By Ankur Bansal, Executive Director, Blacksoil.

The venture debt model originated in Silicon Valley in the 1970s and has since become an established form of alternative capital that is available to VC backed companies globally. Many well-known technology companies have taken venture debt at some point in their growth journeys including Google, Facebook, Uber, Airbnb etc.

At its core, venture debt is entrepreneur-friendly as it helps founders and cash-hungry startups avoid over-diluting shareholder equity at early stages of a company’s growth. Used appropriately, venture debt can also extend the cash runway between fundraising rounds, sometimes helping companies achieve performance targets set by equity investors (or avoid dreaded valuation down-rounds). Another benefit of venture debt is that, in appropriate instances, it can support companies facing unexpected market turbulence or short-term capital traps as witnessed during covid times.

Factors leading to emergence of Venture Debt

The traditional banking system has several lending criteria that do not apply to startups; things like profitability, business vintage, financial history and sufficient collaterals, with a preference for hard collaterals, personal guarantees, etc.

The turnaround time of traditional banking is also unhelpfully lengthy, while for high-growth companies, timely availability of capital is the key.

Traditional lenders typically have domain expertise limited to traditional businesses and industries, while startups, by their nature, are set up to disrupt the old industries and therefore need to be assessed with a different lens.

While PEVC provides the necessary growth capital for startups to prove their business model and scale up, it’s still an expensive source of capital and leads to dilution of a promoter’s equity. Hence, high growth and cash-hungry startups prefer debt for their working capital requirement or for any specific capex or contract financing requirements. This helps founders to avoid the risk of losing out on richer valuations at the later stage exit options, when the company grows to its full potential.

The cost of the venture debt is also tax deductible, resulting in lower after-tax cost of capital.

Type of Venture Debt Investments

Venture debt can structure financing best suited to a business and its characteristics. Apart from lending against defined repayment structures, venture debt firms prefer to have an option to subscribe to equity of the company to the extent of 10%-15% of the debt amount. The primary objective is to enhance returns through an equity kicker.

Right Time to Avail Venture Debt

Venture debt’s biggest drawback is that it is not readily available to startups that have not done an institutional VC round.

Since most startups are burning cash to scale their business, there is a constant need of equity infusion for various activities including debt repayment. Hence, venture debt is not a replacement for equity. While VC firms bring sector expertise, growth knowledge and are the first line of backers for a startup, venture debt augments this and supports both the founder and the investors through the journey. It is also generally limited to 20% of the equity fundraise.

Therefore, most venture debt firms show interest post the Series A equity round, as by then a startup would have proved its business model and is entering the growth phase. Similarly, a new entrant in the lending industry is Revenue Based Financing, which links repayments with revenue of companies and therefore lends even to Pre-Series A startups.

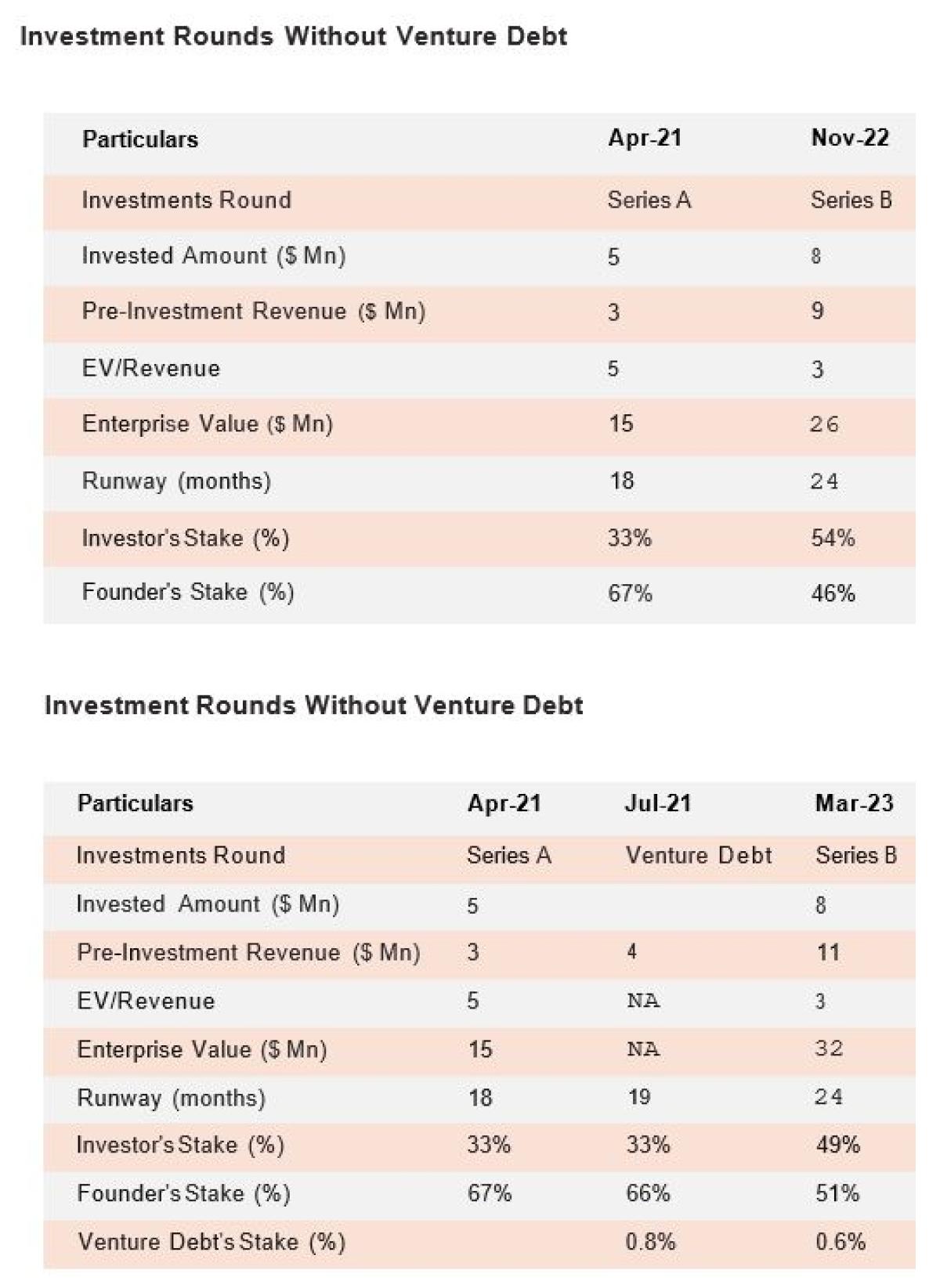

Case Study

A Healthtech startup raised an initial round of angel and seed capital and reached a revenue of $3 million. The company is expecting to grow its revenue at 6% per month on an average, over next few years and is therefore looking to raise further capital.

As can be seen from the above tables, the Healthtech startup clearly has an advantage by using a mix of VD and VC rather than just VC funds. The mix of VD and VC led to the extension of runway of the startup by 4 months (from Nov-22 to Mar-23) and ~5% less dilution of the promoters.

Current Trends in VD

In India, the total amount raised by venture debt funds jumped from $62 million in 2020 to $85 million in 2021. Deals took place across diverse business models and industries such as e-Commerce, Fintech, Consumer Services, EdTech and SaaS. In Q1 2021, startups raised $91 million through venture debt financing, hitting a 25-quarter high. In CY21, venture debt financings were estimated to have grown by 40% year-on-year.

Some of the key benefits of Venture Debt over Venture Capital are:

- Debt Financing is cheaper than equity

- Debt allows to maintain control over businesses

- Cost of Debt is Tax Deductible resulting in lower after-tax cost of capital

- Debt can be made available faster than equity, as equity investment takes longer due to in depth diligence

Impact of Covid on Venture Debt:

Startups are not sheltered from the disruptions caused by the Covid-19 pandemic. Many had to turn conservative in their operations when the first wave hit. As a result, the VD industry saw a boom during this period and came into the limelight as an asset class both for investors and borrowers.

Deal flow increased for venture debt firms, though only the startups with a strong business model, high capital efficiency and some degree of profitability were able to raise the required capital. Trending businesses sectors such as SaaS, e-Commerce, Gaming, Agri-Tech, Med-Tech, Ed-Tech & Logistics found it relatively easy to raise debt funding, due to the efficient tech play and tailwinds from Covid-19. Overall based on market reports, there was a doubling of venture debt funding from $217 million in 2019 to $427 million in 2020.

The pandemic has left a long-lasting impact on the way businesses is done. For some companies Covid-19 has been a blessing in disguise and they enhanced their business substantially on the back of technology. Others, especially in bricks-and-mortar businesses, felt the most heat and have had to resort to cutting cost, or even shutting up shop.

If you enjoyed this article, be sure to read CAIA Association’s new report, The Rise of India’s Private Equity Market.

About the Author:

Ankur Bansal is Co-Founder & Director of BlackSoil Group, which is a new-age venture debt platform also focused on structured and real estate debt. With over 15 years of experience in idea origination, credit, M&A execution, investment thesis, commercial negotiations, and post-deal investment management.

Under his leadership, Blacksoil Group has made credit disbursements of over INR 1,650 Crs across 110+ transactions with 60+ notable exits at an average IRR of 18%. Blacksoil has provided INR 1,160+ Crs across 90+ growth and VC backed companies, such as - Oyo Rooms, Infra.Market, Zetwerk, Udaan, Koye Pharma, Furlenco, Purplle, EarlySalary, BTI Payments, Chumbak, Homelane, etc.

Previously, Ankur was employed with J P Morgan investment banking, Mumbai. He was also associated with Citi Group where he completed multiple complex capital market transactions encompassing equity, equity linked and retail bond deals across formats like IPO, QIP, FCCBs, block trades etc.

Ankur's academic background includes a degree from the Institute of Chartered Accountants of India, Chartered Financial Analyst (CFA) Institute and graduation from Narsee Monjee College of Commerce and Economics.