By Nicolas Rabener, CAIA, of FactorResearch (@FactorResearch) INTRODUCTION John Maynard Keynes famously asked, “When the facts change, I change my mind—what do you do, sir?” If this question was directed at global pension funds and their fixed income allocation, then the answer would have to be, “Not much.” Their average allocation to bonds was approximately 30% in 2020, almost identical to 1999, according to a study by the Thinking Ahead Institute. Over that 20-year period, global bond yields decreased significantly. The U.S. 10-year government bond yield fell from 5% to a mere 1.5% currently. Given that the expected return of a bond is highly related to its starting yield, this had made fixed income in the U.S. less attractive and unattractive in Europe and Japan where yields are negative. The facts have changed, so why not allocations? Furthermore, public and corporate leverage is at peak levels, which reduces long-term economic growth and ultimately the ability of borrowers to repay debt, making bonds riskier. In this short research note, we will explore replacing the traditional 40% allocation to bonds with liquid alternatives from the perspective of creating an anti-fragile portfolio. BONDS VERSUS LIQUID ALTERNATIVES Upfront, it is unlikely that there is a great alternative for bonds, at least from a historical perspective. Bonds have been in a bull market since the 1980s and generated exceptionally high risk-adjusted returns over that period. However, the past is the past and investors need to consider the bleak outlook for the asset class. Investors have started shifting allocations, and the main beneficiaries are private asset classes like real estate, private equity, or infrastructure. Unfortunately, none of these private asset classes represent true diversifiers for an equity portfolio as they, like stocks, depend on positive economic growth. On paper, they may seem to offer diversification benefits, but that is simply due to smoothened and lagged valuations of private assets. Given this, we are going to evaluate liquid alternative strategies that potentially offer truly uncorrelated returns. Specifically, we focus on three strategies that are backed by academic research and are available via liquid alternative mutual funds or ETFs.

- Managed futures, also known as trend-following funds or CTAs, represented via the SG Trend Index.

- Multi-factor market-neutral strategy, providing exposure to five equity factors, namely value, size, momentum, low volatility, and quality.

- Long volatility strategy, a simple combination of JPY / AUD and gold, which represent safe-haven instruments and closely replicated the performance of the CBOE Eurekahedge Long Volatility Hedge Fund Index.

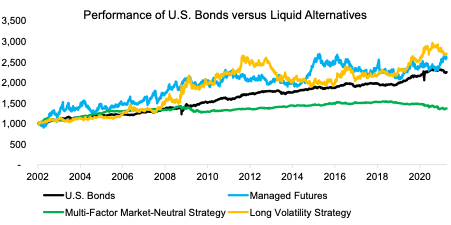

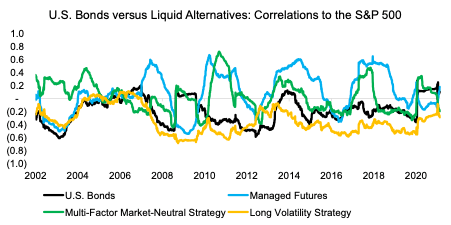

We observe that managed futures and the long volatility strategy generated a similar return to U.S. investment-grade bonds in the period from 2002 to 2021, although with significantly higher volatility. In contrast, the multi-factor market-neutral strategy generated a lower return, albeit also with less volatility.  Source: SG, FactorResearch MEASURING THE DIVERSIFICATION POTENTIAL The beauty of the 60/40 portfolio in recent decades was the largely negative correlation between stocks and bonds that generated attractive diversification benefits. In order to measure the diversification potential of the three liquid alternative strategies, we calculate the one-year rolling correlations to the S&P 500. We observe correlations of approximately zero of managed futures and the multi-factor market-neutral portfolio, similar to bonds, as well as a negative correlation of the long volatility strategy to stocks on average. It is interesting that the trends in correlations were often similar between managed futures and the multi-factor market-neutral portfolio, as well as between US bonds and the long volatility strategy, which indicates cross-strategy relationships.

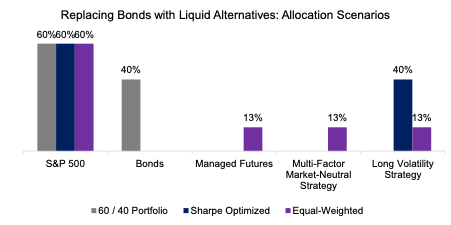

Source: SG, FactorResearch MEASURING THE DIVERSIFICATION POTENTIAL The beauty of the 60/40 portfolio in recent decades was the largely negative correlation between stocks and bonds that generated attractive diversification benefits. In order to measure the diversification potential of the three liquid alternative strategies, we calculate the one-year rolling correlations to the S&P 500. We observe correlations of approximately zero of managed futures and the multi-factor market-neutral portfolio, similar to bonds, as well as a negative correlation of the long volatility strategy to stocks on average. It is interesting that the trends in correlations were often similar between managed futures and the multi-factor market-neutral portfolio, as well as between US bonds and the long volatility strategy, which indicates cross-strategy relationships.  Source: SG, FactorResearch ALLOCATION SCENARIOS Given that we have verified that the three liquid alternative strategies offer uncorrelated returns to equities, the next question is how much to allocate to each. We can simplify the asset allocation framework by keeping the allocation to equities fixed at 60%, so we only need to allocate the 40% that historically went to bonds. There are many asset allocation frameworks and all have strengths as well as weaknesses; none is clearly superior. We are going to contrast two models, one that optimizes the Sharpe ratio over the 20-year period and a second one that allocates equally to the three strategies. Goal-seeking for the highest risk-adjusted return is a purely backward-looking process and typically results in the out-of-sample returns being less attractive than the in-sample returns, so investors need to be wary of this approach. The optimization process results in a zero allocation to managed futures and the multi-factor market-neutral strategy, which is surprising given that combining uncorrelated strategies typically maximizes the Sharpe ratio. In this case, the entire 40% allocation moved from bonds to the long volatility strategy. Interestingly this result remains unchanged if we reduced the lookback period for the optimization from 20 to 10 or even 5 years, or if we move from risk-adjusted to absolute returns. The long volatility strategy dominates as it provided positive returns that were slightly negatively correlated returns to equities, which generated the largest diversification benefits.

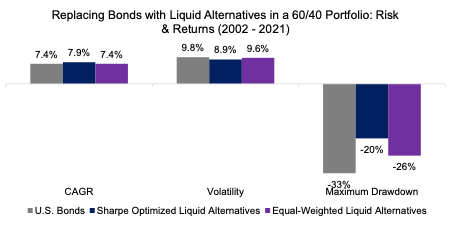

Source: SG, FactorResearch ALLOCATION SCENARIOS Given that we have verified that the three liquid alternative strategies offer uncorrelated returns to equities, the next question is how much to allocate to each. We can simplify the asset allocation framework by keeping the allocation to equities fixed at 60%, so we only need to allocate the 40% that historically went to bonds. There are many asset allocation frameworks and all have strengths as well as weaknesses; none is clearly superior. We are going to contrast two models, one that optimizes the Sharpe ratio over the 20-year period and a second one that allocates equally to the three strategies. Goal-seeking for the highest risk-adjusted return is a purely backward-looking process and typically results in the out-of-sample returns being less attractive than the in-sample returns, so investors need to be wary of this approach. The optimization process results in a zero allocation to managed futures and the multi-factor market-neutral strategy, which is surprising given that combining uncorrelated strategies typically maximizes the Sharpe ratio. In this case, the entire 40% allocation moved from bonds to the long volatility strategy. Interestingly this result remains unchanged if we reduced the lookback period for the optimization from 20 to 10 or even 5 years, or if we move from risk-adjusted to absolute returns. The long volatility strategy dominates as it provided positive returns that were slightly negatively correlated returns to equities, which generated the largest diversification benefits.  Source: FactorResearch As bonds generated high risk-adjusted returns over the last two decades, it is surprising that a portfolio with a 40% allocation to a long volatility strategy would have generated a higher return and lower maximum drawdown. Furthermore, even equal weightings to all three liquid alternative strategies would have resulted in better risk-adjusted returns than using bonds. Stated differently, investors could have replaced bonds with liquid alternatives already and would not have incurred a worse investment outcome over the last 20 years.

Source: FactorResearch As bonds generated high risk-adjusted returns over the last two decades, it is surprising that a portfolio with a 40% allocation to a long volatility strategy would have generated a higher return and lower maximum drawdown. Furthermore, even equal weightings to all three liquid alternative strategies would have resulted in better risk-adjusted returns than using bonds. Stated differently, investors could have replaced bonds with liquid alternatives already and would not have incurred a worse investment outcome over the last 20 years.  Source: FactorResearch FURTHER THOUGHTS This analysis can be easily challenged as the liquid alternative strategies partially excluded transaction costs, which would have resulted in lower actual returns, and are not liquid enough to offer a true alternative for the trillions invested in fixed income instruments. Unfortunately, there is no alternative for the global pension funds than to dramatically reduce expected returns and cut pension payments. In the coming decades, this will result in unsound political and economic decisions as the power of the elderly is growing given negative demographics. They have plenty of time to fight for their well-being. Politicians will cave to their demands, which practically means higher pension payments financed by more public debt. Ironically, this makes again an even stronger argument for liquid alternatives like long volatility strategies over bonds where investors assume that they will be repaid. Better to adopt portfolios before the facts change. RELATED RESEARCH Creating Anti-Fragile Portfolios Volatility Hedge Funds: The Good, the Bad, and the Ugly Global Macro: Masters of the Universe Merger Arbitrage: Arbitraged Away? Multi-Strategy Hedge Funds: Equity in a Different Shade?

Source: FactorResearch FURTHER THOUGHTS This analysis can be easily challenged as the liquid alternative strategies partially excluded transaction costs, which would have resulted in lower actual returns, and are not liquid enough to offer a true alternative for the trillions invested in fixed income instruments. Unfortunately, there is no alternative for the global pension funds than to dramatically reduce expected returns and cut pension payments. In the coming decades, this will result in unsound political and economic decisions as the power of the elderly is growing given negative demographics. They have plenty of time to fight for their well-being. Politicians will cave to their demands, which practically means higher pension payments financed by more public debt. Ironically, this makes again an even stronger argument for liquid alternatives like long volatility strategies over bonds where investors assume that they will be repaid. Better to adopt portfolios before the facts change. RELATED RESEARCH Creating Anti-Fragile Portfolios Volatility Hedge Funds: The Good, the Bad, and the Ugly Global Macro: Masters of the Universe Merger Arbitrage: Arbitraged Away? Multi-Strategy Hedge Funds: Equity in a Different Shade?