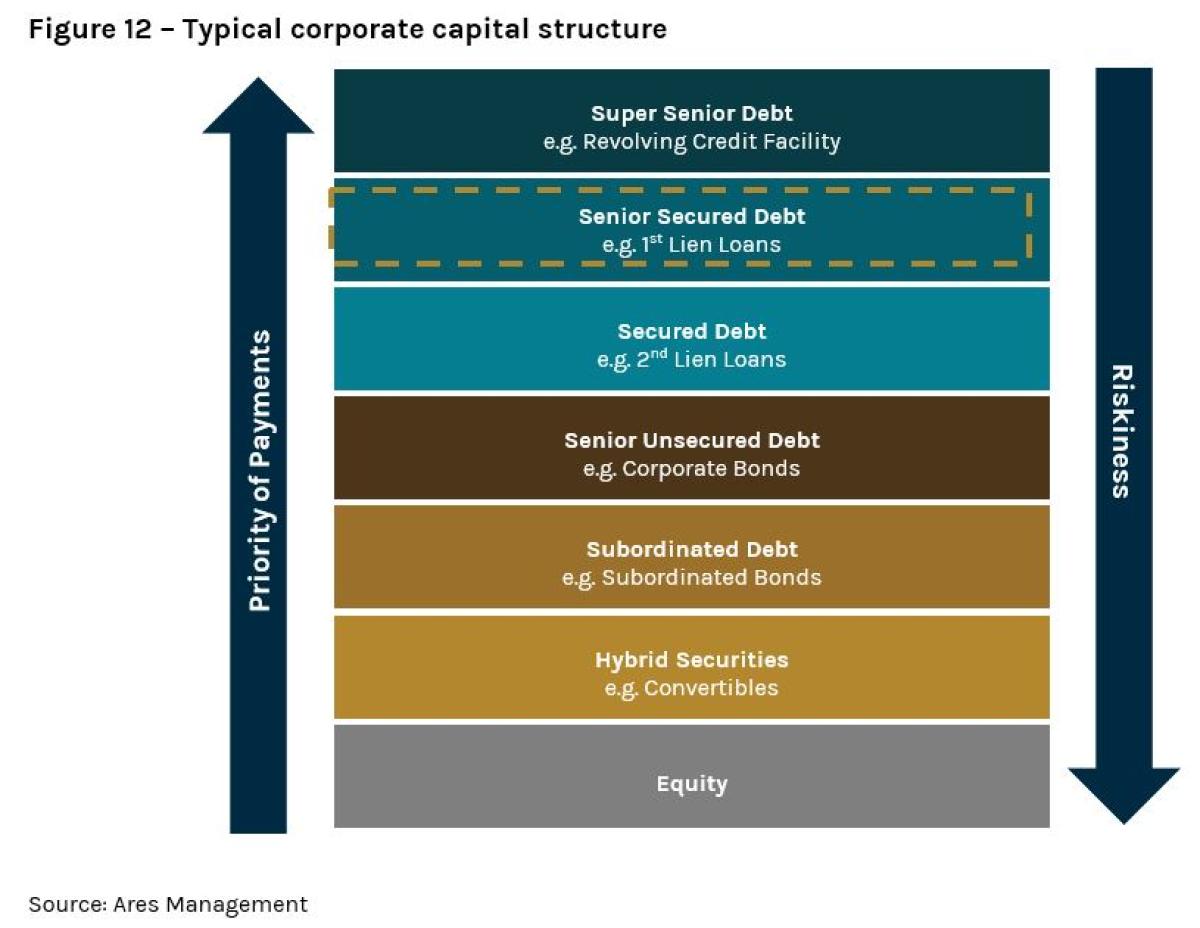

Seniority in the capital structure:

Over 95% of the leveraged loan universe is classified as 1st lien senior secured debt. This classification places the asset class in an elevated position within a company’s capital structure. Investors in 1st lien debt benefit from a higher certainty of income as they will be prioritised with regards to interest payments. In addition, they also have the first claim on a company’s assets in the event of a default and liquidation. The fact that the loans are “secured” implies that they are supported by assets pledged by the company; for example, shares of operating companies or physical assets such as machinery or plants. Meanwhile, over 70% of the high yield bond market is classified as unsecured and therefore sits below loans in the capital stack. This characteristic helps to explain why bonds have typically experienced lower recovery rates in the event of default (figure 9). Equity investors sit at the bottom of a company’s capital structure and will only receive dividend payments once all financial obligations with debtholders have been met.

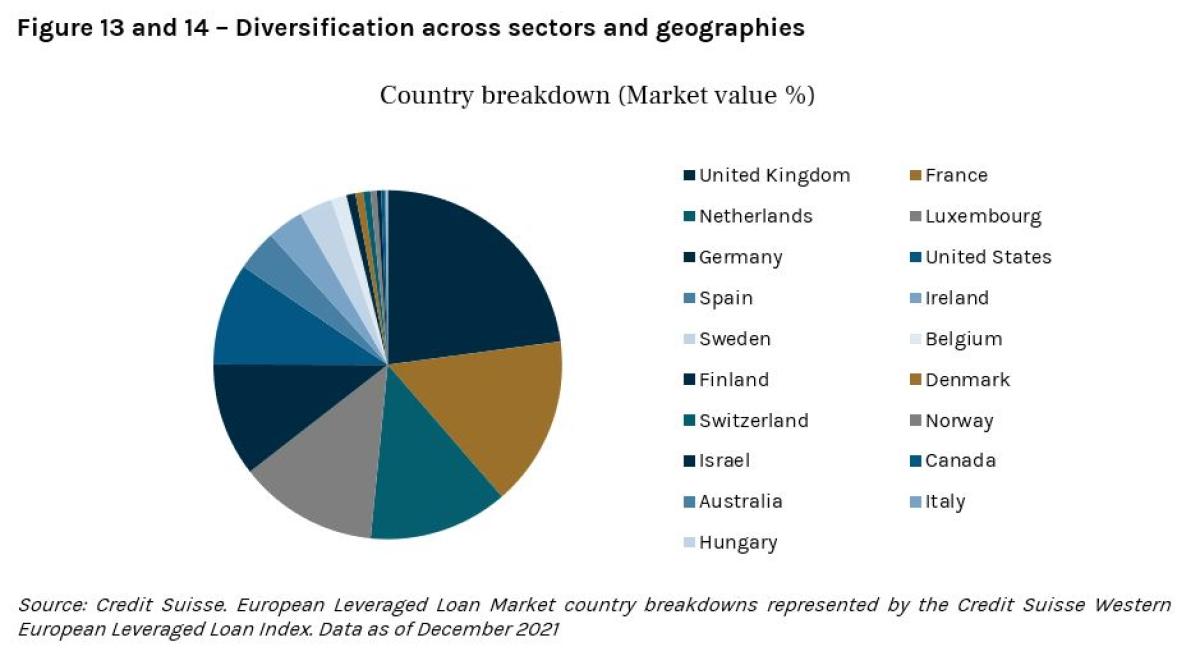

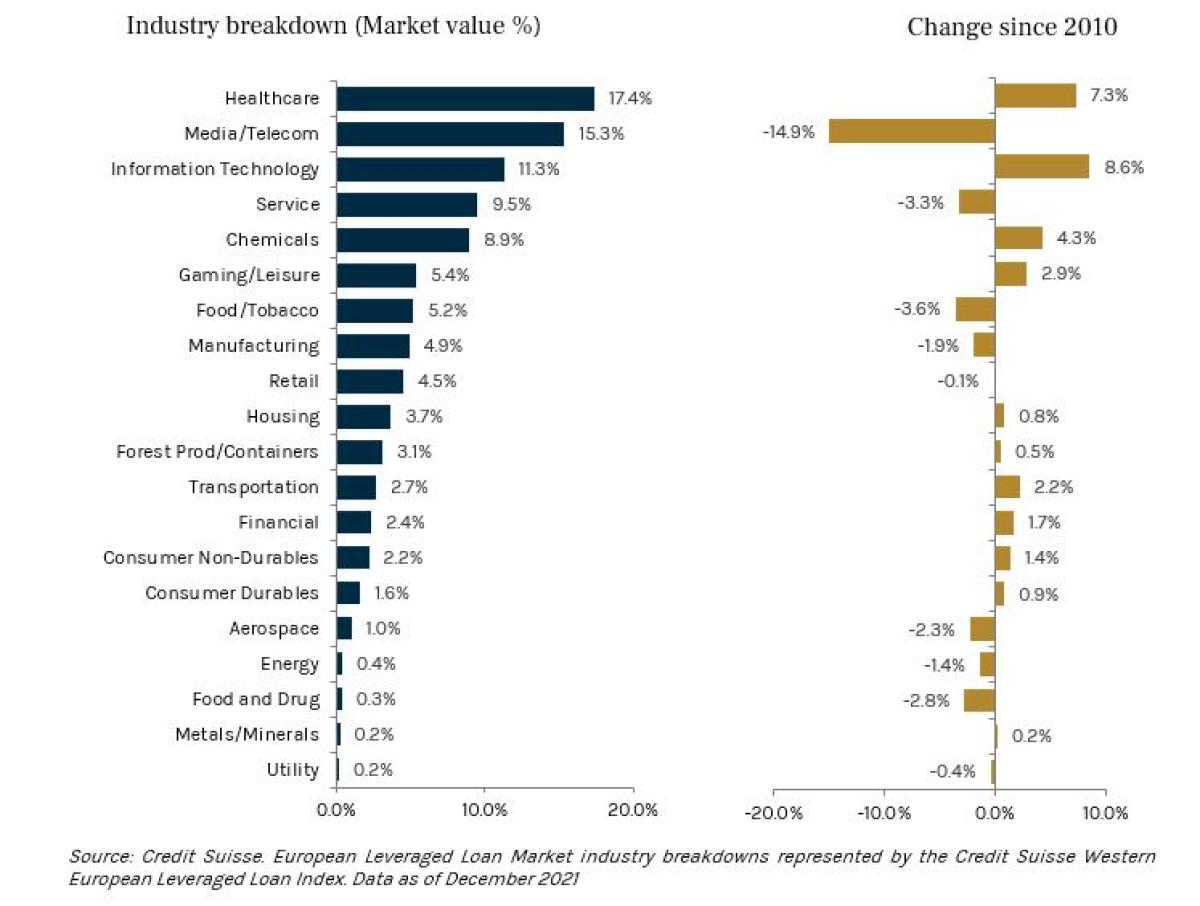

Credit risk can be materially reduced if a portfolio benefits from a well-diversified opportunity set. With over 560 loan deals issued by companies operating in 20 distinct industry sectors across 19 countries, we believe the composition of the European leveraged loan market provides ample levels of diversification within the opportunity set (figures 13 and 14). Furthermore, the change in these compositions over time also reveal increased diversification. For example, the media/telecom sector made up more than 30% of the total market back in 2010; however, this has since reduced to around 15% as of December 2021, with other sectors such as technology, healthcare and chemicals taking a notably higher share of the market.

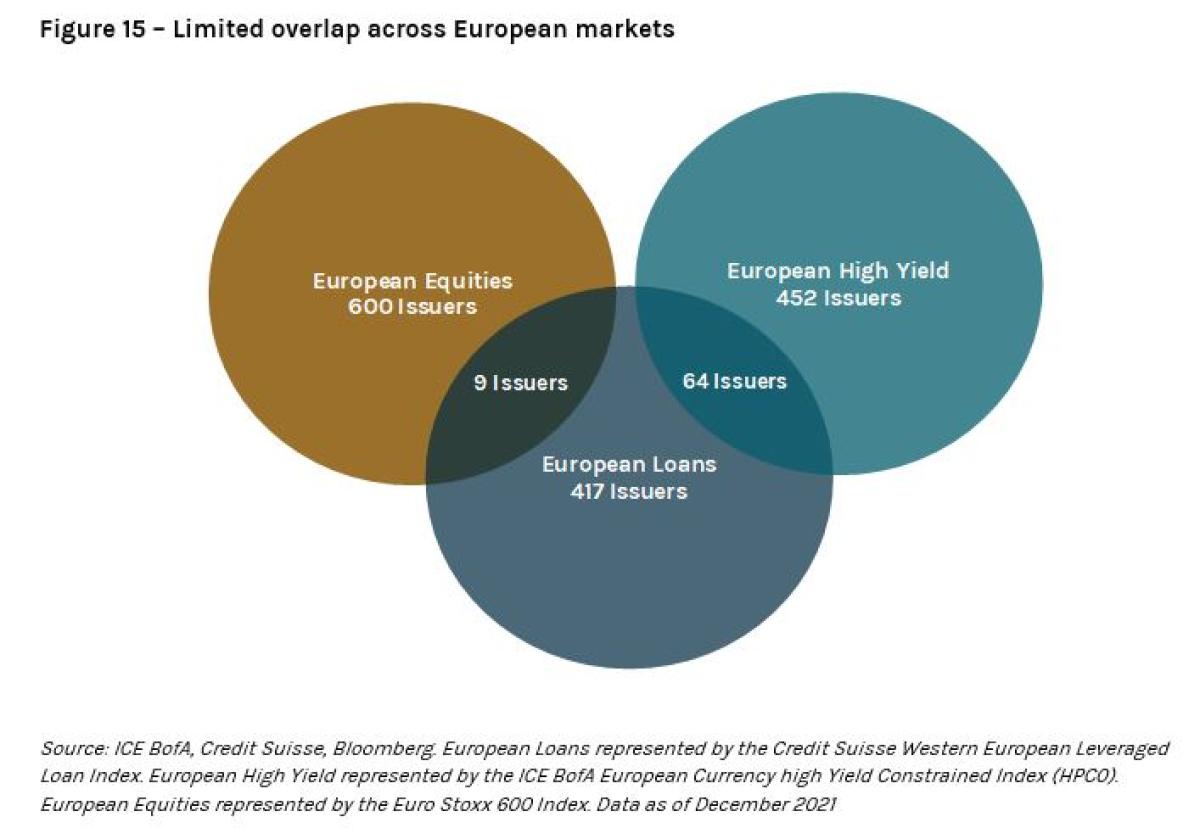

In addition to diversification within the opportunity set, we believe that the European leveraged loan market also diversifies a broader portfolio by exposing an investor to many companies that are not present in European equity and high yield indices. As highlighted earlier in this paper, the majority of European leveraged loan volumes have been associated with private equity sponsored companies. As a result, there are just nine issuers in the European leveraged loan index that overlap with public European equities (Eurostoxx 600). Moreover, most issuers in Europe tend to choose either the loan or bond market in order to raise debt. Since 2009, the average proportion of loan-only and bond-only primary market supply within the European leveraged credit markets has been over 80%. Consequently, there are only 64 issuers with both loans and bonds outstanding in Europe. Meanwhile, within the US leveraged credit markets, it is more common to see issuers access both the high yield and loan markets in order to raise capital.

The low levels of issuer overlap with other European asset classes helps ensure that investors in European leveraged loans are truly diversifying their portfolios, providing an increased number of idiosyncratic opportunities while also improving the overall credit risk profile.

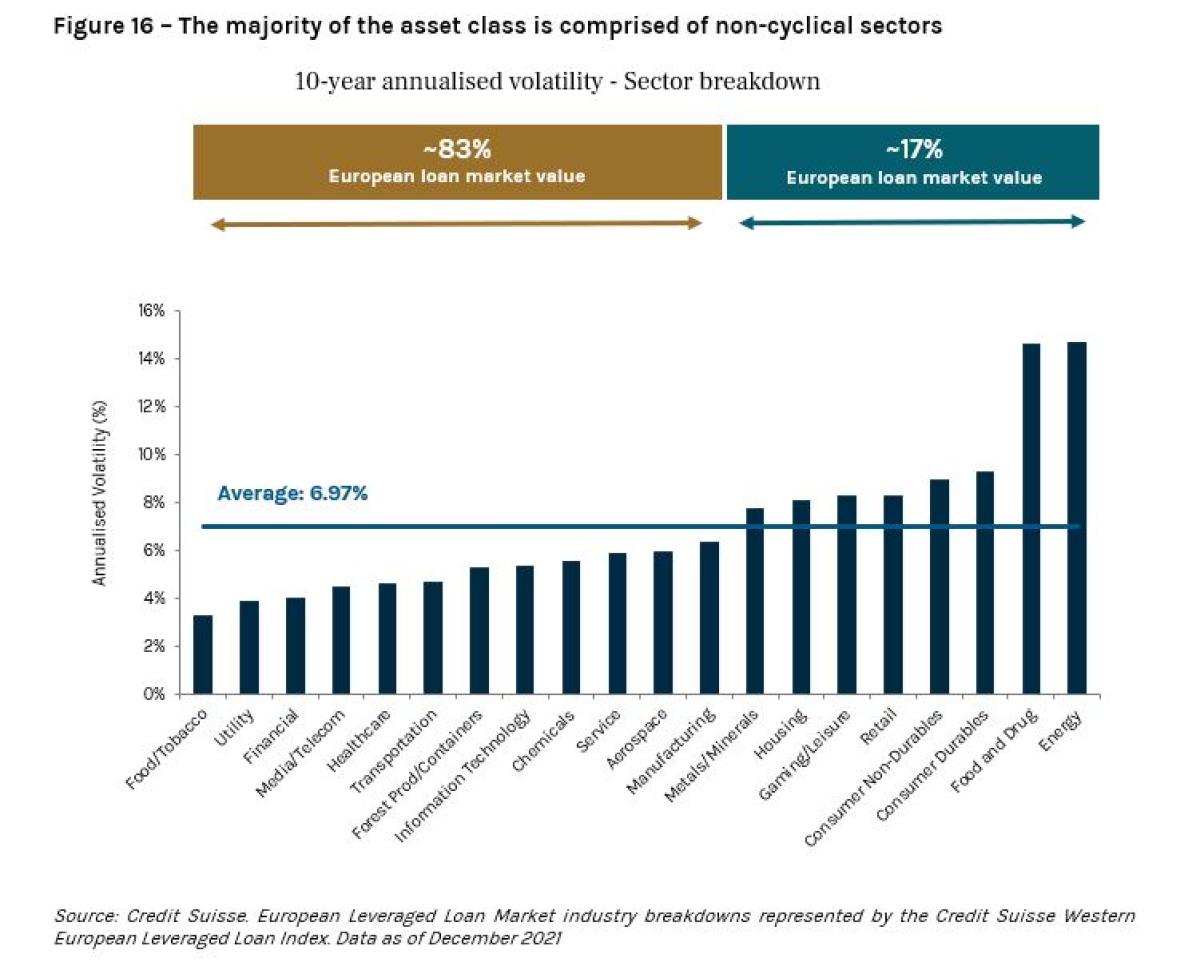

Another compositional factor to highlight concerns the sector distribution within the asset class. European leveraged loans have a lower weight to some of the more cyclical sectors that exhibit relatively high levels of volatility. For example, 83% of the asset class (in market value terms) has a 10-year annualized volatility below the market average.

Some of the least volatile sectors within the asset class make up a significant portion of the total market value. For instance, telecoms/media and healthcare are among the five least volatile sectors, representing 22% and 12% of the market on average over the past 10 years respectively. Unsurprisingly, energy has been the most volatile sector, however its ten-year average weight in the index is less than 2%2.

The attractive risk-adjusted return profile is driven by:

(2) the rate structure of the asset class

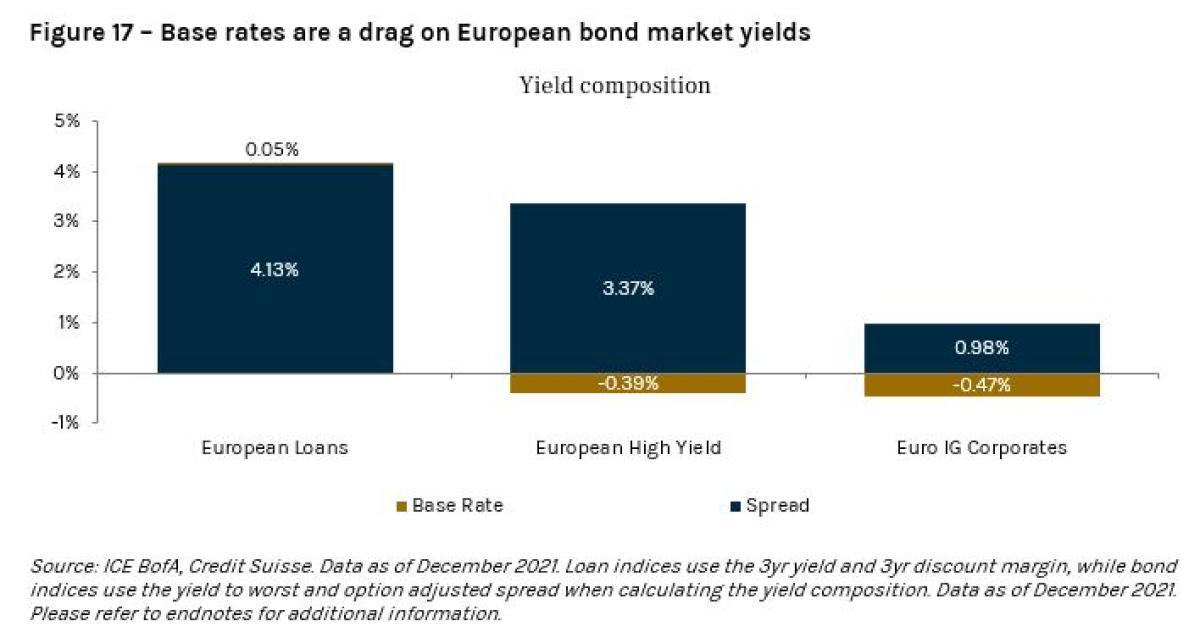

Protection from negative rates:

A prominent theme that has characterized fixed income markets in recent years – particularly those in Europe – has been negative interest rates, which have proved to be a drag on all-in yields in the bond markets (Figure 17).

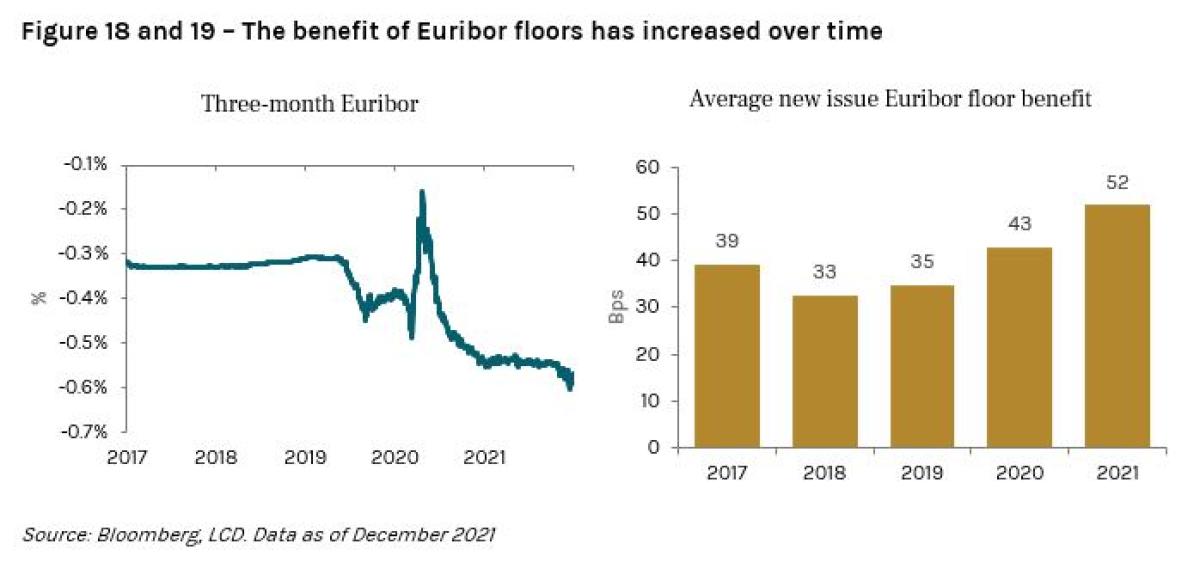

In contrast, the European leveraged loan market has benefitted from this dynamic given the fact that 97% of the asset class has a Euribor floor of 0% or above, which effectively removes the impact of negative rates across the asset class. The benefit these floors have provided compared to incorporating a negative rate into the all-in yield has increased as Euribor has fallen deeper into negative territory over time (Figure 18 and 19).

Well-positioned for rising rates:

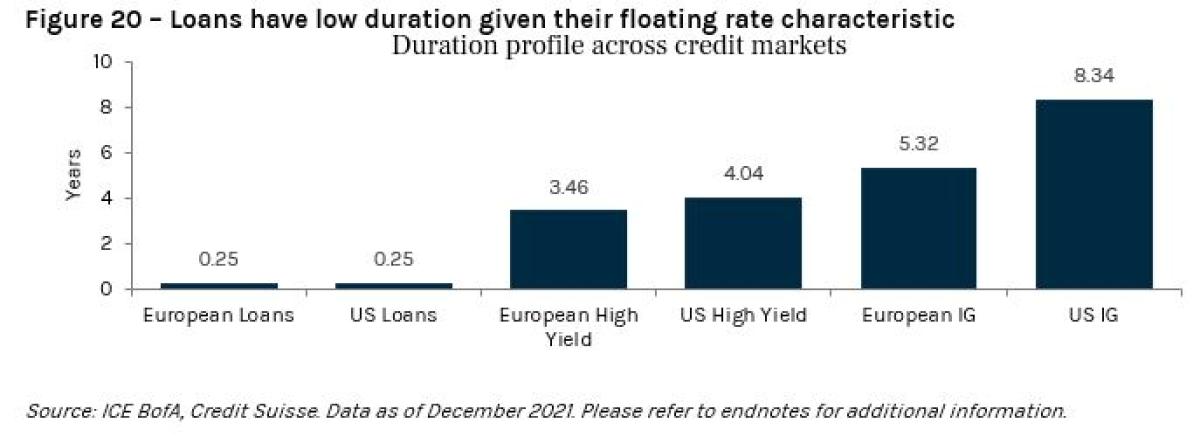

Duration measures the sensitivity of a given asset class to movements in interest rates. As depicted in Figure 20, European leveraged loans have a duration that is significantly below that of bond markets attributable to their floating rates that typically adjust every three months based on Euribor.

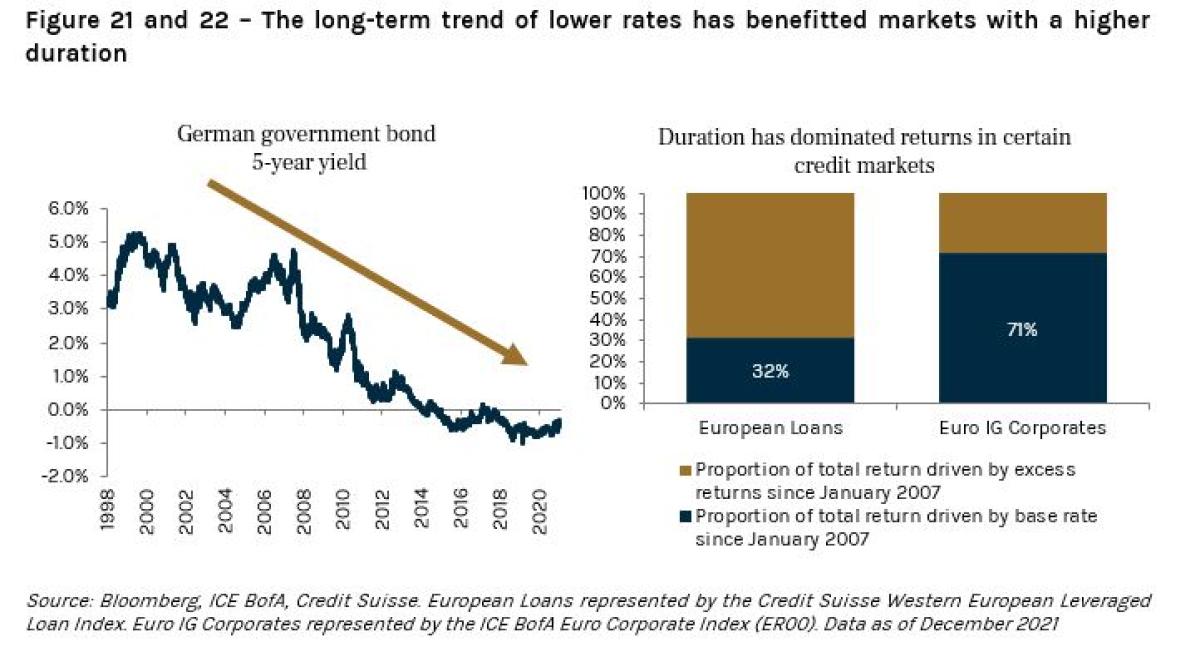

Certain fixed income asset classes have benefitted from having a relatively high duration profile and the capital appreciation uplift that has come from interest rates moving consistently lower over the past few decades (Figure 21). For example, over 70% of the total return from European IG corporates has been driven by base rates over the past 15 years compared to around 30% in the loan market (Figure 22).

With interest rates near historic lows, and in many cases tracking in negative territory, bonds are unlikely to receive the same level of performance uplift from duration going forward, while the downside risk of rising rates will remain a prominent theme. The low duration profile of the European leveraged loan market will ensure the asset class is shielded from rising rates. Moreover, we believe loan valuations stand to benefit if Euribor moves back into positive territory given that yields will periodically adjust upwards, ensuring the underlying “risk-free” rate adequately compensates investors as compared to other segments of the credit market.

Shifting market dynamics that investors should be aware of

It is important to note that the asset class has seen some compositional changes in recent years that may lead some investors to question whether the return profile will be impacted going forwards. Some of the most noteworthy changes include the rise in covenant-lite (“cov-lite”) loans as well as the impact of environmental, social and governance factors becoming increasingly important to market participants.

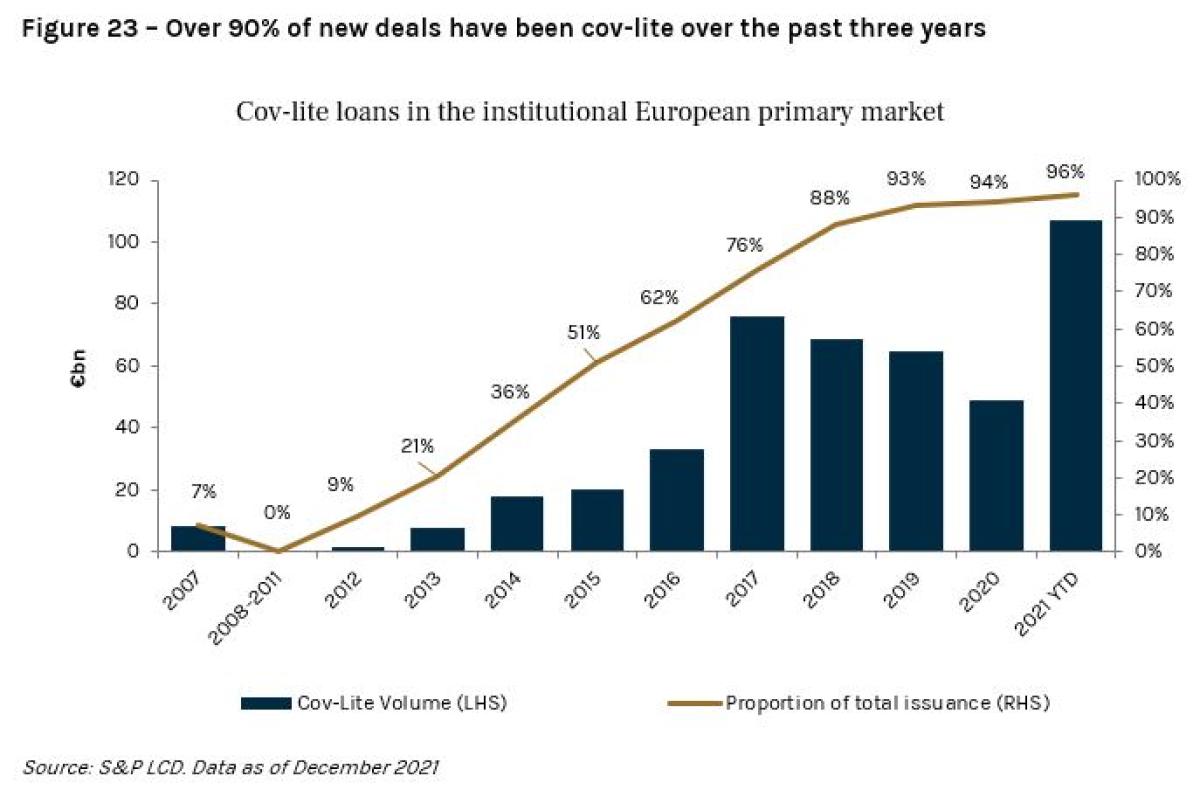

The prevalence of covenant-lite loans:

A discussion on the leveraged loans market would not be complete without addressing the compositional shift to cov-lite loans. This dynamic first became prominent in 2013 and has since fast become the norm within the asset class – this is clearly evidenced within the primary market in which over 90% of new deals over the past three years have come with cov-lite structures (Figure 23).

It is important to note that cov-lite does not mean that loans have simply disposed of their covenants. This label indicates that a given loan does not have maintenance covenants, but instead is likely to have incurrence covenants. Maintenance covenants require the borrower to maintain a certain level of activity. For instance, an issuer may have a maintenance covenant that requires net leverage (Total Debt less Cash/EBITDA) to be less than 6x, tested on a quarterly basis. If the test fails, the issuer incurs a default on their debt. Incurrence covenants, which have traditionally been found in the high yield bond market, are now a common feature of cov-lite loans. Incurrence covenants provide the issuer with more flexibility as the covenant is not tested on a periodic basis and will only take effect when an issuer takes a specific action. For example, an issuer’s incurrence covenant may

require that net leverage must be below 6x if a borrower wants to issue new debt. A default would only occur if new debt is issued while the net leverage ratio was above the stated limit.

Hence, maintenance covenants generally provide the lender with more protection for their investment. However, it is worth highlighting that the shift to a cov-lite environment also has its benefits. For example, if an issuer defaults on their debt due to failing a maintenance covenant, management time and company resources are steered away from improving business operations and may become more focused on addressing the default. Company resources may also be put towards executing a covenant waiver – something which can be a timely and bureaucratic process. The removal of these covenants allows management to concentrate on navigating through what could be a temporary downturn, which could ultimately enhance the fortunes/financial position of the company and allow the lender to potentially recover 100% of their initial investment.

As a result of the shift to cov-lite, the asset class is likely to support lower default rates as borrowers are afforded more flexibility to avoid covenant-related defaults, also known as technical defaults. For defaults experienced going forward, the recovery rates will potentially be lower than those seen historically as the default is more likely to be linked to a more severe debt servicing default (e.g., missing payments on interest or principal payments), rather than a technical default. However, as highlighted earlier in this paper, it is notable that European loan recoveries have moved higher despite the increasing prevalence of cov-lite loans.

Growing focus on Environmental Social and Governance (“ESG”) considerations:

Similar to most asset classes across the financial markets, Environmental, Social and Governance (“ESG”) factors have become increasingly emphasized in the European leveraged loan market for both borrowers and lenders.

Regarding the composition of the asset class, European leveraged loans exhibit various characteristics that are beneficial to the investor who is mindful of sustainable investing. For example, the asset class has a very low exposure to the energy and transportation sectors (0.41% and 2.7% respectively) and hence businesses that are associated with high carbon footprints. Additionally, the market is weighted towards sectors that are generally associated with a lower carbon footprint such as telecoms, technology and services (~35% of market on aggregate).

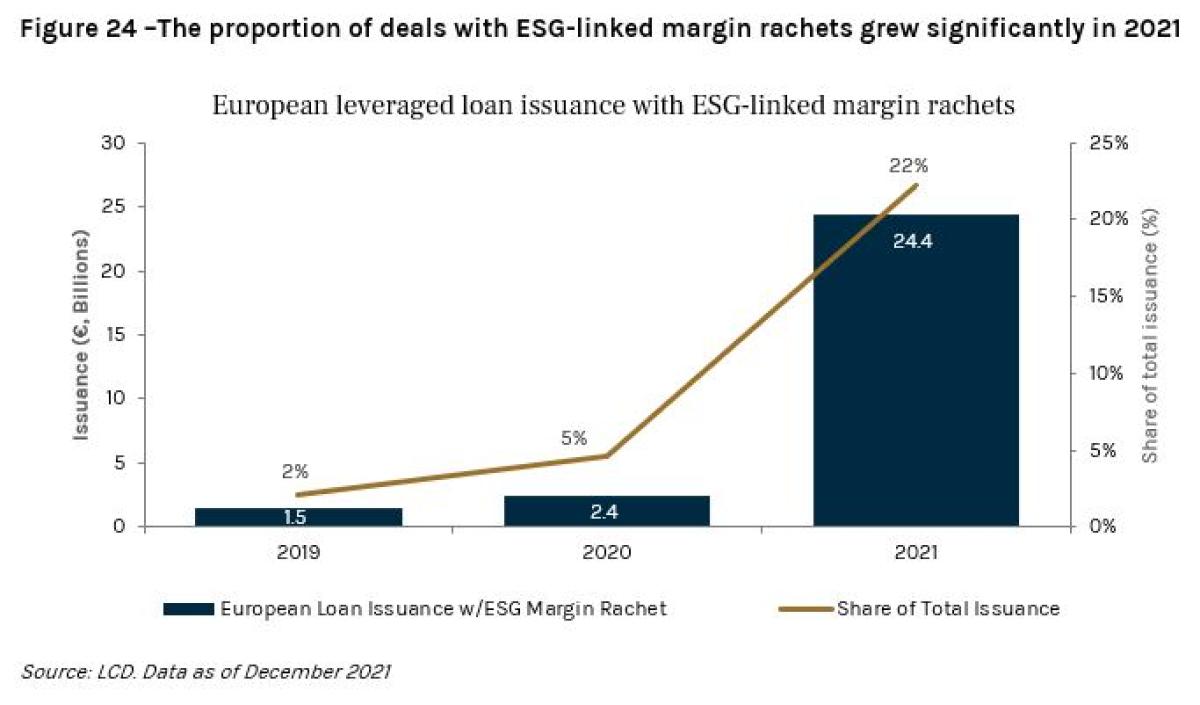

A notable theme within the asset class over the past year has been the increasing proportion of leveraged loans with ESG-linked margin rachets. These are a dynamic mechanism to improve disclosure and to incentivize issuers to achieve certain defined ESG performance targets. A margin rachet will either increase or decrease the coupon that a loan issuer is required to pay based on achieving a particular set of objectives. The rachets increase the frequency of ESG data collection (typically annually) and in some cases the interest cost savings (if the margin ratchets down) are deployed into further ESG initiatives. ESG-linked margin rachets will typically increase or decrease the coupon by 5.0 to 7.5bps and the objectives will vary depending on the sector that the issuer operates within. Examples include:

- increase third party ESG rating;

- reduce Scope 1 and Scope 2 greenhouse gas emissions;

- reduce accident rate per hours worked; and

- reduce amount of non-recyclable materials used in product packaging.

During 2019 and 2020, respectively, 2% and 5% of the total European leveraged loan issuance came with an ESG-linked margin rachet. However, 2021 saw a significant increase, with €24.5 billion of loan supply containing ESG-linked margin rachets – this equates to 22% of total volumes (figure 24).

Investors in leveraged loans have also undertaken measures to formalise the way in which they consider ESG factors. For instance, leveraged loan managers may explicitly:

- exclude sectors according to their responsible investment policy;

- apply ESG ratings to identify the highest and lowest ranked names within portfolios and across the opportunity set; or

- formally engage with issuers requesting more specific ESG disclosures related to their industry and take a proactive voice to help promote ESG-related objectives.

Finally, as mentioned earlier in this paper, the majority of deals that come to the European leveraged loan market are from companies backed by private equity sponsors. Most private equity managers are responding to the demands of their underlying investors and developing ESG best practices that can be implemented across their portfolio companies through engagement with senior management. Over time, these measures, combined with demands from lenders in the leveraged loan community and regulatory frameworks – such as the Sustainable Finance Disclosure Regulation and the Task Force on Climate-Related Financial Disclosures – should lead to more formalised sustainability objectives and an improvement in the level of disclosures on ESG related data that can ultimately be used for leveraged loan investor due diligence and third party ESG ratings.

The rise of cov-lite loans and an ever-increasing focus on ESG has led to a significant shift in the asset class composition, and in the case of ESG, should continue to drive change in the market in

the years ahead. Even though these changes are expected to remain in place, we believe that they will have a limited impact on the risk-adjusted return profile of the European leveraged loan market and could potentially have a positive impact to the investment experience.

The European leveraged loan market has become a distinct asset class within the financial markets, with an increasingly liquid and diverse range of underlying issuers that provide investors with access to secured debt. The market has a robust track record for producing consistent returns, coupled with relatively low levels of volatility, and we believe it is well placed to continue this trend when considering relative valuations and the ownership composition.

The attractive risk-adjusted profile has been buoyed by improving default and recovery trends, which could be explained in part by the maturation of the asset class. An elevated position in the capital structure, the composition of the asset class from a sector standpoint as well as a diversified opportunity set are also supportive of credit performance. The rate structure of European leveraged loans has also bolstered the risk-adjusted return profile. Unlike bonds, loans are protected from the downside risk of rising interest rates, while the advent of Euribor floors ensures that the impact of negative rates can be largely mitigated. The prevalence of cov-lite loans has arguably provided issuers with a higher degree of financial flexibility at the expense of the lender. However, the additional flexibility could provide attractive outcomes for both parties, as covenant structures are brought more in line with those seen in the high yield bond market. Finally, ESG has become an increasingly important feature of investing in the asset class, with both leveraged loan issuers and investors taking steps to formally address this topic, as evidenced by the significant increase in leveraged loans with ESG-linked margin rachets and in the formal incorporation of ESG factors into the investment process.

By adding the benefits of diversification, and potentially boosting risk-adjusted returns, we believe these features make a strong case for investing in European leveraged loans as a distinct core holding within a broader, diversified portfolio.

Footnotes:

- Source: ICE BofA, Credit Suisse, Bloomberg. Data covers ten years to December 2021. See Endnotes for additional information.

- Source: Credit Suisse. Data as of December 2021. European loan represented by the Credit Suisse Western European Leveraged Loan Index.

- Source: Credit Suisse. Data as of December 2021. European loan metrics are superior when compared to European high yield, U.S. high yield and U.S. loans

About the Authors:

Boris Okuliar is a Partner in the Ares Credit Group, and Portfolio Manager and Co-Head of Global Liquid Credit.

He serves as a member of the Ares Credit Group's European Liquid Credit and European Direct Lending Investment Committees, as well as a member of the Global Asset Allocation Committee. Prior to joining Ares in 2016, Mr. Okuliar was a Managing Director and Head of Capital Markets for Global Market Strategies at The Carlyle Group, where he focused on sourcing credit investment opportunities from banks and sponsors, syndicating excess risk, and developing new business opportunities. Previously, Mr. Okuliar was Head of Leveraged Capital Markets for UBS, where he focused on the structuring and market execution of leveraged loans, bridge financing and high yield bond placements. In addition, Mr. Okuliar was Head of High Yield Capital Markets and Syndicate at Barclays Capital in London. He has also worked for Banc of America Securities in Syndicated Finance and High Yield Capital Markets in the U.S. and London. Mr. Okuliar holds a B.S.B.A. from Georgetown University with a double major in Finance and International Business, and is a graduate of the Advanced Management Program at Harvard Business School.

Brian Abdelhadi is a Partner and Portfolio Manager in the Ares Credit Group and serves as a member of the Ares Credit Group's European Liquid Credit Investment Committee.

Prior to joining Ares in 2020, Mr. Abdelhadi was a Senior Portfolio Manager in the Global Fixed Income Group at Allianz Global Investors, where he managed global high yield and multi-asset credit portfolios across a broad range of strategies. Previously, Mr. Abdelhadi was an Analyst at Camares Capital, where he focused on relative value, catalyst-driven and capital structure arbitrage credit opportunities. He also held high yield analyst positions at Citigroup and Barclays. Mr. Abdelhadi holds a B.S. from DePaul University in Accounting and an M.B.A. from the University of Navarra, Instituto de Estudios Superiores de la Empresa (IESE Business School).

Elliot Hill is a Vice President in the Ares Investor Relations Group, where he focuses on credit investor relations.

Prior to joining Ares in 2020, Mr. Hill was an Investment Specialist in the Global Credit Strategy Group at J.P. Morgan Asset Management, where he focused on all client matters related to the asset class including new business generation and mandate retention. Mr. Hill holds a B.A. from The University of Exeter in Economics. Mr. Hill is a CFA® charterholder.

Executive Summary and Figure 3 - Source: ICE BofA, Credit Suisse, Bloomberg. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. US Loans represented by the Credit Suisse Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). US High Yield represented by the ICE BofA US High Yield Constrained Index (HUC0). Emerging Market Corporates represented by the ICE BofA Emerging Markets Diversified Corporate Index (EMSD). European Equities represented by the Euro Stoxx 50 Index. US Equities represented by the S&P 500 Index. Data as of December 2021

Figure 4 - Source: ICE BofA, Credit Suisse, Bloomberg. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. US Loans represented by the Credit Suisse Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). US High Yield represented by the ICE BofA US High Yield Constrained Index (HUC0). Emerging Market Corporates represented by the ICE BofA Emerging Markets Diversified Corporate Index (EMSD). European Equities represented by the Euro Stoxx 50 Index. US Equities represented by the S&P 500 Index. Data as of December 2021

Figure 5 - Source: ICE BofA, Credit Suisse, Bloomberg. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. US Loans represented by the Credit Suisse Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). US High Yield represented by the ICE BofA US High Yield Constrained Index (HUC0). Emerging Market Corporates represented by the ICE BofA Emerging Markets Diversified Corporate Index (EMSD). European Equities represented by the Euro Stoxx 50 Index. US Equities represented by the S&P 500 Index. Data as of December 2021

Figure 6 - Source: ICE BofA, Credit Suisse. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. US Loans represented by the Credit Suisse Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). US High Yield represented by the ICE BofA US High Yield Constrained Index (HUC0). Euro IG Corporates represented by the ICE BofA Euro Corporate Index (ER00). US IG Corporates represented by the ICE BofA US Corporate Index (C0A0). Loan indices use the 3yr yield, bond indices use the yield to worst. Data as of December 2021

Figure 8 and 9 - Source: Credit Suisse. European Loans represented by the Credit Suisse Western European Leveraged Loan Index (“CSWELLI”) and U.S. Loans represented by the Credit Suisse Leveraged Loan Index (“CSLLI”). Distressed exchanges included in default rate calculation. European High Yield is represented by the Credit Suisse Western European High Yield Index and US High Yield is represented by the Credit Suisse US High Yield Index. Distressed exchanges included in default rate calculation. Data as of December 31, 2021.

Figure 17 - Source: ICE BofA, Credit Suisse. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). Euro IG Corporates represented by the ICE BofA Euro Corporate Index (ER00). Loan indices use the 3yr yield and 3yr discount margin, while bond indices use the yield to worst and option adjusted spread when calculating the yield composition. The risk-free rate includes the impact of the FX hedge. Data as of December 2021

Figure 20 - Source: ICE BofA, Credit Suisse. European Loans represented by the Credit Suisse Western European Leveraged Loan Index. US Loans represented by the Credit Suisse Leveraged Loan Index. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0). US High Yield represented by the ICE BofA US High Yield Constrained Index (HUC0). Euro IG Corporates represented by the ICE BofA Euro Corporate Index (ER00). US IG Corporates represented by the ICE BofA US Corporate Index (C0A0). Data as of December 2021

Index Definitions

The Credit Suisse Leveraged Loan Index (“CSLLI”) is designed to mirror the investable universe of the $US-denominated leveraged loan market. The index inception is January 1992. The index frequency is daily, weekly and monthly. New loans are added to the index on their effective date if they qualify according to the following criteria: 1) Loan facilities must be rated “5B” or lower. That is, the highest Moody’s/S&P ratings are Baa1/BB+ or Ba1/BBB+. If unrated, the initial spread level must be Libor plus 125 basis points or higher. 2) Only fully-funded term loan facilities are included. 3) The tenor must be at least one year. 4) Issuers must be domiciled in developed countries; issuers from developing countries are excluded.

The Credit Suisse Western European Leveraged Loan Index (“CSWELLI”) is designed to mirror the investable universe of the leveraged loan market of issues which are denominated in US$ or Western European currencies. The issuer has assets located in or revenues derived from Western Europe, or the loan represents assets in Western Europe, such as a loan denominated in a Western European currency. Loan facilities must be rated “5B” or lower. That is, the highest Moody’s/S&P ratings are Baa1/BB+ or Ba1/BBB+. Only fully funded term loan facilities are included and the tenor must be at least one year. Minimum outstanding balance is $100 million and new loans must be priced by a third-party vendor at month-end. The index inception is January 1998.

The ICE BofA US High Yield Master II Constrained Index (“HUC0”) contains all securities in The ICE BofA US High Yield Master II Index but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%. Issuers that exceed the limit are reduced to 2% and the face value of each of their bonds is adjusted on a pro-rata basis. Similarly, the face values of bonds of all other issuers that fall below the 2% cap are increased on a pro-rata basis. In the event there are fewer than 50 issuers in the Index, each is equally weighted and the face values of their respective bonds are increased or decreased on a prorata basis. Accrued interest is calculated assuming next-day settlement. Cash flows from bond payments that are received during the month are retained in the index until the end of the month and then are removed as part of the rebalancing. Cash does not earn any reinvestment income while it is held in the Index. The Index is rebalanced on the last calendar day of the month, based on information available up to and including the third business day before the last business day of the month. Issues that meet the qualifying criteria are included in the Index for the following month. Issues that no longer meet the criteria during the course of the month remain in the Index until the next month-end rebalancing at which point they are removed from the Index.

The ICE BofA European Currency High Yield Constrained Index (HPC0) contains all securities in The BofA European Currency High Yield Index but caps issuer exposure at3%. Index constituents are capitalization weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 3%. Issuers that exceed the limit are reduced to 3% and the face value of each of their bonds is adjusted on a pro-rata basis. Similarly, the face values of bonds of all other issuers that fall below the 3% cap are increased on a pro-rata basis. In the event there are fewer than 34 issuers in the Index, each is equally weighted and the face values of their respective bonds are increased or decreased on a pro-rata basis. Inception date: December 31, 1997.

ICE BofA Euro Corporate Index (ER00) tracks the performance of EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch) and at least 18 months to final maturity at the time of issuance. In addition, qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of EUR 250 million. Original issue zero coupon securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. Fixed-to-floating rate securities also qualify provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Contingent capital securities (“cocos”) are excluded, but capital securities where conversion can be mandated by a regulatory authority, but which have no specified trigger, are included. Other hybrid capital securities, such as those issues that potentially convert into preference shares, those with both cumulative and non-cumulative coupon deferral provisions, and those with alternative coupon satisfaction mechanisms, are also included in the index. Euro legacy currency, equity-linked and securities in legal default are excluded from the Index. Securities issued or marketed primarily to retail investors do not qualify for inclusion in the index. Index constituents are market capitalization weighted. Accrued interest is calculated assuming next-day settlement. Cash flows from bond payments that are received during the month are retained in the index until the end of the month and then are removed as part of the rebalancing. Cash does not earn any reinvestment income while it is held in the index. Information concerning constituent bond prices, timing and conventions and index governance and administration is provided in the ICE BofA Bond Index Methodologies, which can be accessed on our public website (https://indices.theice. com), or by sending a request to iceindices@theice.com. The index is rebalanced on the last calendar day of the month, based on information available up to and including the third business day before the last business day of the month. New issues must settle on or before the calendar month end rebalancing date in order to qualify for the coming month. No changes are made to constituent holdings other than on month end rebalancing dates. Inception date: December 31, 1995

ICE BofA US Corporate Index (C0A0) tracks the performance of US dollar denominated investment grade corporate debt publicly issued in the US domestic market. Qualifying securities must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), at least 18 months to final maturity at the time of issuance, at least one year remaining term to final maturity as of the rebalancing date, a fixed coupon schedule and a minimum amount outstanding of $250 million. Original issue zero coupon bonds, 144a securities (with and without registration rights), and pay-in-kind securities (including toggle notes) are included in the index. Callable perpetual securities are included provided they are at least one year from the first call date. Fixed-to-floating rate securities are included provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Contingent capital securities (“cocos”) are excluded, but capital securities where conversion can be mandated by a regulatory authority, but which have no specified trigger, are included. Other hybrid capital securities, such as those issues that potentially convert into preference shares, those with both cumulative and non-cumulative coupon deferral provisions, and those with alternative coupon satisfaction mechanisms, are also included in the index. Equity-linked securities, securities in legal default, hybrid securitized corporates, eurodollar bonds (USD securities not issued in the US domestic market), taxable and tax-exempt US municipal securities and $1000 par preferred and DRD-eligible securities are excluded from the index. Index constituents are market capitalization weighted. Accrued interest is calculated assuming next-day settlement. Cash flows from bond payments that are received during the month are retained in the index until the end of the month and then are removed as part of the rebalancing. Cash does not earn any reinvestment income while it is held in the index. Information concerning constituent bond prices, timing and conventions and index governance and administration is provided in the ICE BofA Bond Index Methodologies, which can be accessed on our public website (https://indices.theice. com), or by sending a request to iceindices@theice.com. The index is rebalanced on the last calendar day of the month, based on information available up to and including the third business day before the last business day of the month. New issues must settle on or before the calendar month end rebalancing date in order to qualify for the coming month. No changes are made to constituent holdings other than on month end rebalancing dates. Inception date: December 31, 1972

The Standard & Poor's 500 (“Domestic”), often abbreviated as the S&P 500, or just "the S&P", is an American stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices.

The Euro STOXX 50 Index is a market capitalization-weighted stock index of 50 large, blue-chip European companies operating within Eurozone nations. Components are selected from the Euro STOXX Index, which includes large-, mid- and small-cap stocks in the Eurozone.

ICE BofA Emerging Markets Diversified Corporate Index (“EMSD”) tracks the performance of US dollar denominated emerging markets corporate senior and secured debt publicly issued in the US domestic and eurobond markets. In order to qualify for inclusion in the Index an issuer must have primary risk exposure to a country other than a member of the FX G10, a Western European country, or a territory of the US or a Western European country. The FX-G10 includes all Euro members, the US, Japan, the UK, Canada, Australia, New Zealand, Switzerland, Norway and Sweden. Individual securities of qualifying issuers must be denominated in US dollars, must be senior or secured debt, must have at least one year remaining term to final maturity a fixed coupon and at least $500 million in outstanding face value. Qualifying securities must have at least 18 months to final maturity at the time of issuance. The index includes corporate debt of qualifying countries, but excludes sovereign, quasi-government, securitized and collateralized debt. Original issue zero coupon bonds 144a securities, both with and without registration rights, and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. Fixed-to-floating rate securities also qualify provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Securities rated Ca/CC or lower by any of the three rating agencies do not qualify for inclusion. Contingent capital securities (“cocos”) are excluded, but capital securities where conversion can be mandated by a regulatory authority, but which have no specified trigger, are included. Other hybrid capital securities, such as those issues that potentially convert into preference shares, those with both cumulative and non-cumulative coupon deferral provisions, and those with alternative coupon satisfaction mechanisms, are also included in the index. Securities issued or marketed primarily to retail investors do not qualify for inclusion in the index. Equity-linked securities, securities in legal default and hybrid securitized corporates are excluded from the index. Index constituents are market capitalization weighted, subject to a 5% issuer cap. Issuers that exceed the limits are reduced to 5%, and the face value of each of their bonds is adjusted on a pro-rata basis. Similarly, the face values of bonds of all other issuers that fall below the cap are increased on a pro-rata basis. In the event there are fewer than 20 issuers, each is equally weighted and the face values of their respective bonds are increased or decreased on a pro-rata basis. Inception date: December 31, 2004.

Endnotes

1 Source: Credit Suisse. Data as of December 2021. European Loans represented by the Credit Suisse Western European Leveraged Loans Index. US Loans represented by the Credit Suisse Leveraged Loan Index. Both indices are hedged to EUR.

2 Source: Credit Suisse. Data as of December 2021. European Loans represented by the Credit Suisse Western European Leveraged Loans Index.

3 Source: ICE BofA. Data as of December 2021. European High Yield represented by the ICE BofA European Currency high Yield Constrained Index (HPC0).

5 Source: S&P LCD. Data as of November 2021

6 References to “downside protection” or similar language are not guarantees against loss of investment capital or value.

7 Diversification does not assure profit or protect against market loss.

Disclaimer

These materials are not an offer to sell, or the solicitation of an offer to purchase, any security, the offer and/or sale of which can only be made by definitive offering documentation. Any offer or solicitation with respect to any securities that may be issued by any investment vehicle (each, a “Fund”) managed or sponsored by Ares Management LLC, Ares Management Limited (“AML”) or Ares Management UK Limited (“AMUKL”) (AML and AMUKL are each a wholly owned subsidiary of Ares Management LLC and together with Ares Management LLC, are “we” or “Ares Management”) and/or one of Ares Management LLC's affiliated entities will be made only by means of definitive offering memoranda, which will be provided to prospective investors and will contain material information that is not set forth herein, including risk factors relating to any such investment. Any such offering memoranda will supersede these materials and any other marketing materials (in whatever form) provided by Ares Management to prospective investors. In addition, these materials are not an offer to sell, or the solicitation of an offer to purchase securities of Ares Management Corporation (“Ares Corp”), the parent of Ares Management. An investment in Ares Corp is discrete from an investment in any fund directly or indirectly managed by Ares Management. Collectively, Ares Corp, its affiliated entities, all of Ares Corp’s underlying subsidiary entities including Ares Management, and the Funds shall be referred to as “Ares” unless specifically noted otherwise. The Recipient (as defined below) acknowledges and agrees to the following:

By acceptance of this presentation, the recipient, including , without limitation, its legal and financial advisors, board members and/or trustees, as applicable (collectively, along with anyone else who receives this presentation through the person to whom they were originally delivered, the “Recipient”), hereby acknowledges and agrees that information included in the presentation includes confidential and proprietary information (“Confidential Information”) that is not otherwise publicly available or otherwise prepared for public dissemination and is subject to any other confidentiality provisions between the Recipient and Ares (including, if applicable, the limited partnership agreement(s) of any Fund(s) described herein). The distribution or the divulgence of any of these materials to any person, other than the person to whom they were originally delivered and such person's advisors, without the prior consent of Ares, is prohibited. The Recipient agrees to use this presentation solely in connection with its evaluation of the relevant Ares entity and not for any other purpose. Moreover, some of the Confidential Information is based on information provided to Ares in accordance with underlying confidentiality agreements and/or prepared by referenced portfolio companies for Ares respecting Ares’ (portfolio) investment in such company; as such no representations are made to the completeness and/or accuracy of the Confidential Information. In any event, in light of the confidential nature of such information, the Recipient further acknowledges and understands that disclosure of such Confidential Information and/or any other unauthorised use thereof may result in potential damages to and claims by Ares and/or the applicable portfolio company. Accordingly, the Recipient agrees to maintain the confidential nature of the Confidential Information and limit its use accordingly solely in connection with the purpose for which this presentation was prepared and the relevant Ares entity referred to herein. The Recipient further agrees that damages due a breach of the foregoing, including misuse and/or other publication of the Confidential Information , may be difficult to determine and that Ares (and/or potentially the subject portfolio company, as applicable) may be entitled to injunctive relief and other equitable remedies.

The information contained herein has been prepared to assist the Recipient in making its own evaluation of Ares or the relevant Ares entity and does not purport to be all inclusive or to contain all of the information that the Recipient may desire respecting its evaluation of the same. These materials are not intended as an offer to sell, or the solicitation of an offer to purchase, any security, the offer and/or sale of which can only be made by definitive offering documentation.

Any subscription in relation to any Fund will only be accepted on the basis of definitive offer documentation (the “Agreements”) which may be issued to a prospective investor on a confidential basis upon request. Any information contained in these materials relating to the terms and conditions of any Fund will be superseded, and is qualified in its entirety, by reference to the Agreements, which should be reviewed for complete information concerning the rights, privileges and obligations of investors in any Fund. These materials contain information about Ares and certain of its personnel and affiliates and the historical performance of certain Funds and/or investment vehicles whose portfolios are managed by Ares. This information is supplied to provide information as to Ares’ general portfolio management experience. Ares makes no representation or warranty (express or implied) with respect to the information contained herein (including, without limitation, information obtained from third parties) and expressly disclaims any and all liability based on or relating to the information contained in, or errors or omissions from, these materials; or based on or relating to the Recipient’s use of these materials; or any other written or oral communications transmitted to the Recipient in the course of its evaluation of Ares.

The Recipient should conduct its own investigations and analyses of Ares and the information set forth in these materials.

These materials are not being provided to the UK public. They are only intended for: (i) investment professionals falling within Article 14(5) of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 (the “CIS Promotion Order”) and/or (as applicable) article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “General Promotion Order”) or (ii) persons who are high net worth companies, unincorporated associations, partnerships or trusts falling within any of the categories of persons described in Article 22 of the CIS Promotion Order and/or (as applicable) Article 49 of the General Promotion Order or (iii) any other person to whom they may otherwise be lawfully distributed in accordance with the CIS Promotion Order, the General Promotion Order or COBS 4 of the FCA Handbook of Rules and Guidance. Persons of any other description in the United Kingdom may not receive, and should not act or rely on, these materials. Potential investors in the United Kingdom are hereby notified that certain protections afforded by the United Kingdom regulatory system will not apply to an investment in the Fund and only investors who qualify as “eligible claimants” for the purposes of the UK Financial Services Compensation Scheme may be entitled to compensation.

Within the European Economic Area (the “EEA”) interests in a fund which qualifies as an alternative investment fund within the meaning of the European Union Alternative Investment Fund Managers Directive 2011/61/EU may only be marketed to professional investors or any other person to whom such interests may be lawfully marketed, and information in relation to such interests may only be distributed to persons to whom they may lawfully be distributed. In this regard a professional investor is every investor that is considered, or may be treated based on a request made to Ares, as a professional client within the meaning of Annex II of the Markets in Financial Instruments Directive (2014/65/EU). Accordingly, the distribution of these materials is restricted to professional investors and others who may lawfully receive them. Persons of any other description may not receive and should not rely on these materials or any other materials relating to a Fund.

It is expected that interests in any Fund will not be registered under the laws of any jurisdiction, including the U.S. Securities Act of 1933, as amended (the “Securities Act”). It is expected that interests in any Fund will be offered for investment only to “accredited investors” pursuant to the exemption from the registration requirements of the U.S. Securities Act provided by Section 4(2) and Regulation D or to non-U.S. persons pursuant to the requirements of Regulations, each as promulgated thereunder. It is further expected that the Fund will not be registered as an investment company under the U.S. Investment Company Act of 1940, as amended.

Nothing in these materials should be construed as a recommendation to invest in any securities that may be issued by any Fund or as legal, accounting, investment or tax advice. Recipients of these materials should also be aware that Ares Management (and its affiliates) are not responsible for providing recipients with the protections afforded to its / their regulatory clients and before making a decision to invest in any Fund, a prospective investor should carefully review information respecting Ares and such Fund and consult with its own legal, accounting, tax and other advisors in order to independently assess the merits of such an investment. These materials are not intended for distribution to, or use by, any person in any jurisdiction or country where such distribution or use would be contrary to law or regulation. These materials contain confidential and proprietary information, and their distribution or the divulgence of any of their contents to any person, other than the person to whom they were originally delivered and such person's advisors, without the prior consent of Ares is prohibited. The Recipient is advised that United States, United Kingdom and other securities laws restrict any person who has material, non-public information about a company from purchasing or selling securities of such company (and option, warrants and rights relating thereto) and from communicating such information to any other person under circumstances in which it is reasonably foreseeable that such person is likely to purchase or sell such securities. The Recipient agrees not to purchase or sell such securities in violation of any such laws.

These materials may contain “forward-looking” information that is not purely historical in nature. The forward-looking information contained herein is based upon certain assumptions about future events or conditions and is intended only to illustrate hypothetical results under those assumptions (not all of which will be specified herein). Not all relevant events or conditions may have been considered in developing such assumptions. The success or achievement of various results and objectives is dependent upon a multitude of factors, many of which are beyond the control of Ares. No representations are made as to the accuracy of such estimates or projections or that such estimates or projections will be realised. Actual events or conditions are unlikely to be consistent with, and may differ materially from, those assumed. Past performance is not indicative of future results. There is no assurance that the Fund will be able to generate returns for its investors (as stated herein or otherwise). A total loss of the investment is possible.

These materials may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content.

THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.

Unless otherwise indicated, the information presented herein is as of the date of this presentation and subject to change. Neither Ares nor any of its Funds, portfolio companies or other affiliates undertakes any duty or obligation to update or revise the information contained herein.

Charts and graphs presented herein are shown for illustrative purposes only.

This may contain information sourced from BANK OF AMERICA, used with permission. BANK OF AMERICA IS LICENSING THE BANK OF AMERICA INDICES AND RELATED DATA “AS IS,” MAKES NO WARRANTIES REGARDING SAME, DOES NOT GUARANTEE THE SUITABILITY, QUALITY, ACCURACY, TIMELINESS, AND/OR COMPLETENESS OF THE BOFA MERRILL LYNCH INDICES OR ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM, ASSUMES NO LIABILITY IN CONNECTION WITH THEIR USE, AND DOES NOT SPONSOR, ENDORSE, OR RECOMMEND ARES MANAGEMENT, OR ANY OF ITS PRODUCTS OR SERVICES.

The outbreak of a novel and highly contagious form of coronavirus (“COVID-19”), which the World Health Organization has declared to constitute a pandemic, has resulted in numerous deaths, adversely impacted global commercial activity and contributed to significant volatility in certain equity and debt markets. The global impact of the outbreak is rapidly evolving, and many countries have reacted by instituting quarantines, prohibitions on travel and the closure of offices, businesses, schools, retail stores and other public venues. Businesses are also implementing similar precautionary measures. Such measures, as well as the general uncertainty surrounding the dangers and impact of COVID-19, are creating significant disruption in supply chains and economic activity and are having a particularly adverse impact on energy, transportation, hospitality, tourism, entertainment and other industries. The impact of COVID-19 has led to significant volatility and declines in the global financial markets and oil prices and it is uncertain how long this volatility will continue. As COVID-19 continues to spread, the potential impacts, including a global, regional or other economic recession, are increasingly uncertain and difficult to assess. Any public health emergency, including any outbreak of COVID-19 or other existing or new epidemic diseases, or the threat thereof, and the resulting financial and economic market uncertainty could have a significant adverse impact on investment portfolios and the value of their investments. The information herein is as of the dates referenced, and not all of the effects, directly or indirectly, resulting from COVID-19 and/or the current market environment may be reflected herein. The full impact of COVID-19 and its ultimate potential effects on portfolio company performance and valuations is particularly uncertain and difficult to predict.