By Masao Matsuda, PhD, CAIA, FRM, President and CEO of Crossgates Investment and Risk Management.

Recently, some institutional investors have adopted the Total Portfolio Approach (TPA) whereby the distinction between traditional investments and alternative investments is de-emphasized. In fact, the CAIA Association now maintains that “in today’s investment landscape everything is an alternative.” While this may sound like a bold description of the relationship between traditional investments and alternative investments, when focused on the complexity of risk management and alpha opportunities as core elements of asset allocation, one finds it to be a quite apt expression. This blog post will suggest a prescriptive framework to implement TPA while pursuing asset allocation among traditional assets and alternative investment strategies in an integrated and seamless manner. Admittedly, there may be other ways to pursue TPA, but the author believes that what is proposed below is a flexible framework that can be successfully adapted by different types of institutional and individual investors.

Expanding Role of Alternative Investments

When market size is emphasized, asset allocation decisions will naturally focus on traditional asset classes which are known to have large capitalization or outstanding amounts.[i] By contrast, alternative investments are a collection of strategies that invest in various assets and/or investment contracts, and represent a fraction of the size of traditional assets.[ii] Based on the commonly held belief that in an efficient market determining asset weights based on market capitalization leads to the optimum asset mix, investors are often propelled to seek allocations centered on traditional assets.

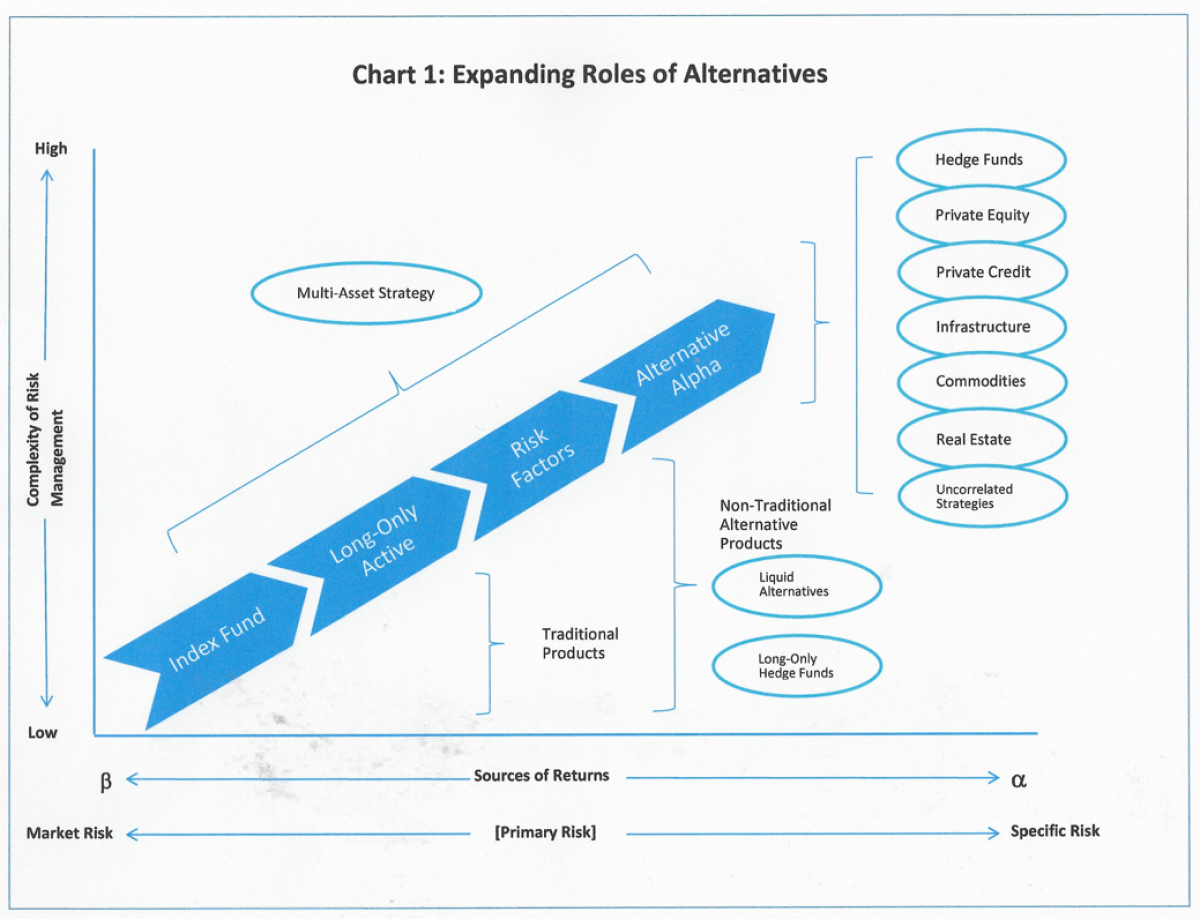

Despite the handicaps stemming from market size, the importance of alternative investments has been steadily rising. Chart 1 is a modified version of the chart that appeared in the paper entitled “Alternative Alphas and Asset Allocation”[iii] and highlights the expanding role of alternatives in investment management. The vertical axis represents the complexity of risk management. Along the axis, index funds are considered to have lower complexity compared to alternative alpha strategies such as hedge funds and private equity investments. Factor-oriented investments are positioned in between.

The horizontal axis represents the sources of returns. At the lower left corner lies index funds, the returns of which are derived from beta exposure to risks such as equity market risk. As one moves to the immediate right of index funds one finds long-only active investments. Together with index funds, these constitute traditional investments. Farther to the right are various factor exposures, sometimes referred to as smart betas, strategic betas, alternative betas or risk premia. Finally, toward the upper right corner lie various alternative investment strategies, whose sources of returns are principally derived from alphas or specific risks.

Viewed through a different lens such as the one depicted in the chart, a different mission for asset allocation is crystalized; the role of allocators should be to find a combination of asset classes and/or investment strategies that will enhance the probability of achieving a desired investment outcome (or outcomes). These investment outcomes are also referred to as investment goals, and will be discussed in a later section. On the other hand, seeking the asset mix that purportedly optimizes payoffs in the static and two-dimensional risk-return space, as practiced in a traditional asset allocation, does not lead to achieving investment outcomes by itself. Achieving these goals requires a more dynamic and purposeful approach which takes into account the complexity of risk management and alpha opportunities.

Behind the rise of alternative investments lies a broad set of opportunities to generate alphas for these investments. Alternative investments are less constrained by relative performance benchmarks such as information ratio, and often enjoy freedom to adjust exposure to underlying assets. These investments can also employ leverage. To the extent that the opportunity set is greater, the complexity of risk management is undoubtedly higher.

Since the seminal work of Brinson et al.[i], it is well-known that asset allocation is the most critical determinant of investment performance. This is the major reason that Strategic Asset Allocation (SAA) has been emphasized in institutional asset management for many decades. SAA, however, assumes that investment conditions remain the same for the relevant time horizon for which an allocation strategy is pursued. In reality, investment conditions generally fluctuate and various factors affect the performances of asset classes within any given period.

Through dynamic allocation, one can add returns or “allocation alphas.” Among various alpha opportunities afforded to alternative investments, allocation alphas are a critical element in discussing the Total Portfolio Approach. For instance, significant levels of allocation alphas can be achieved by avoiding (or reducing) exposure to equities when high equity volatilities are expected. There are sufficient empirical evidences supporting the significance of allocation alphas. This is true with many traditional asset classes[ii] and alternative investment strategies.[iii]

While index funds may rank low in terms of the complexity of risk management and alpha opportunities, it still has a role for large institutional investors who will easily face capacity constraints of many funds and managers. In this sense, for allocators, CAIA Association’s assertion that “everything is an alternative” is true, as choices of investment returns and risks should be managed in a holistic and logically consistent fashion. In effect, it is irresponsible not to examine all the choices.

The Total Portfolio Approach and Alternative Asset Allocation

As its name implies, the Total Portfolio Approach (TPA) is, “one unified means of assessing risk and return of the whole portfolio.”[iv] TPA is practiced by some well-known institutional investors including (1) Future Fund, Australia’s sovereign wealth fund, (2) CPP Investments, Canada’s largest pension fund, (3) New Zealand Superannuation Fund, New Zealand’s sovereign pension fund, and (4) GIC, Singapore’s wealth fund.[v]

These institutions by no means employ TPA in a “monolithic”[vi] manner. Instead, they tend to emphasize different aspects of TPA such as governance structure or a single portfolio culture.[vii] However, there are several common threads that tie together the practices of TPA. One such thread is the greater amount of freedom and responsibility given to a CIO and his/her offices. Underlying this thread is recognition of the dynamic nature of capital markets and investment opportunities, which necessitates timely and effective decisions and implementation, unhampered by a large committee or a board.[viii]

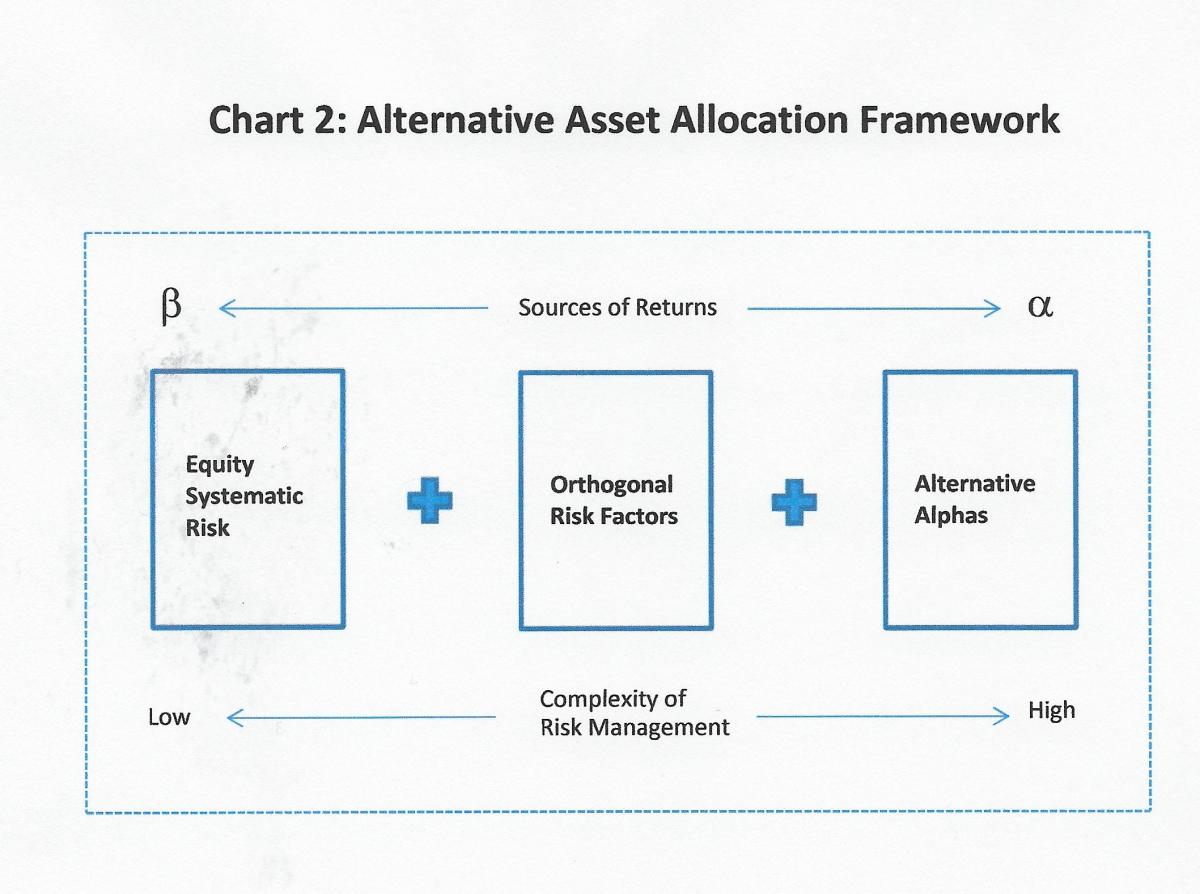

While the importance of TPA is patently clear, its principle remains normative. To gain wide-spread acceptance in the investment management community, a prescriptive approach is called for. The chart below shows one way to integrate asset allocation among various assets while harvesting risk premia and pursing alpha opportunities in a way consistent with the basic tenets of TPA.

In Chart 2, which originally appeared in “Alternative Alphas and Asset Allocation,”[i] there are three boxes or components depicting different sources of returns. The first component is exposure to the equity market or systematic risk, which is expected to carry risk premia and hence bring investment returns. The market risk corresponds to the single factor in the Capital Asset Pricing Model. The second component consists of a collection of risk factors, except for the equity market risk, and represents the middle portion of the investment universe depicted in Chart 1. A variety of risk factors such as smart betas, alternative betas and/or risk premia may be included. The third component represents various alternative investment strategies listed on the right-side of Chart 1. The sources of returns are alphas based on the skills of investment managers. Alternative Asset Allocation (AAA) can be pursued by any combination of these boxes or components.

Viewing investment opportunity through a factor lenses is another common thread found in implementing TPA.[ii] The first and second components in Chart 2 only consist of risk factors. While the third component is comprised of alphas from various alternative strategies, a large portion of these alphas may come from exposure to various risk factors. To effectively pursue alternative alphas, therefore, it is necessary to analyze the factor exposure of these strategies. Thus, both TPA and AAA are destined to apply factor-lenses.

When the three components in Chart 2 have no correlations among each other, allocation decisions can be made in a linear-additive fashion, and this makes an application of AAA markedly less taxing. Since there are so many choices in each of the second and the third components, it is not difficult to create a portfolio of factors or strategies that are orthogonally-related to other components. Even if a small-degree of correlation among each of the components exists, AAA is unlikely to lose its ease of application.

Making investment decisions in accordance with these components has three important properties.

- There is no need to rely on unreliable “expected return” parameters of each asset class or strategy.

- There is no need to determine an investor’s “risk tolerance,” which is unobservable, for portfolio construction or asset allocation.

- An investor’s desired “investment outcome” can be explicitly pursued by combining components or specific strategies in each component.

Thanks to these properties, the shortcoming of strategic asset allocation can be directly addressed. To illustrate, strategic allocation relies on the assertion that maintaining asset class weights essentially determine the result of asset allocation,[iii] and generating “expected return” parameters becomes a major undertaking to optimize asset weights in SAA. Unlike volatility, which is the square root of the second moment of probability distribution, predicting mean (the first moment) of returns is fraught with high uncertainty.

In the AAA framework, it is neither necessary to rely on expected return nor to assume a certain level of risk tolerance. In addition, instead of mean-variance optimization for allocation decisions, one can employ “volatility targeting” in order to decide the weight of each component.[iv] In contrast to expected returns, volatility of returns tends to be stable.[v] Next month’s volatility is likely to be similar to this month’s volatility. For asset allocation, therefore, it makes sense to focus on this relatively stable parameter.

Importantly, equity volatility has an ability to differentiate the returns of equity and other asset classes. When equity volatility is high, for instance, the returns of equity tend to be low or negative. When equity volatility is low, this asset class tends to reward investors with positive returns. When equity volatility is high, the returns of bonds tend to be larger than their average returns. When equity volatility is low, the returns of bonds tend to be lower than their average. This ability of equity volatility to differentiate returns of equities and bonds applies to other asset classes and investment strategies as well.[vi]

Moreover, as was discussed in the blog piece in Portfolio for the Future, titled “The Dimensions of Volatility,”[vii] equity volatility also affects “volatility” of other asset classes, as well as, “correlations” among these asset classes.[viii] In light of the fact that both volatility and correlations are calculated based solely on returns, this may not be surprising. Nevertheless, this observation has a practical significance, and is indispensable in seeking meaningful diversification.[ix]

Outcome-orientation

The outcome or goal-orientation mentioned in the first section, is yet another common thread binding the practices of TPA. While strategic asset allocation (SAA) leads to a theoretically optimum combination of asset weights given the level of risk tolerance, the underlying rationales for investments remain unaddressed. Conceivably, this has been the most significant failure of the SAA approach. Moreover, performance of investments in each asset class is evaluated against a benchmark representing each asset class. As a result, traditional investments based on SAA become “relative return oriented,” and these investments’ contributions to, or detraction from, desired investment outcomes are peripheralized.

Instead, an investment “should be managed with the objective of improving the probability of meeting future cash flow needs of investors, including capital gain, in accordance with the particular outcome being sought.” [x] To accomplish this, investment should be “agnostic of asset classes or investment opportunities,”[xi] and allocation decision should be dynamic and centralized in the office of the CIO or its equivalent. It is no coincidence that TPA calls for the greater role of the CIO in its implementation.

Desired investment outcomes vary, but the following four are among the ones emphasized by a variety of organizations[xii]:

- Inflation protection and real returns

- Volatility and risk management

- Equity risk diversification and market neutrality

- Alpha opportunities from expanded sources of returns

For individual investors, devising a policy for and implementing asset allocation decisions may be a tall order. Instead, these investors tend to invest in a product that purportedly balances allocation among different asset classes. These funds implicitly rely on SAA as a guiding principle. A common presumption is that when one’s investment horizon is very long, one can take a higher level of risk but when the horizon is short one should primarily invest in safe securities. For instance, in typical target date funds (TDFs), the weight of equity suggested for young people is very high because the level of risk tolerance is considered to be high. When one’s investment horizon is short, it is assumed that one cannot take a high level of risk and one should instead focus mostly on fixed-income securities.

To the extent that SAA has challenges, TDF also faces problems. Most critically, as discussion in the previous paragraphs indicate, even if one has an extremely long horizon, one is better off eliminating or reducing exposure to the equity market when high equity volatility is predicted.[xiii] This observation throws the core assumption of TDFs into question.

TDFs can be restructured so that these funds can directly address investors’ desired outcomes. For instance, when one has retired or is near retirement, one can focus on the outcome of “inflation protection and real returns.” On the other hand, for someone in their early career who either has started investment in equity or has indirect exposure to equity performance, the outcome of “equity risk diversification and market neutrality” may be important.

In an interesting twist, it may be easier to implement TPA through the AAA approach for portfolio managers of products for individual investors. According to Pensions and Investments, The California State Teachers’ Retirement System (CalSTRs) has recently created “a new division called total fund management to help make the $337.9 billion pension fund more resilient, flexible and dynamic.”[xiv] While CalSTRs has astutely decided to pursue TPA, the pension fund expects “it will take three years for the new division to fully ramp up.”[xv] The legacy investment process among institutional investors is hard to break. By contrast, in the case of the products intended for high-net-worth and other types of individual investors, the investment responsibilities can be fully delegated to a CIO or portfolio manager and these products can have pre-defined investment goals toward which allocation decisions can be dynamically pursued without being hampered by a legacy structure.

Managing Portfolio Risk and Tail-Risk

In SAA, the overall risk arising from traditional assets tends to determine the total risk of a portfolio, as alternative investments tend to account for a small weight. On the other hand, in AAA, weight can be determined based on the risk-reward ratio of each component shown in Chart 2. Suppose that one has targeted the volatility levels of the second and the third components at the levels that the first component (the volatility of equity market risk, e.g., 15% per annum) has maintained. Suppose further that the second and the third component can be constructed so that they have zero (or near-zero) correlations to the first component, i.e., equity market risk. In this case, the total volatility of the portfolio resulting from AAA is expected to be lower than the targeted levels of volatility for each component as substantial diversification effects can take place.

In a typical implementation of SAA, the mean-variance optimization approach is employed. One of the well-known weaknesses of this approach is that, by definition, only the mean and variance of returns are taken into account. In terms of “moments” of probability distribution, however, tail risks appear in the third and the fourth moments (skewness and kurtosis), rather than in the first and second moments (mean and variance). Negative skewness along with excess kurtosis, for instance, implies a return series that contains a high degree of tail risk. Needless to say, in seeking a pre-determined investment outcome, tail risk or downside risk can significantly affect such an outcome.

In implementing the AAA approach, one can pursue detailed analyses of tail portions of return distribution quite effectively and adjust the investments in each component accordingly. Moreover, potential tail risks which have not materialized in the past performance record can be analyzed by checking exposure to proxy factors that may have unacceptable levels of tail risks. Many alternative investment strategies extract alphas by altering the probability distribution of underlying investments, and in the process may induce tail risks.[xvi] For this reason, implementing asset allocations that include alternative investments need to employ measures that minimize or mitigate tail risks.

One metric often used in tail risk analysis is Conditional Value at Risk (CVaR). It represents the left side of threshold for a Value at Risk (VaR). For instance, 95% VaR will leave 5% of a distribution in the left tail and the mean value of the tail is the CVaR for the distribution. While it is mathematically simple, CVaR has an added benefit of being a “coherent measure of risk” and enjoys characteristics that are valued in financial risk management such as “sub-additivity” whereby the combined risk of two portfolios is less than or equal to the sum of risk of each portfolio.[xvii]

Additionally, the tail risk inherent in traditional assets such as equity can be mitigated in making use of volatility prediction. As was discussed in “The Dimensions of Volatility,” the value of S&P 500’s CVaR was 2.5 times higher in high volatility months (12.45% in 114 months with high volatility out of 228 months from October 2004 to September 2023) than in the low volatility months (4.86% in 114 months with low volatility). A similar tendency was observed in MSCI EAFE (14.04% vs. 4.88%) and MSCI Emerging Markets (18.48% vs. 8.66%).[xviii] This means that by avoiding, or reducing exposure to, investment in equity in the months with high predicted volatility, one can lower tail risks markedly.

For institutional investors with large investments in active equity mandates, it may not be practical to dynamically adjust the equity exposure based on predicted levels of equity volatility. One effective remedy in such a situation may be to apply an overlay strategy that invests in assets/factors which tend to do well when equity volatility is high. It has been demonstrated that using a group of risk factors for the overlay can improve returns while reducing the risks including CVaR.[xix]

Conclusion

The Total Portfolio Approach (TPA) can be effectively implemented through the Alternative Asset Allocation (AAA) approach described in the above sections. By isolating exposure to equity market risk, among other risk factors, one can better manage exposure to this critical source of returns. By formulating a portfolio of risk factors that are uncorrelated to other investments including equity, one can effectively pursue allocations that do not rely on traditional classification of asset classes. By investing in a portfolio of alternative investment strategies, one can add alphas from various skill sets of investment professionals. By making use of predicted levels of equity volatility, one can extract allocation alphas and lower both overall risks and the tail risks.

In the process of implementing asset allocation decisions, the goal-orientation of TPA can be expressly sustained while emphasizing the governance structure that concentrates decision making authority and responsibility in the office of Chief Investment Officer. The Strategic Asset Allocation approach has been taken for granted in the investment management community for too long. It is now time to shift to TPA and treat everything as an alternative as the CAIA Association maintains. In particular, the AAA approach highlights a framework that combines the three components of allocation in a linear additive fashion and seamlessly integrates allocation among traditional assets, risk factors, and alternative strategies.

Footnotes:

[i] At the end of 2022, traditional assets totaled around $127 trillion. See CAIA Association, “Innovation Unleashed: The Rise of Total Portfolio Approach,” p.6

[ii] At the end of 2022, the amount of assets invested in alternative strategies was reported to be around $22 trillion. See CAIA Association, p.6.

[iii] Masao Matsuda, “Alternative Alphas and Asset Allocation,” Alternative Investment Analysts Review, (Q1 2019), pp.17-26.

[iv] Gary P. Brinson, L. Randolph Hood and Gilbert L. Beebower, “Determinants of Portfolio Performance,” Financial Analysts Journal, (July-August 1986), pp.39-44.

[v] See, for instance, Masao Matsuda, “The Dimensions of Volatility.”

[vi] See, for instance, Masao Matsuda, “Time-varying Volatility Adds a Critical Dimension to Diversification,” and “Time-varying Equity Volatility Markedly Affects Hedge Fund Performance.”

[vii] CAIA Association, p.4.

[viii] Op. cit.

[ix] Op. cit.

[x] CAIA Association, p.14.

[xi] CAIA Association, p. 5.

[xii] Matsuda, “Alternative Alphas and Asset Allocation.”, p.23.

[xiii] CAIA Association, p. 19.

[xiv]While this assertion may be statistically true, given a set of asset classes, the classification of asset classes may be incorrect and/or insufficient.

[xv] For some alpha-generating strategies, one may not even need to target volatility and one can accept the strategy’s volatility as given.

[xvi]When the impact of equity volatility is taken into account, orthogonal relationships become easier to pursue; it is under high equity volatility that tail risk events often materialize and cause diversification effects among different asset classes to disappear.

[xvii] See Table 1 in Masao Matsuda, “The Dimensions of Volatility.”

[xviii] See “The Dimensions of Volatility.”

[xix] Notably, there are some asset classes and investment strategies whose returns are not well differentiated by equity volatility. Does this mean equity volatility is not a relevant consideration in allocation? The answer is a resounding “no,” as such an observation means that these asset classes and investment strategies are likely to be great diversifiers of equity risks regardless of the levels of equity volatility.

[xx]Diversification benefits are not likely to be priced by the market. The principle of the Arrow-Debreu completeness does not apply to these benefits; when a security can be replicated as a combination of two other securities, diversification effects of these securities are not taken into account. As a result, a strategy that effectively brings about diversification can provide a free lunch by enhancing returns given the level of risk.

[xxi] CaseyQuirk, “Life After Benchmark: Retooling Active Asset Management,” (November 2013), page 3.

[xxii] See Callan Institute, “New Generation of Multi-Asset Class Strategies,” (January 2018).

[xxiii] These institutions include Morgan Stanley Wealth Management, Callan Institute, Prudential Investments, and McKinsey & Co. See Masao Matsuda, “Outcome-Oriented Alternative Investments,” Alternative Investment Analysts Review, (Q3 2019), pp.17-23.

[xxiv] “The Dimensions of Volatility.”

[xxv] Arleen Jacobius, “CalSTRs creates a new division, taking more flexible, dynamic investment approach,”Pensions and Investments (July 24, 2024).

[xxvi] Op. cit.

[xxvii] For instance, a study shows that between 1991 and 1997, 6% of OTM puts on the S&P 500 index had losses every month. This means that writing such put options would have generated profits every month for 8 years consecutively. See Mark Brodie et al. “Understanding Index Option Returns,” The Review of Financial Studies, (2009), pp. 4493-4529.

[xxviii] Other characteristics are monotonicity, homogeneity, and translation invariance.

[xxix] See Table 3 in in “The Dimensions of Volatility.”

[xxx] See Table 4 in “The Dimensions of Volatility.”

About the Author:

Masao Matsuda, PhD, CAIA, FRM is President and CEO of Crossgates Investment and Risk Management. He has over three decades of experience in the global financial services industry. He has acted as CEO of a US broker-dealer and CEO/CIO of a number of investment management firms. In addition to his broad knowledge of alternative investments and traditional investments, he also possesses a technical expertise in financial modeling and risk management. He is experienced as a corporate director for operating and holding companies, and as a fund director for offshore investment vehicles.

Prior to founding Crossgates Investment and Risk Management, Masao spent 18 years with the Nikko group of companies of Japan. For the last seven years of his career at Nikko, he served as President/CEO of various Nikko entities in the US, and as a director of Nikko Securities Global Holdings. He received his Ph.D. in International Relations from Claremont Graduate University. He holds CAIA and FRM designation. He is a member of the Steering Committee of CAIA’s New York Chapter, as well as a committee member of GARP’s New York Chapter. He can be reached at matsuda@crossgates-im.com.

"All posts are the opinion of the contributing author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CAIA Association or the author’s employer."